A few problems

Geographic barriers to the entry have long protected providers from best-in-class competition. Provider consolidation – theoretically a logical response to the current operating environment — reinforces these barriers by locking up referrals and making systems too big / too few to fail. Instead of pushing providers aggressively on value, payers and regulators may end up nursing underperforming systems (e.g. Highmark’s bail-out of the West Penn Allegheny system) and discouraging disruptive entrants for fear of unintended damage to the stability of the local provider infrastructure. Even if consolidation is necessary for value-based care, the result looks like a leverage grab. In the long run, it will be hard even for the most mission-driven providers not to use this leverage in negotiations with payers to defer or blunt painful change.

Without restoration of strong competition, the pace of value improvement may be glacial. How can competitive forces be orchestrated to drive local performance faster towards national best practice? How can geographic barriers to entry be broken down?

Potential solutions and their failings

Cross-geography alliances between national providers and local partners could theoretically accelerate best practice adoption. But change requires enormous effort (systems, procedures, culture and talent) while the actual commitments in many alliances is limited (second opinions, conferences on pathways, some trial access, a new logo, etc.). So, unless the alliance is tied with an integrated bottom line (via a clinically integrated network or change of control) or is otherwise strategically critical for both sides, day-to-day operational demands will get in the way of real impact.

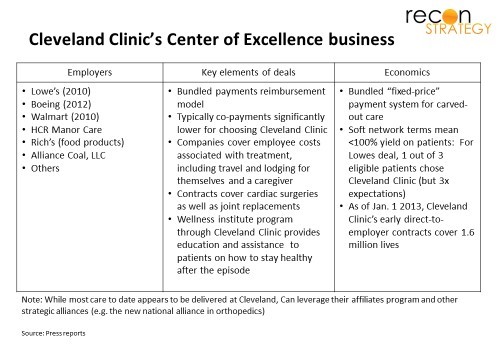

Medical tourism could ease geographic entry by exploiting the at-scale operations in the entrant’s home market (vs. building a new infrastructure locally). To date, however, only a trickle of enterprising patients and innovative plan sponsors have tapped into this opportunity for a limited scope of care. See exhibit for a brief overview:

While intriguing, direct contracting for Centers of Excellence (CoE) have hardly taken off: Not only do local providers lack the incentives to export patients; CoE strategies generally focus on the acute intervention episode only for conditions which can be neatly separated from pre-, post- and parallel care into an episode (such as transplants, selected orthopedics, etc.), leaving the potential for best-in-class pre-episode management which may delay or avoid the need for big interventions as well as support after an episode’s “warranty” period — in other words, the population health component — unexploited. There’s just not enough value in the intervention episode alone to create a compelling value proposition for most patients and payers.

Care exporters need a direct channel to the patient.

Telemedicine could theoretically be that direct channel. Direct-to-patient telemedicine today is limited to the minor acute care which can be done outside an office, a few “touchless” specialties (behavioral, derm) and as a bridge between actual office visits. To move beyond triaging coughs and headaches, a remote care provider needs routine diagnostics and clinical hands for the physical exam, implying a private exam room, nursing staff, basic biometric and diagnostic infrastructure . That infrastructure is costly. Even if the remote provider is operating on a “marginal cost” basis, the infrastructure needs to be supported by a critical mass of local patient volumes. Ideal would be for the remote provider to rent an existing office infrastructure for the duration of an appointment. But that means collaborating with a local provider who, typically, will already have local referral partners.

A speculative answer

In other sectors where infrastructure economics are naturally oligopolistic (e.g. railways, energy utilities, telecom), regulators split the infrastructure from operations and opened that infrastructure for use by multiple, competing operators on a neutral basis. We also see the emergence of more and more “as a service” models offering infrastructure of various kinds “on demand.” Perhaps a similar model could be applied to healthcare.

Convenient care networks – retail clinics, urgent care centers, free-standing EDs, corporate clinics – are fast becoming multi-regional and national in scope. While many are owned by local providers, several of the largest are strategically neutral. These centers have a fairly consistent template with patient rooms, nursing staff, ancillaries (labs, often an x-ray, access to pharmacy), IT/EMR, and a compulsive adherence to protocols, all wrapped up in a convenient location and pleasant consumer experience.

What if these networks were to equip their sites with video interfaces and – either directly or via some intermediary bringing together several networks — offer their infrastructure and nursing staff as a point of care to remote providers for patient consultations? We could have:

- A larger scope of care deliverable by care-exporting providers

- A recognizable office setting which many patients still prefer

- Office infrastructure costs “variabilized” for the care-exporting provider making small volumes of patients feasible to serve and

- The convenience care provider’s own infrastructure costs partially offloaded by leasing out capacity at non-peak times .

Such a virtual office visit would allow the care-exporting provider to engage newly diagnosed patients before a major acute intervention, prescribe treatments that may delay or avert it altogether, make the call on the timing of major procedures and manage the preparations leading up to the actual intervention. A whole new scope of value can be created by best-in-class providers (taking on risk on a population vs. an episode) allowing for financing a stronger patient value proposition.

Further, using convenience care networks would make the care export operation far easier to scale because the convenience care provider’s standardized operating template and EMR making it far easier for a care-exporting provider to plug into many locations in one deal and standardize care protocol.

An example scenario

The Pittsburgh market has two main providers – UPMC and Highmark’s West Penn Allegheny. UPMC is strongly branded and struggling West Penn has run into the protective embrace of Highmark and is tapping the brand halo of Johns Hopkins in Maryland. Very few providers in Pittsburgh have not aligned with one camp or the other and consumers must largely choose between the nationally lauded care quality and high price tag of UPMC and the lower cost but largely unrated care from West Penn. Suppose Cleveland Clinic was interested in entering the Pittsburgh market in cardiology? Today, it would be unlikely to see many referrals from either incumbent.

MedExpress is a major urgent care chain operating in the Mid-Atlantic and a particular concentration in Pittsburgh. Its acquisition by UnitedHealth which should reinforce its strategic neutrality in most markets (and, if anything, bias it towards supporting more local competition). The typical MedExpress site is a de novo build with 9 to 10 exam rooms, a care team of APNs and nurses led by an MD and supported by a full complement of admin staff; on-site labs and x-rays.

If MedExpress were to equip some of its rooms with video screens, build EHR interfaces with Cleveland Clinic and open its calendar for appointments, it would be possible for the Cleveland Clinic to directly contract with Pittsburgh employers on a cardiac center of excellence carve-out. Patients could be engaged throughout their chronic conditions by top providers and, if necessary, elective and semi-elective procedures could be delivered in Cleveland.

From low cost beachhead to a care exchange platform

If the feasibility of convenience care sites as a rentable beachhead for care exporting providers could be demonstrated, several intriguing possibilities open:

There is no need for exclusivity: the infrastructure could work with multiple competing providers and allow plan sponsors to pick among several. Take our Pittsburgh scenario: other high performing Ohio providers (e.g. University Hospitals, OhioHealth, and Mercy) could contract to use the same infrastructure to compete with Cleveland Clinic and local incumbents for employer carve-out contracts. Perhaps contact terms could evolved (e.g. episode-based, PMPM, different bundles of therapeutic areas) and an exchange of sorts emerge whereby employers could evaluate different offers. A critical mass of carve-out and virtual medical home options will strengthen the value proposition .

The convenience care network could become a platform and may find it attractive to expand options by filling in clinical ancillaries on site, raise rental prices charged remote providers and develop a marketing channel for the model to employers (indeed some of the most prominent convenience care networks already have powerful channels to employers, health transaction management capabilities and consumer engagement and education capabilities within their corporate families)

As more specialty care can be covered in carve-outs, the platform provider may shift its own care model beyond minor acute care to include broader primary care, developing ongoing patient relationships, and helping patients navigate to the right remote care specialty provider when appropriate. The relationship between the convenience care platform and remote care provider might shift from being a vendor selling excess capacity to instead become a market maker and care “broker”.

Most importantly, by chipping away at the geographic barriers to entry, such a model could push local providers to compete not just with each other but with national best in class providers – and they will need to figure out how to match that performance quickly or cede that care where they cannot to others.

(Original article eddited for clarity on February, 28, 2016)