Summary

- A Portland-based urgent care operator is launching a health plan from scratch

- The strategy targets the busy and healthy with the convenience of a retail network providing “store brand care”; a simple, consumer oriented service model at low cost.

- Carving out this segment can plausibly allow for sustained advantage in admin, medical cost and revenue management.

- The plan has hit a speed bump with regulators on pricing, so evidence of this model’s market appeal will come slowly.

- Convenience care has historically played nice with the ecosystem, but Oscar’s explosive valuations may convince some to be more aggressive. Insurers may end up competing not just with Oscars but with low-cost Oscars enabled by a tight but convenient primary care network.

- If “healthy specialist” models become more prevalent, incumbents might find themselves with an increasingly sicker pool. Models differentially focused on the well vs. the sick could become as relevant and prevalent in retail healthcare as the split between ASO and risk has historically been in the B2B group market.

- If the urgent care operator’s insurance product shows signs of life, United may have bought itself an increasingly valuable option with its acquisition of MedExpress earlier this year.

Zoom’s urgent care platform

Zoom+ is a leading urgent care center operator in the Pacific Northwest with 27 sites mostly in Portland and the rest in Seattle. The nearest rival in Oregon is Providence Health (one of the largest Pacific Northwest delivery systems), and Everett Clinic in Washington, with 9 sites each.

The Zoom model in brief:

- Network of small sites (~1K square feet) located in high traffic areas

- High leverage staffing model focused on PAs (and, occasionally, NPs)

- Each site offering minor acute care coupled with onsite x-ray, simple labs and dispensing of up to ~100 prescription and OTC medications.

- High density in core markets, allowing for overlapping hours and strong demand management (patients secure same day appointments at their site of choice via the web; if not enough slots are available, they are guided to nearby locations).

- Various types of virtual visits and ancillaries are also available.

Zooming vertical

Leading urgent care operators usually focus on expanding geographically and “keep the peace” by triaging high-margin, high-acuity cases out to incumbent providers. Zoom, however, is expanding “vertically” – adding primary/chronic, specialty care, limited dental, and now health insurance starting in 2016 funded by selling Endeavor Capital a 20% share in the dedicated insurance subsidiary.

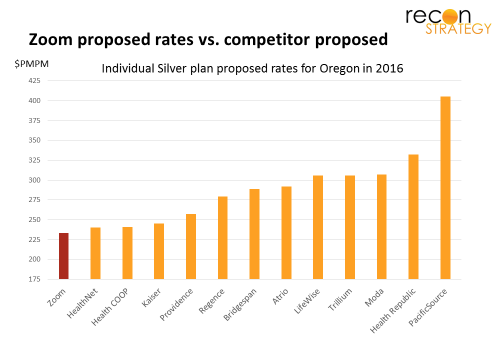

The products are tightly controlled for low-cost care delivery. Members can only go to Zoom for their scope of service and a narrow specialty care network for everything else (mostly focused on OHSU, a powerful Portland brand which should allay concerns on quality of care in the case of catastrophic bad luck). In its initial filing, Zoom contemplated a $233 PMPM base premium (Silver 40), the lowest amongst requested rates and 18%+ below the weighted average rate request. Key drivers were an assumed 14% cost advantage via provider reimbursement and medical management and amortizing large start-up administrative costs over a five year growth period.

The pricing, network configuration, and care management model seem surgically designed to appeal to busy, healthy members looking for good benefits (e.g. silver plan level). And that segment is not small, in Zoom’s thinking: they planned for 4,500 members in 2016 and ~50K members (25% of Oregon’s current individual market) by 2020 (our guess based on the filings).

Even so, the move is puzzling. Why is it better to build a brand new insurance company – with a lot of start-up cost and strategic risk in rattling incumbents – rather than just continue serving this segment as an urgent care provider? Or partnering with an existing insurer on a co-branded narrow network product?

Making money on the low-risk

I see three potential paths (potentially complementary) by which Zoom health insurance can achieve advantaged profitability:

Revenue management: Risk-adjustment arbitrage

Risk adjustment (the regulator-driven reallocation of premium dollars across insurers based on the distribution of membership risk) should lower Zoom’s net revenue if it attracts more than its fair share of the young and healthy. But the rules cannot fully correct for the impact of risk, allowing room for “arbitrage:”

First, plans need to work to document risk to get full credit in adjusted premiums. Given low premiums typical on exchanges, however, they are unlikely to work very hard (the ROI just isn’t there for a lot of costly home visits for example) leaving plans with higher average risk membership underpaid and – given budget neutrality rules on the Exchange – plans with lower average risk membership potentially overpaid.

Second, risk adjustment focuses on diagnosis and demographics, not care behavior. If Zoom members are biased towards lower utilizers for a given level of risk (e.g. busy people who let minor complaints resolve on their own) and more ready to adopt low cost care models (e.g. APN care, telemedicine), it is easy to see how diagnosis-based risk adjustment might overpay for these patient behaviors.

Medical cost: Insulating members from big system restructuring pain

Today’s providers are top-heavy with specialist and facility capacity . The lumpy nature of this capacity will constrain restructuring and force providers to recover fixed costs over a future of declining volumes. Incumbent insurers with multiple lines of business will be reluctantly forced to accommodate. Further, providers are struggling with the change management of getting their (often senior, comfortable) practitioners to deliver retail care (e-visits, “retail” clinic hours, team delivery, demands of continuity of care).

Zoom insurance won’t have either burden: it owns no big ticket facilities and can “rent” what other clinical infrastructure it needs. As long as it can maintain a branded tertiary care partner in its network (and game theory says it will), it should be able to shield its members from those fixed cost recovery efforts. And, because Zoom is building its provider system organically, it can recruit “Zoomers” most ready to adopt new, technology driven care models, making the change management issues much easier.

Admin cost: modeled for simplicity and for the self-server

A savvy membership trained to go online for same-day appointments and broadly accepting of new care channels (e-visits) is also probably more accepting of web-based and self-service administrative service models. Product simplicity coupled with a care front aligned and supportive of the insurance model’s priorities can also save a lot of cost which might otherwise get spent on educating members. Network simplicity and focusing the referral network on OHSU (a partnership that Zoom has already enjoyed and extended) can likewise save on network management costs.

Zooming past Oscar?

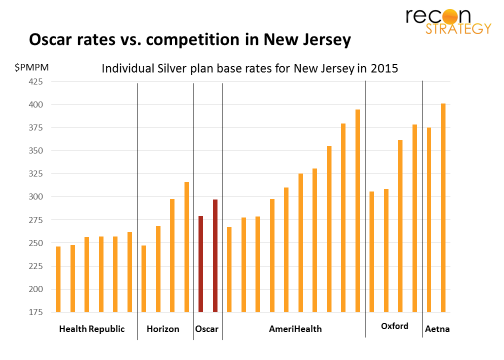

Zoom’s focus on technology, simplicity, ancillary product features and consumer delight is similar to Oscar, the New York / New Jersey focused health insurance start-up valued in its most recent funding round at $1.5B. They are certainly targeting similar segments of the market, but Oscar lacks the “store brand” care front end and same strategic partnership in its network. As a result, its premium pricing is best described as “ just below average” vs. Zoom’s “lowest in the market” strategy (compare graph below vs. Zoom’s target premium position):

Oscar and Zoom’s growth strategies will necessarily also look different. Zoom has been building its urgent care brand in the Portland area since 2006 (a decade before it will begin selling its insurance). Growing bricks and mortar takes time and resources. In fact, Zoom pulled out of Idaho in 2014 to focus resources on its existing markets. Accordingly, Zoom’s growth strategy will focus on achieving depth in a smaller number of markets rather than a presence in a larger number of markets. Oscar, on the other hand, not tied to any bricks and mortar, can swiftly expand geographically without needing to take as much share in each market. We already see a focus on rapidly expanding into new large markets, building on their New York and New Jersey entry with plans to launch in California and Texas.

A fine theory hits “regulator-grade” reality

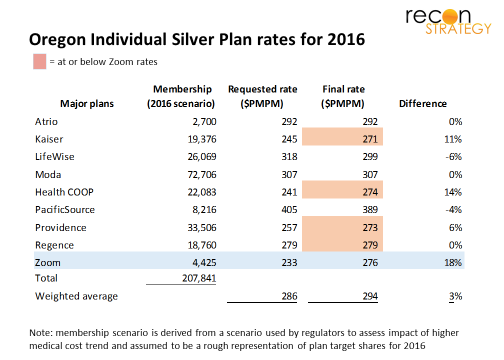

Unfortunately for Zoom, Oregon regulators were not inclined to experiment for 2016. Having seen major losses among Exchange insurers in 2014, and more on the way in 2015, their focus was on ensuring stability. Among other things, they disallowed Zoom’s 14% care cost advantage assumption and doubled the G&A PMPM in the premium build because they did not accept the start-up cost amortization plan. These – plus other changes – increased Zoom’s base premium target (Silver 40) to $276 PMPM, on par with approved rates for Providence ($273), Kaiser ($271) and Regence ($279) and now just 6% below the market weighted average (See table).

A decisive blow to the strategy? Doubt it. CEO Dave Sanders is savvy enough not to have put his chips in a single year’s regulatory review process. But the outcome will certainly slow things down. Expect to see Zoom push other elements of its value proposition – talking up the brand, the access, the OHSU connection – and adding more hooks. But the case will be harder, and competing providers are not standing still. Providence Health, for example, has brought in Amazon executives to “disrupt from within” and currently has $39 on-demand, online telehealth appointments and is piloting $99 physician visits to the home or work. Expect also to see Zoom push harder outside the regulated market (benefit consultant managed private exchanges, ASO).

Implications

Zoom strategy exploits the classic “innovator’s dilemma” constraints on incumbents:

- Large, hospital-centered integrated provider systems are becoming increasingly prevalent but will be challenged to address the shift towards retail and financing the fixed cost of facilities infrastructure

- Insurance and provider systems will naturally gear towards higher margin patients (Medicare), potentially leaving the healthy, convenience oriented, and low risk unsatisfyingly served

Healthcare going “retail” will be more than just mastering exchanges, building direct marketing engines or integrating patient feedback scores into management processes. As a second order effect, it also means opening the door to new entrants deploying classic retail business strategies such as low cost competitors who build a self-reinforcing advantage via a self-selecting segment focus (think Aldi / Trader Joe’s).

In the light of Zoom’s plans, United’s recent acquisition of MedExpress (the leading urgent care network with heavy concentration in the Mid-Atlantic) suddenly looks a lot more intriguing. Could the Pittsburgh market be the next test case for the Zoom strategy?