Earlier this month, Mercy Health announced deals to dismantle HealthSpan (the former Kaiser business in northeast Ohio acquired in 2013), selling the insurance arm to local powerhouse Med Mutual, dissolving the medical group, and transitioning physicians to various northeast Ohio providers. 2015 was supposed to be a growth year for the business, but membership declined across lines of business, PMPM costs ballooned and Exchange risk adjustment obligations wreaked havoc with the bottom line ( HealthSpan is said to cover 160K lives total, of which half are risk with the legacy Kaiser operation and its PPO sister and 45K Mercy employees who, together with dependents, presumably make up the balance).

What happened to the grand vertical integration scheme?

Large losses should give pause to any strategy, but abandoning vertical integration (a complicated play) after only 2 years (1 year really – the acquisition occurred so late in 2013 that the operating plan for 2014 was largely locked in) suggests either negative surprises in the underlying asset or rapid changes in the strategic environment.

I don’t believe there were any surprises about the asset: the Kaiser operation had been losing money well before the acquisition and, as a general rule, the Kaiser model is hard to grow in markets that lack exposure to and faith in the Kaiser brand. Mercy’s turnaround challenge was all the greater because it needed to build the HealthSpan brand from scratch (Using the Mercy brand would probably not have helped: “Mercy Health” was a brand under construction having been adopted by Catholic Health Partners in 2014; further Mercy had little local presence in the Cleveland area (other than well to the west in Lorain). Finally, as noted later, I suspect Mercy wanted its HealthSpan asset to become the branding for its state-wide activities supporting various provider partners. Branding the insurance arm as “Mercy” might have gotten in the way of that plan) . Clearly this approach was going to take a while to pay off.

The implication, then, is that there has been a change in the operating environment. The initial strategic pay-off for Mercy in the Kaiser acquisition was, I think, building a northeast physician footprint to cover more of the state and lock University Hospitals (UH), Cleveland Clinic’s primary local competitor, into the Mercy orbit. Immediately after acquisition, Mercy switched the tertiary referral care for legacy Kaiser patients from Cleveland Clinic to UH. They also appear to have tightened up on care outside the network (shifting more care to the contracted hospital and medical providers) which should have increased the volume to UH:

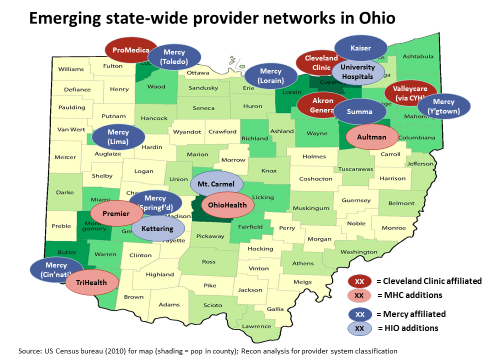

Roughly coincident with the Kaiser acquisition, UH was identified as a member of the Mercy-sponsored Health Innovations Ohio (HIO), a strategic collaboration among selected Ohio providers to promote value-based care and payment reform inside the participating systems (see chart below) – a short-term success.

The chicken and egg dilemma of building a provider-based insurance business

The longer-term strategic payoff for Mercy was, in my view, building out a state wide commercial insurance capability to put at the service of HIO. For that strategy to work, however, HIO members would need to collaborate operationally and be strategically aligned about competing with their customers (the plans). Starting points were mixed: Summa and Mt. Carmel have long standing Medicare Advantage plans, but have not pushed into commercial. UH had no insurance play of any kind and there was limited geographic overlap between Mercy’s provider operations and its Healthspan insurance operations. HIO was likely facing a classic chicken-and-egg new business problem: in this case — you need aligned providers to get patient flow; but you need the patient flow to persuade the providers to align. The Kaiser asset as is was just too small and local to drive alignment across so many systems.

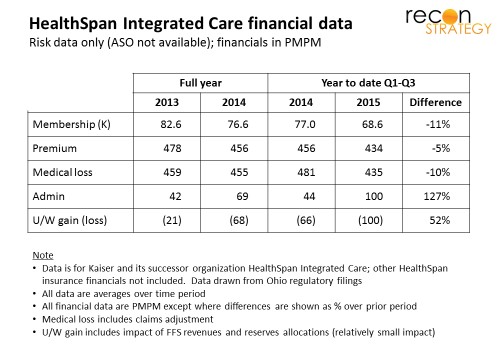

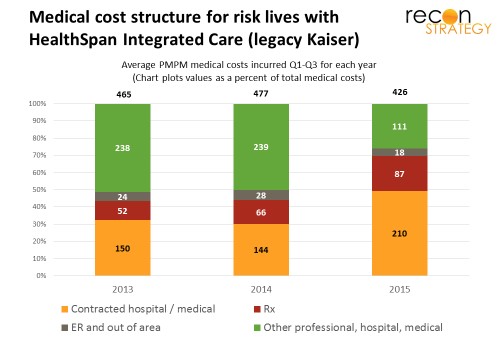

Mercy’s answer appears to have been: go big or go home. They seemed to have taken advantage of lower medical costs (-10% reduction vs. 2014 – see first chart) to fund lower premiums (-5% vs. 2014 but still operating at a 95% MLR), and launched an aggressive growth program driving a doubling of admin costs. It talked up its value to employers via PPO and self-funded options and the broader state network built on the Mercy system. But the results were ugly: continued loss of lives on all markets and a rapid run up of losses. Over a hundred million in losses later (reportedly $117M in first three quarters of 2015), Mercy threw in the towel.

Clinically Integrated Networks – the better mousetrap?

Mercy is not abandoning forward integration, just pursuing it in a more limited but (hopefully) more effective way. Simultaneous with the decision to shut down HealthSpan, Mercy and Summa introduced a clinically integrated network called Advanced Health Select for risk contracting and capability builds. Moving towards increasing accountability (all the way to percent-of-premium deals) can yield a lot of the rewards of forward integration with far fewer regulatory compliance, operational and ‘trench warfare’ customer acquisition headaches. Further, large employer lives – frequent targets of clinically integrated network deals – are more likely to yield brand new patients than small groups or individuals who self-select for a provider-sponsored narrow network.

If this view is accurate, Mercy has reached the same conclusion as many other providers pushing CINs for the commercial business, including Mercy’s prime competitor for leadership in Ohio, Cleveland Clinic. Their MidWest Health Collaborative (a state-wide partnership among six Ohio systems) had as one of its objectives when launched, assessment of the business case for a state wide provider network. This past November, MHC launched a search for a CEO among whose major responsibilities is listed as developing network business deals with employers. It sounds like that case came back positive.

Putting HIO in the refrigerator (for now)

One curiosity about Mercy’s CIN announcement was the absence of any other HIO members (some of whom have their own CINs already). One might have expected these CINs to be stitched together into a larger solution to appeal to more employers. Instead, the patchwork remains in place suggesting that the HIO partners are each going it alone at least for now.

Mercy does not seem to have solidified much of a relationship with University Hospitals in Cleveland despite the very expensive “gift” of a year’s worth of Kaiser referral care. UH seems strategically focused on solidifying its location position with hospital acquisitions and risk deals for its own system vs. participating in a state-wide game. Notably, UH did not affiliate with the HealthSpan physician group (as one might have expected if Mercy-UH relationship was tightly collaborative) and instead cherry-picked a minority of the physicians. In addition, UH appears to be acquiring practices in the Akron market south of Ohio, putting it a bit at odds with Mercy’s local affiliate, Summa.

One qualified success HIO can point to is Medicare Advantage. Two of the partners have homegrown MA plans and have seen substantial growth since the formation of the alliance and the inclusion of allied providers in the plan networks: Mt. Carmel’s MA enrollment grew from 30K at the end of 2012 to 57K as of March 2016. Summa’s MA plan grew from 24K at the end of 2012 to 32K at end of 2014. (Membership has since fallen back to 24K in March 2016 because they were hit with CMS sanctions for appeals process missteps late in 2014 which reduced the stars rating to 2.5 stars and prevented new enrollment but that can hardly be laid at HIO’s door).

Otherwise, HIO has not shown much life since the Kettering system joined in May 2014. The initial CEO, a former hospital executive jointly funded by the partners, has been replaced by Mercy’s current SVP of Payer Contracting apparently as a dual role. The partners’ ambitions for HIO are apparently modest enough that no dedicated CEO is necessary and the risks of divided loyalties not worth mitigating. It appears HIO is being scaled back for now until competitive pressures, regulatory changes or market opportunities can generate greater alignment.

Implications

- Right now, clinically integrated networks may offer a lower risk, lower cost way for providers to get into the attractive parts of the commercial insurance business (accountability, risk management) while avoiding the less attractive, more scale driven parts (marketing, regulatory compliance, operations).

- Plans should pay attention. If CINs focus on large employers, plans may find themselves competing against local CIN-enabled TPAs willing to operate on very thin margins. Mid-size employers might find self-funding with local high performing CINs attractive, further shrinking the profitable large group risk segment.

- The Mercy story does not challenge the idea that Medicare Advantage appears to be a viable market for provider-centered plans given the larger per-member dollars at stake, the closer relationship Medicare-eligibles have with their doctors, and the opportunity to shift FFS ACO lives into a more profitable and cash flow advantaged model (Mercy’s exit from MA when it sold off HealthSpan is not a real test: Mercy was not a major provider brand in the local market so lacked the advantages that most provider-sponsored plans have. Nor was it feasible to get rid of the commercial business and hold onto the Medicare business given the legacy Kaiser model. Finally, local powerhouse Med Mutual entered the MA business in 2016 which made the market much more competitive).

- Perhaps CINs that lack an MA offering today would make for interesting targets for partnership discussions to enable them to get into the business.