Back in 2013, Dignity and Optum formed a joint venture for revenue cycle management (RCM) services named Optum360. Dignity contributed processing centers and 1,700 employees in return for ~25% share in the venture. Optum contributed technology and 1,300 employees in return for owning the rest. In addition, Dignity promised to buy RCM services from the joint venture for the subsequent ten years.

At the time, our view was that the joint venture “marriage” gave Optum the scale and reference client needed to credibly compete vs. majors (R1, Parallon, Conifer) at a time when third party RCM appeared well positioned to take off given regulatory pressures (e.g. ICD-10, alternative payment mechanisms) and increasingly complex affiliation structures (too complex to integrate all the in-house operations). And, indeed, success has been substantial:

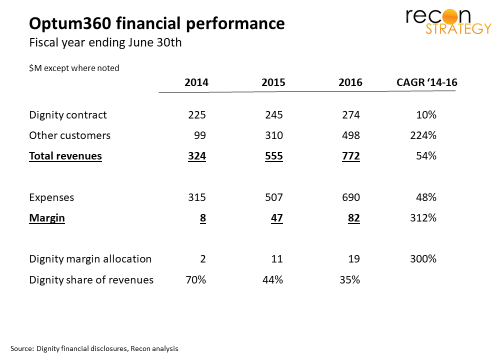

Note: We are dependent on Dignity financials for this view so limited to a fiscal year ending in June. Also, after 2016, Dignity no longer reported out Optum360 financials so no 2017 view is available.

The business growth appears to have come primarily from three publicly disclosed deals: Northwell (April 2015), Mayo Clinic (April 2015), and Quest Laboratories (September 2016). Each of these deals contain features which will be hard for pure play RCM competitors or EMR vendors to replicate:

- Northwell’s contract followed the Dignity template: Northwell signed a 10 year agreement for RCM services (for 14 of the 19 hospitals and worth $114M in fees in calendar 2016) and shifted about 1K employees over to Optum360 while receiving an 8% share in the venture (with both Dignity and Optum shares being diluted).

- The Quest deal was part of a package: in addition to providing RCM services, Optum made Quest its exclusive partner for diagnostics among its partners and clients.

- The Mayo deal appears to be a straightforward outsourcing deal but part of a broader strategic relationship. In 2013, Optum and Mayo launched a joint venture to identify care improvement opportunities from Optum’s vast data warehouses (OptumLabs). And Mayo is a key ongoing partner in Optum’s Center of Excellence program.

Thus, in 3 years, Optum grew a legacy $100M business to ~$1B in revenues (Piper Jaffray actually estimates current revenues at $1.3B) with multiple marquee clients (easing potential anxieties about trusting a United subsidiary with highly confidential contract rates information). And Dignity converted an administrative cost center into a 23% share (after dilution from Northwell entry) of an asset worth a couple billion at least. Well done!

Others are trying similar paths

Just last week, Hackensack Meridian Health (northern and central NJ shore) and Jefferson Health (Philadelphia) formed a joint venture with Med-Metrix (a small scale RCM vendor led by former MD-X/MedAssets executives) to perform revenue cycle services. Like Dignity, Hackensack understands that an anchor customer can add immensely to the capability and credibility of a small scale vendor and wants its share in the value creation.

The fact that Hackensack brought only Jefferson’s NJ hospitals — which it acquired via a merger with southern-NJ based Kennedy Health last month — into the venture also suggests some underlying plans for a state-wide network collaboration. Hackensack Meridian covers the Jersey coast pretty well but lacks a footprint south and inland near Philadelphia. So Hackensack Meridian may have been interested in the managerial influence a JV structure can offer as well.

Future of outsourced revenue cycle management

The “sea change” shift to end-to-end outsourced RCM which many (including us) have been expecting has yet to happen. A few big deals have trickled out each year – in particular, Optum360’s wins plus some expansions of existing arrangements: for example, Conifer’s big win with CHI in 2015 only added 20 hospitals to the 56 they have been serving under a 2012 deal. And their contract to serve 6 hospitals of Wellstar (Marietta, GA) won in 2016 was probably helped by the fact that Conifer supported the other 5 hospitals in Georgia that Wellstar bought from Tenet earlier the same year.

But most providers keep the bulk of RCM internal. Surveys (e.g. the hospital survey run by UBS) suggest between 10% to 15% of hospitals outsource their RCM to (non-EMR) vendors (the same surveys suggest 2-5% use their EMR vendor to support RCM). On the other hand, hospitals do appear to increasingly rely on vendors for specific services to fill in internal capability gaps (for example, Black Book’s recent survey of hospital CFOs suggests ~40% now outsource complex claims vs. 20% in 2013). Perhaps RCM is perceived as too central to patient experience (the Accretive scandals of 2011 /12 may continue to color perceptions) or too much in need to local customization (given contract terms or payer practices) to be safely vendored out on an end-to-end basis.

Perhaps for this reason, RCM M&A (e.g., Navicure’s acquisition of ZirMed in September) have become a popular way to add tuck-in capabilities, broaden the menu for clients as well as hunt for new relationships for cross-selling. But that model for industry growth plays right to Optum360’s hands. Not only can it aggressively acquire (e.g. Optum’s recent acquisition of Advisory Board which brings with it RCM assets and a large network of provider relationships), but Optum’s provider service portfolio extends far beyond RCM (analytics, population health, etc). Whether outsourced RCM remains a patchwork of targeted service carve-outs or transitions to more of an end-to-end model, Optum360 can expect to win.

When we first read about the Optum360 deal in 2013, we thought Dignity was the right family for Optum to marry into. Maybe it was really the other way around.