Next week, the California insurance commissioner will propose legislation to deter small employers from exiting the traditional health insurance market and going self-insured. The legislation will put a floor on the amount of losses an employer must incur with any one employee before the stop-loss coverage is triggered (“attachment point”). This won’t affect larger employers which benefit from the balancing impact of their large numbers and so only need to protect themselves from the most catastrophic risks. The bottom lines of self-insured smaller employers are much more vulnerable to even a moderately ill employee; therefore, lower loss thresholds for stop-loss coverage are important to make self—insurance viable for small group.

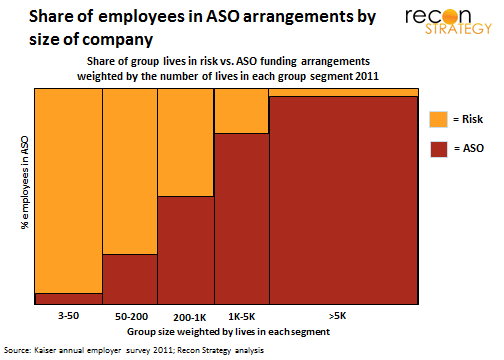

The potential for growth in smaller group ASO is large because the majority of these lives remain in risk arrangements (see the orange parts in the chart below). Conversion opportunities among the larger employers are rarer.

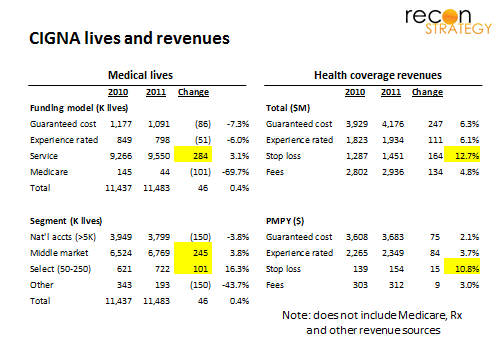

And it appears that “attacker” insurers such as Cigna are figuring out the right model to offer these employers (being an “attacker” is important because the $ profits on an ASO live are usually far less than a risk life so incumbents face a cannibalization dilemma in driving ASO). Let’s take a look at Cigna results which has lives helpfully reported both by funding model — risk, ASO — and by segment — national >5K, middle market and small group (50-250 lives) – which they call Select:

The ASO value proposition is multi-dimensional (flexibility, better data, more control), but lower cost is at its core. If an employer believes it has a lower cost group than the broad risk pools insurers are using the price (or can reduce costs with a more closely managed medical strategy), ASO will appear an attractive option. Healthy groups leaving the risk pool can set regulators on edge (not to mention hitting state budgets directly but losses in taxes on premiums etc.). No wonder California regulators (bruised by a brutal series of increases in the individual market) are intervening. Policy thinkers are recommending tighter controls. Other states that have put limits on stop-loss: for example, New York and Oregon prevent the sale of stop loss to groups <50. The NAIC decided in early March to update the various attachment points in their Stop Loss Model Act to reflect recent claims experience. Other states are rethinking regulatory strategies as well (see the RFP from New Hampshire for a consultant to make recommendations on the stop loss regulations).

Two observations:

First, intensifying stop-loss regulations may not stop ASO penetrating small group in its tracks: the attachment point floor being considered is $40K per employee which is far more than the $10K or $20K currently being sold in California for groups of ~25 but well above the average attachment point of $74K for the 50-200 group ASO market. Implication: a floor of $40K may put ASO out of reach of <50 groups and make less attractive to groups of 50-100, but there is still plenty of opportunity among larger end of small group.

Second, to the extent the ASO escape hatch is “blocked” employers will look at other mechanisms to control costs. As these regulations are updated, the appetite among the affected small groups for defined contribution / private exchanges will correspondingly swell.