OptumHealth and its proposed acquisition target DaVita Medical Group (DMG) have a lot in common:

- Ambulatory care portfolios: physician practices, urgent care centers and ambulatory surgical centers (ASCs) – both directly owned and affiliated via owned independent practice associations (IPAs)

- Geographic position: multiple states and markets

- Advantaged model: within-market cross-referrals and care collaboration which should support market share, economics and a value-based care advantage

- Construction: largely assembled via acquisition resulting in similar challenges in integrating operations (e.g. multiple EHRs, management structures)

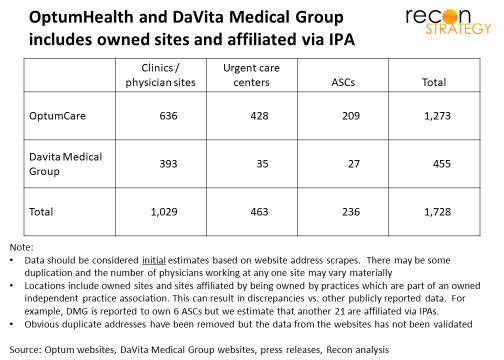

In short, the DMG acquisition is a classic horizontal play. And the assets coming from both sides are significant (note: rough numbers given complexity of IPA footprint):

What will be the impact of adding the two together on OptumHealth’s market position?

Limited expansion of geographic reach

To assess the growth in reach, we added the DMG sites with those currently belonging to OptumHealth. Our analytical approach was this:

- Add the DMG sites (including IPA affiliated locations) to our database of OptumHealth locations based on addresses listed on the DMG website

- Identify how many health care markets regions (one of the 3,500 or so Hospital Referral Regions defined by Dartmouth Atlas) had one type of care (e.g. clinics), two types of care (e.g. clinics and urgent care or clinics and ASC’s) or all three types of care (clinics, urgent care centers and ASC’s)

- Weigh those regions by their population and estimate the share of population with in-region access to legacy OptumHealth or DMG.

We want to understand where OptumHealth has two or three different care models active so we can gauge the potential for cross-referrals across settings — which can improve market share, business economics and support a value-based care advantage.

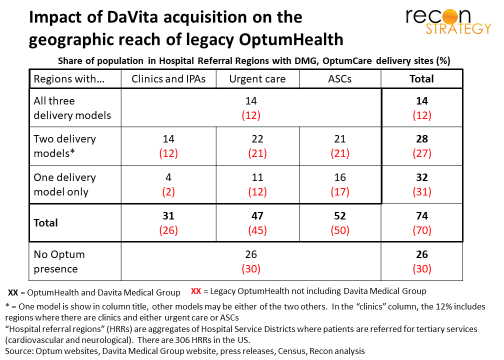

The exhibit below summarizes the analysis (new combined numbers in black, legacy OptumHealth only numbers in red):

We had estimated that 70% of the US population has access to (= lives in a region with) some type of legacy OptumHealth care and 12% has access to all three types of legacy OptumHealth. Adding DMG did not change this much: 74% of the US population has access to new OptumHealth and about 14% have access to all three modes.

Significantly increased density in existing geographies

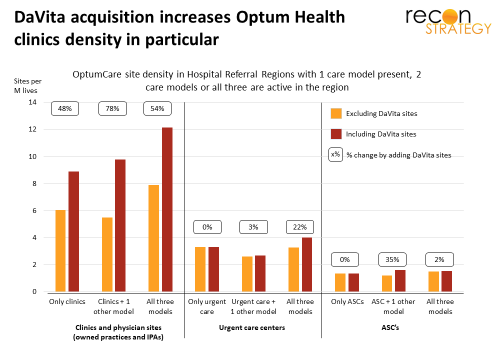

DMG is a large business and, to the extent it can be squeezed into the same geographic envelope as legacy OptumHealth, there must be a substantial increase in density. Indeed, this is what we find, particularly with physicians and clinics towards which DMG’s clinical portfolio is heavily weighted.

One metric to evaluate density is number of sites per million inhabitants. It is a rough metric for several reasons but the distortions will be similar across DMG and legacy OptumHealth so we can use it to assess changes in density. The more sites per million lives, obviously, the more dense the delivery network. The exhibit below shows the results within those Hospital Referral Regions where DMG and OptumHealth are active:

Strategic value

Higher density (especially in clinics) yields multiple advantages, but only for an entity with the management and operational structures to exploit them:

- Better ability to exploit cross-referral synergies (more site locations means more convenient options for referring patients and a higher capture rate or a larger referral base upon which to build a business plan for a new care site)

- Greater scale to cut fixed operating costs (e.g. marketing) or fixed investments (e.g. care management technology)

- Greater mindshare with payers and provider partners, thereby getting better business terms (e.g. value-based reimbursement deals, optimized referral paths).

The major impact of the DMG acquisition is to sharply increase the clinical presence in OptumHealth markets. This probably yields a better balance across care delivery models (more clinics needed to support referrals to a set number of ASCs, and more clinics needed to receive referrals from a set number of urgent care centers) and greater strategic independence.

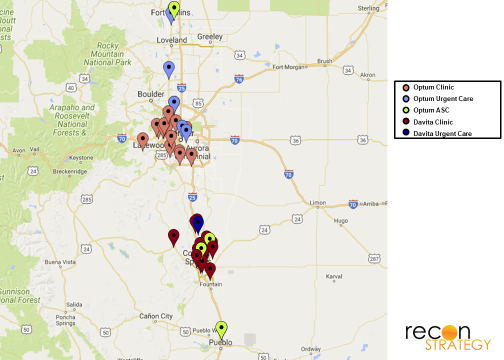

For example, take a look at the map below of Colorado:

From the map, we can see that OptumHealth had a strong position around Denver with clinics and urgent care centers. Its ASC’s however were located mostly south of Denver in Colorado Springs and Pueblo without any nearby clinic or urgent care assets. By adding DaVita, however (which acquired a number of primary and specialty practices in the Colorado Springs area), those ASCs are now surrounded by a large number of potentially referring physicians with no ties to the local hospital systems.

Conclusion

DaVita had been struggling with its DMG business for a while, with missed earnings expectations and analyst complaints. Some might argue that the underlying DMG business was flawed and that Optum overpaid with the $4.9B acquisition price.

But the business will clearly be worth a lot more in Optum’s hands than other potential acquirers:

- Scale up value from the combination of closely aligned footprints

- New synergies with the UNH insurance business unavailable to DaVita

- Some pre-existing alignment on EHR strategy which should also ease integration: Optum is standardizing on Allscripts Touchworks (motivated, I suspect, by Allscripts willingness to accommodate Optum software and by Optum’s unwillingness to incur a dependency on Epic). Large portions of DMG also appear to operate on Allscripts (e.g., DMG’s 2013 plans to expand a nationwide partnership with Allscripts by rolling out the EHR to its California sites). This is not to say there won’t be some heterogeneity (e.g., DMG’s The Everett Clinic uses Epic) but perhaps less than with other potential acquirers.

As long as Optum negotiators did not pay much of a premium over what other buyers would pay, the price was probably very good value for Optum.

And now the Optum Health’s threat to incumbent hospital-centered provider systems just got a lot more intimidating.