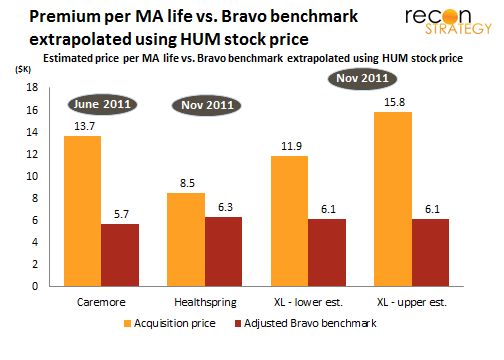

Several recent acquisitions suggest a rapidly growing valuation on Medicare Advantage (MA) lives. Last August, Healthspring paid about $3.6K per adjusted MA life with its acquisition of Bravo. (My adjustments extract the value of the PDP lives using the CVS acquisition of Universal American PDP lives as a benchmark and for the share of Special Needs Plan or SNP lives which typically have higher utilization levels and higher reimbursement). This past November, there were two major MA acquisitions, both with sharply higher prices. Cigna (CI) bought Healthspring for $3.8B — $8.8K per adjusted MA life or about 2.5x what Healthspring paid for the Bravo lives. The anticipated price for XL Health (bounded between $1.5 to $2.0B per press reports) implies that United (UNH) is paying somewhere between $11.9K and $15.8K per adjusted MA life which is 3-4x the price per life just 15 months earlier. Can stand-alone MA plans looking to exit the market expect this kind of pricing to hold? Short answer: No. Recent pricing has been capability driven. Plans with just lives (no special capabilities) to offer won’t have much leverage to match recent pricing. The Bravo price point is still probably the best benchmark for stand-alone MA lives.

Now, there is good reason why the market is valuing MA higher over these days vs. a year or so ago. For a variety of reasons, health care reform increased the value of scale in MA, creating real synergies for consolidators able to add meaningfully to their book. And, although health care reform was supposed to sharply reduce funding for MA plans ($6B out in 2012), a major CMS demonstration on star ratings bonuses has added a lot back to MA funding for the next few years ($3B for 2012 — see an excellent report on this from Kaiser here). Coupled with the expanded eligibility for bonuses to include plans with 3 stars, plans are expected to receive an additional $280 per enrollee in 2012. Humana’s stock price – heavily dependent on its senior business and therefore probably the closest to a clean pure play price — has gone up roughly 70/80% since August 2010.

But there is still a huge gap between recent acquisition prices and an extrapolated value of stand-alone MA lives (using the Bravo benchmark and updating with the Humana stock price) suggesting a rising acquisition premium. Below is a comparison of recent per MA life acquisition cost vs. the updated Bravo benchmark.

In each of these acquisitions, there is more than just the lives as stake driving the valuation:

In each of these acquisitions, there is more than just the lives as stake driving the valuation:

Caremore: In addition to the MA lives, Wellpoint also bought the provider system that managed the primary and much of the specialty care for the enrollees. Assuming there was a healthy margin due the care provision (implied by the high praises sung about the model), there is a logic that says $13.7K per life works.

Healthspring: The combination with CI created a marketing cost synergy (from transitioning CI age-ins into an MA plan) and maybe enhanced CI’s DTC sales capability across the commercial book (as already noted here, I am a bit skeptical of how much new value can be created by Healthspring alone in turbo-charging CI’s provider engagement strategy). A sharply increased growth trajectory enabled by special access to CI’s 275K Medicare age-ins each year (assuming 2.5% of their 11M members become Medicare eligible in any one year) could explain a large part of the acquisition premium.

XL Health: Neither of those synergies applies to the UNH since they already have a very strong MA presence. The story described at UNH’s investor day meeting was one of capabilities: Two capabilities were identified as being distinctive vs. UNH’s legacy: XL Health’s ability to (1) visit all their members in the home to build get a very clear clinical picture of what is going on and (2) leverage a highly integrated platform for managing the care and getting reimbursed. Assuming the updated Bravo price per MA life reflects the stand-alone economics, United paid about $775M for the lives and the remainder (between $0.7B and $1.2B) for the capabilities.

Implication for stand-alone MA plans looking to exit: don’t use these most recent benchmarks to set your pricing expectations — unless you also have something very special beyond just the lives to offer the buyers.

A closer look at United’s premium for XL Health

Is $0.7B-$1.2B a reasonable price to pay for XL capabilities?

Could be, though the corollary is that UNH’s legacy medical management is leaving some significant dollars on the table. Putting some context on this: Right now, UNH has about 400K lives in MA in XL Health’s operating states (AR, GA, MD, MO, SC, TX), and another 300K lives in states where XL Health is planning on expanding next year per recent press releases (IL, IN, IA, NM, NY, WI). Assuming the capability premium should be amortized across these lives (that is, XL Health will reduce the medical cost of the legacy UNH lives in these states), UNH is paying $1.0K to $1.7K per life for the capabilities.

If UNH is seeking to get its investment back over, say, 5 years, XL Health capabilities would need to reduce medical costs (or improve reimbursement through better documentation) by 2.0%-3.5% over their entire MA book in these states. Of course, it may be that XL Health’s capabilities can be leveraged in more geographies in the next 3-4 years or may help with UNH retirees outside the MA program. However, the XL model seems premised on an in-home visit feeding the platform. Those sorts of networks take some time to develop and perfect and the expansion plans UNH has already laid out for XL are aggressive as it is (6 new states).

The other potential story may be around dual eligibles. There is a pretty large overlap between Medicare/Medicaid dual eligibles and other members in chronic disease SNPs (XL’s specialty). There is certainly a lot more interest in Washington these days and among the states to push forward on initiatives to better coordinate the care of dual eligibles. A home visit model like XL’s could also have a big impact on this vulnerable population. But that also implies that UNH’s Evercare (the largest player among duals with 170K lives) is somehow under-managing its target population. Also, there is not a lot of overlaps between the 15 states that have projects approved by the Federal Coordinated Health Care Office in CMS and the ones where XL is currently active or expanded (the 15 states are CA, CO, CT, MA, MI, MN, NY, NC, OK, OR, SC, TN, VT, WA and WI – overlaps with XL current or future target states are NY, SC and WI).

Fact is that any small percentages value creation (2-3% off medical cost) multiplied out over any large enough base can add up to a big number. Since UNH reduced its chronic disease SNP business last year, they probably have a good idea of what constitutes an impressive capability and properly value what XL has to offer. But making sure they make good on this investment will be very hard to track in a dynamic environment (with different baselines among legacy UNH vs. legacy XL lives and new programs and strategies being continually added to the mix).

Further, a few days after the XL announcement, Humana bought Seniorbridge (a home health player with $72M in revenues) for presumably a lot less than the premium UNH paid for XL. Of course, Senorbridge is not XL Health. But Humana’s acquisition hammers home the point: When you want capabilities, it can often be cheaper to just buy the capabilities rather than the paid the full freight of the associated lives. Of course, it also helps if you are not in a public bidding war against several well-funded rivals (it was reported that Aetna and Wellpoint were interested in XL as well).