Why would a health plan want to buy an exchange? Isn’t the only synergy if the owning plan tilts the exchange in their products favor? And won’t that damage the value proposition of the exchange for buyers and see them flock elsewhere?

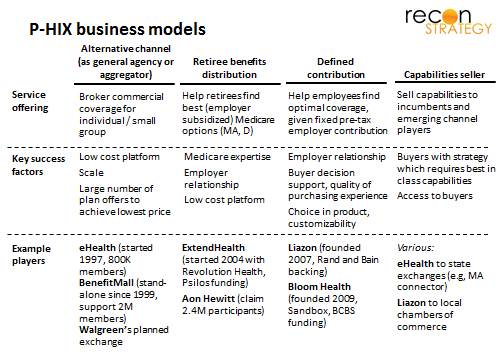

To understand the Bloom Health acquisition, it is important to recognize that the private health insurance exchange (PHIX) space is quite fluid, consisting of three or four distinct market opportunities. (The fourth — capabilities resell — might not really qualify as a PHIX specific opportunity, it is more a readily accessible adjacency):

The models run a spectrum from acting as a “commoditizing” transaction facilitator (with no particular intimacy with either buyer or seller but a lot of participants to facilitate low price) to helping employers transition their employees to a radically different model of thinking about health benefits (focused on: minimizing the potential blow back from perceived benefits reduction with a compelling array of decision support, buying experience quality, and choice among benefit design alternatives). (Retiree benefits sit somewhere in the middle because the employer relationship is important but the products are more standardized than in the defined contribution world). Because the capabilities across service offerings are very different, it seems to have been hard for one player to pursue all of them.

The PHIX model started with the channel play (note late nineties start dates for eHealth and BenefitMall) and that is where the bulk of the business remains: Assuming eHealth, BenefitMall and other players numbers can be taken at face value (so adding up to 3-3.5M or so lives) and that the vast majority are in the individual and small group markets (together ~23M lives), that would imply a 13-15% penetration – not small but clearly a segmented appeal. This channel model is likely to grow further under reform, however, given MLR floors putting pressure on broker business models (therefore favoring large scale, web based sites or piggybacking off of other distribution partners – think of Walgreen’s recently announced plans to launch a PHIX — vs. fragmented store front operations). Also, the state exchanges may end up persuading consumers to adopt self-sourcing but fail to deliver on an adequate breadth of offer or a quality consumer experience, driving people to private exchanges. In that sense, the channel PHIXs will compete head to head with the state exchanges.

But reform will also stimulate interest in defined contribution for several reasons:

- Employers are running out of alternative ways of controlling costs (having trimmed benefits to the bone in small group already)

- Reform will add to cost with the minimum benefits standard and risk pooling. There are also other less direct drivers of cost growth such as industry taxes and provider cost shifting etc. as well.

- Employers are encouraged in parts of the legislation to think about their contribution as being more “fixed” – e.g. the vouchers they can provide employees to purchase on the public exchanges under special circumstances, or the looming Cadillac tax which will encourage employers to provide coverage up to the trigger level and no more.

Defined contribution is a nice way-station between defined benefit and opting out (and health plans would like to hold groups in there rather than let their lives migrate into the likely intensely competitive individual market). But it requires a major shift in the expectations of employees – it is more radical than shifting to consumer directed / high deductible plans. There are two possible endgames we see for defined contribution PHIX models, the insurer-led and the channel-led approach:

Going back to the questions posed as the beginning: The acquisition of Bloom Health by Wellpoint, HCSC and BCBSM fits with the insurer-led endgame: “tilting the table” toward Blue products matters less in a defined contribution setting. In fact, a locked-in relationship between a health plan and the defined contribution exchange enables more tailored offerings for the specific employer population and reduces anxieties about adverse selection (since the whole group is committed to one insurer).

Aon Hewitt’s plans to offer a commercial PHIX for large employers on its retiree exchange platform fits with the channel-led endgame. No custom fit here: products will be classified using health reform’s “precious metal” categories. Until more details are released, it is unclear how Aon Hewitt will address employee education in the context of many different carriers and products or adverse selection (e.g. with similar benefit designs, if one product has a more open network, it may attract a sicker portion of the employer’s pool).

It is not clear which of the two endgames will be realized. Critical will be the extent to which insurer-led PHIXs can exploit the vertical integration to create a positive value proposition for defined contribution so that more employers think they can adopt the model without too much push-back. Presumably they are pretty confident since one of the Bloom buyers (BCBSM) has been testing the model out starting in July 2011 (with the “GlidePath” product) and they went ahead with the purchase.

Other observations:

- The price for Bloom was probably not that high (the actual figure hasn’t been released): one of the likely learnings from the BCBSM pilot was that health plan integration was critical to creating the degree of customization required to appeal to employers (hence the purchase). But the inverse implies that Bloom’s stand-alone potential for market penetration wasn’t that great. Besides, its revenues (guessing in the $4-5M range based on $15 PMPM fee and 25K lives) were modest and technology was vended from ConnectYourCare (implying easy replicability had the investor chose to forgo the acquisition)

- Wellpoint sharing the acquisition with two leading non-profit Blues (HCSC and BCBSM) signals two things: first, the Blues utility model is alive and well and second, it was important for there to be non-profit participation (even if Wellpoint owns 78% per press reports) in order for the rest of the Blues system to feel more comfortable using a capability from the for-profit Wellpoint.

- The defined contribution model for small group represents an interesting addition to the potential emerging solution set: the other two being small group ASO (a la CIGNA) and narrow networks (a la Steward-Tufts). (Of course, defined benefit models are attractive to large group as well: but large group has had access to ASO for a long time and local narrow networks are probably less appealing to large group looking for consistency in benefit design across states).