Last December, UPMC announced plans to spend $2B on three new specialty hospitals in downtown Pittsburgh. Each will abut an existing UPMC hospital currently serving as system center of excellence for the particular specialty: cancer will be located near Shadyside; cardiac and transplant near Presbyterian; eye and rehab near Mercy. Given inpatient’s declining share in care delivery, any new hospital construction in an over-bedded market with slow-moving demographics is a curiosity. Even if, as UPMC has promised, no net new beds will be added to the market, the new hospitals will still add fixed cost and reimbursement uncertainty (acceptance of status, contracting rates from third party payers).

Specialty hospitals in general have several potential strategic rationales but none seem to offer upside worth a $2B bet for UPMC. Let’s pressure test three below: (1) operating synergies from consolidation, (2) local market share gain, and (3) broader regional draw of patients. (See note at the end of the post for data and methodology).

Operating and clinical synergies

Consolidating care into a single operation can yield efficiencies in staffing (e.g. enabling greater disease-specific specialization among nursing staff) and more effective use of equipment. Given the well-documented importance of case volume as a driver of clinical quality, consolidating care into a single operation should also improve outcomes.

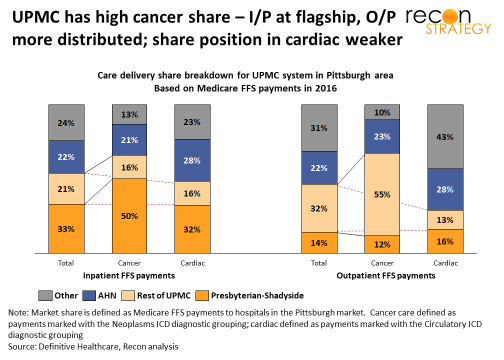

But UPMC already has consolidated volume in its centers of excellence for each disease: 83% of inpatient cancer care and 66% of inpatient cardiac care which UPMC provides in the greater Pittsburgh region is concentrated in either Shadyside or Presbyterian. There’s more room to consolidate outpatient care (e.g., only 17% of UPMC’s cancer in the Pittsburgh region is done at Shadyside/Presbyterian) but it is not clear why patients would want to go downtown for this care given that much of it is routine (e.g., infusions) or whether the hospitals affiliated or partnered with UPMC currently providing this care would be willing to see those economics transitioned out of their systems.

Local market share gain

Building a specialty hospital can signal commitment to high quality care and deep knowledge of the latest research and technique. But UPMC already dominates that brand positioning in Pittsburgh: US News and World Report has Presbyterian/Shadyside at #1 in the Pittsburgh market, #2 in Pennsylvania and nationally ranked in 14 specialties (including cancer and cardiac) and high-performing in 8 conditions. Direct competitor Allegheny General is #2 in Pittsburgh but #18 in Pennsylvania as a whole and ranked high performing in just 4 procedures (and shares the #2 ranking with UPMC St. Margaret). There’s no need for a set of specialty hospitals to differentiate on clinical sophistication. (AHN is not standing still on cancer but investing much less and that in distributed ambulatory sites — e.g., $80M for a new cancer institute at its flagship hospital in Pittsburgh and $140-150M on regional ambulatory sites.)

Furthermore, in cancer, at least, there is not that much share left to gain. UPMC already has 66% share in inpatient and 67% in outpatient cancer care delivered in the Pittsburgh area. Much of the remainder is with the Allegheny Health Network (AHN) and, given the highly supportive network designs of AHN parent Highmark, will be hard to pry free. While there appears to be some share gain opportunity in cardiac outpatient (43% of care is delivered by “non-aligned” systems), we suspect a lot of that care either lacks the severity for downtown to be appropriate or is too acute to wait until a patient can be transitioned downtown (e.g. stabilization).

Regional market share gain

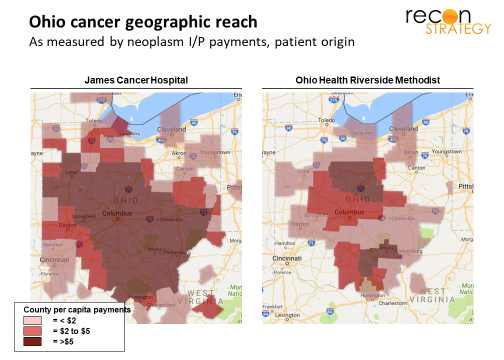

By consolidating expertise and offering advanced techniques, specialty hospitals can attract patients well beyond their local market and the typical patient pools their affiliated systems treat. For example the James Cancer Center based in Columbus is able to draw patients from across all of Ohio, well beyond the reach of either its Ohio State University affiliated system or its local cancer competitor, OhioHealth Riverside Methodist. See the maps below which show county of origin for inpatient cancer care for these two systems for 2016 Medicare FFS patients:

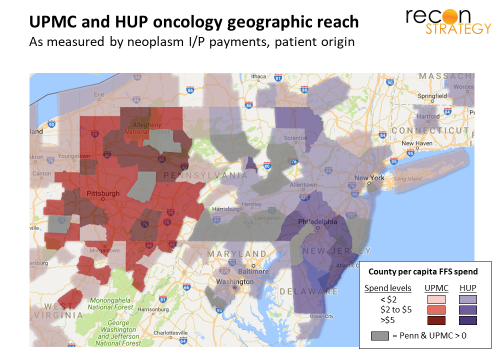

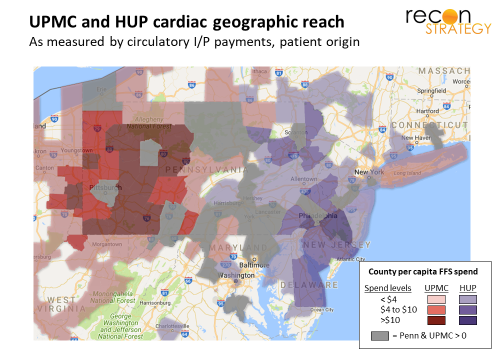

But here again, the potential upside for UPMC’s specialty hospitals appeared tapped out. UPMC already draws cancer and cardiac patients from all of western Pennsylvania and western New York, as well as central Pennsylvania and northern West Virginia. While it is possible to imagine specialty hospitals drawing patients from greater distances (as, for example, Baylor Heat Hospital in Plano does though, in general, everyone seems more willing to travel great distances in Texas), it is hard to see how much further UPMC could reach given that it is bracketed by the James and Cleveland Clinic in the west and Penn Medicine on the east.

Are the hospitals part of a nationally-scaled bet on precision medicine?

The three new specialty hospitals will certainly create some operational efficiencies as well as local and regional share gain. But, even when combined, the potential upside hardly seems worth a $2B bet at a time when local demographic trends are flat and its debt is being downgraded (from Aa3 to A1 with a negative outlook in September 2017 because of the aggressive eastward expansion into central Pennsylvania).

One alternative strategic rationale is that the new hospitals will help UPMC compete beyond its broader regional environment — in other words: nationally (and perhaps beyond). But how could that work, boxed in as UPMC is now with Cleveland Clinic and the James in the west, Penn Medicine in the east, Johns Hopkins in the south and Lake Erie to the north?

No one has accused UPMC of lacking ambition. When UPMC CEO Jeffrey Romoff announced the $2B plan, he said “UPMC desires to be the Amazon of health care.” The implication would be that UPMC plans to break down traditional geographic market limitations and drive disruption with technology

Research has always been at the heart of Romoff’s growth strategy for UPMC dating back to his early days converting Western Psychiatric from a psychoanalytical backwater into a leader in research on the biomedical basis of mental illness (recall that Western Psychiatric eventually became the heart of the UPMC behemoth). The hottest trend in medical research today is discover and elucidate genotype-phenotype-therapeutic response associations – something that requires mountains of high-quality, highly -consistent data (much more than is available in UPMC’s western Pennsylvania hunting grounds).

Considering the three hospitals part of a long-term strategic bet on precision medicine and a St. Jude’s model of medical tourism could make sense for several reasons:

It would explain the scale of investment: Precision medicine is making the linkage between research and care delivery more immediate. That will naturally increase the value of co-location of research and clinical operations. While $2B is a lot to spend on hospitals, it is a reasonable amount if facilities will combine care delivery beds and space for research. Furthermore, using shiny new facilities to lure leading researchers is a well-tested approach.

It would also point to the upside: When therapies can be tailored to a particular patients’ disease profile, it can make a lot more sense for patients to travel greater distances to access that customized care in an evaluation and treatment design episode and then return home for follow-on care. Interestingly, UPMC described the new hospitals as “digital hospitals” and Microsoft figured prominently in the announcement as a key partner in the design. That can mean anything, of course, but if you were going to build a hospital that would treat patients across the country before and after an episode of care, you would want a strong digital and telemedicine capability built into the infrastructure. Further, providing precision medicine to a national patient pool would certainly allow UPMC to break out of its Pennsylvania “box” by leapfrogging over big nearby competitors.

If this hypothesis is correct, we would expect to see a few things in the coming years:

- In the near-term, UPMC will raid other academic centers of any expertise in precision medicine in the three specialties and a build out of other supportive infrastructure (by the way, we have already seen a major investment in research in immunotherapies with a $200M joint venture with the University of Pittsburgh announced in mid-February this year).

- In the medium term, UPMC will break from its traditional strategy of building end-to-end affiliations with geographically contiguous systems and, instead, start forming specialty-specific and potentially looser alliances with systems outside the Pennsylvania “box” (comparable to geographically dispersed alliances formed by top 10 cancer centers and the Cleveland Clinic’s Heart Institute). These alliances will provide access to the patients needing UPMC’s precision medicine solutions.

Anybody want to take a bet on whether that’s what we will see?

Tory Wolff

Managing Partner

Tess Niewood

Associate Consultant

Quick methodological note: Unless otherwise noted, the patient volume data discussed below is drawn from Medicare FFS payments in 2016 provided by Definitive Healthcare. Cancer care includes claims classified in the Neoplasms ICD diagnostic grouping and cardiac care includes claims in the Circulatory ICD diagnostic grouping. (Data for eye and rehab in the FFS data set were too few for reliable analysis). Medicare FFS payments have generally comparable rates across provider participants so good proxies for volume and are free of health plan network designs, so good indicators of physician and consumer habit. However, Medicare FFS data may not reflect share among patients with commercial coverage, greater resources who may also travel further for preferred care.