Correctional health and correctional pharmacy

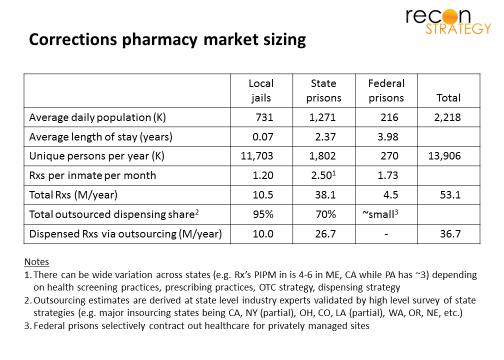

2.2M people are incarcerated in local jails and state and federal prisons at any one time in the U.S. for whose healthcare various government agencies are responsible. This aggregate number hides some important segment differentiation (see table).

Local jails are housing a little over 700K on any average day but typically for a short period of time (on average a month or less), implying over 11M people flowing through the jail system in any one year (boldly assuming few repeated tours). Less than a month is relatively little time to identify and begin treatment of significant health issues. Accordingly, this population receives only about 1.2 Rx per inmate per month (PIPM).

Federal prisons house over 200K prisoners with much lower churn (serving an average of 4 years). While there is plenty of time to identify and begin treatment of health issues, consumption of Rx’s appears low with an average of 1.7 Rx PIPM. Perhaps this is because of the demographic “selection bias” driven by what constitutes a Federal vs. state crime (e.g. more white collar crime, etc).

State prisons hold the majority of the incarcerated with 1.3M prisoners serving an average of 2.4 years – more than enough time for a pre-arrest life of poor health choices and poor healthcare to bloom into serious issues: serious infections (Hep-C, HIV, TB, STDs) comorbid with the “classic” physical chronic conditions and mental health / substance abuse issues. This population we estimate conservatively at 2.5 Rx PIPM. (Some states complain of much higher numbers – upwards of 4 to 6 Rxs PIPM, as a result of purported overutilization as well as different dispensing strategies such as dispensing shorter duration scripts more frequently and dispensing OTC-eligible drugs on a prescription.)

Delivery models

Agencies have chosen among four main ways to provide healthcare to these prisoners (see table):

The model governments choose depends on a lot of factors. Scale of operations, risk tolerance, clinical philosophy and (inevitably) politics all play a role, but they do not follow a simple pattern. For example, the three states with the largest prisoner populations – California, Texas and Florida – have each chosen different paths. One key element appears to be conservatism: several states have endured legal challenges and public embarrassment at the quality of care delivered but stuck to their preferred model (at most switching out vendors).

Prison health care has many unique requirements for vendors, among them:

- Ability to stand up an onsite provider practice quickly upon winning a contract and recruit physicians and nurses for service in uncomfortable settings

- “Muscular” approach to primary care that integrates behavioral and treats at the outer edges of what can be done in the prison infirmary before referring out to specialist or facility care

- Population health model that manages a high risk, demographically diverse population to very tight budgets (a function of the political unpopularity of this government responsibility)

The peculiarity of these requirements coupled with the innate conservatism of state policy makers has resulted in a vendor set that is small, long-standing and highly specialized: the major healthcare service players are Corizon, Correct Care Solutions, Wexford Health Sources and, more peripherally, NaphCare, Armor and a number of local players. Pharmacy vendors are similarly focused with Diamond Pharmacy in the lead with about a third of the market, followed by Maxor (which may be exiting the market), Correct Rx, PharmaCorr (subsidiary of Corizon and frequently bundled into the contracts) and Contract Pharmacy Services.

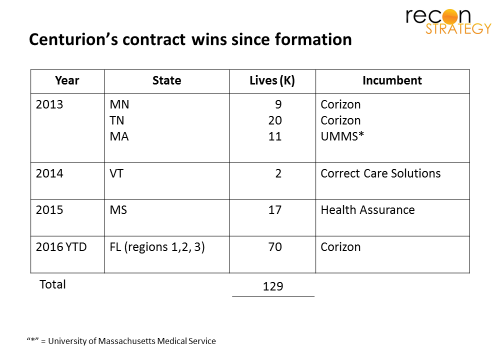

A new entrant rapidly takes share

Since 2013, a joint venture formed by Centene and MHM, a national provider of mental health services in corrections has been winning a series of contracts from leading incumbents, most prominently the Florida contract win for 70K lives announced on February 1st (for comparison, long-standing incumbent Corizon has about 320K prison lives in their care at this time):

Why has an effectively new entrant been able to rack up 130K lives over three years in what is a very conservative market?

The joint venture offers a powerful combination: MHM brings deep experience in mental health for this highly afflicted population, but also a channel because of its long-standing relationships with state and local corrections departments. Centene brings its overall managed care capabilities and extensive provider network relationships in the “free world” (outside of prisons). (Notably, Centurion does not seem to have a preferred pharmacy vendor at this point and works with several incumbents.)

The most recent Mississippi and Florida wins also hint at an additional asset: Centene’s Medicaid strengths. In both those markets, Centene is a major managed Medicaid plan with large memberships and significant state share. Given the ACA’s expansion of Medicaid beyond the “classic core” (young mothers with children and the disabled), the vast majority of released prisoners are likely going to be eligible for health benefits. There are some narrow business advantages for Centene: Many of them can “parole in” to a Centene plan (or, if they don’t qualify for Medicaid, former prisoners have 60 days to sign up for an Exchange plan. Release from prison is, among many other things, a qualifying event).

Further, after treating the prisoners on the inside, Centene will have a very good idea of the key health issues to ensure a full risk adjustment argument. However, there is also a broader advantage: detailed knowledge of the health states of prisoners prior to release can be critical ensuring proper post-release care management. Good quality healthcare – and, in particular, keeping them compliant on mental health medications – can be a key strategy to reduce recidivism. Housed within its extensive specialty subsidiary family, Centene has strong pharmacy-related capabilities (US Medical Management PBM, AcariaHealth for specialty/Hep-C). By not letting released offenders fall through the cracks, Centene should be able to make a synergistic argument to state budget authorities regarding managing the “lifetime” cost of prison-exposed populations – an approach to the cost of prison care reminiscent of Eisenhower (“Can’t solve a problem, enlarge it”).

It will not be an easy pitch to make: state budgeting is notorious for siloed thinking (and corrections departments are not necessarily making themselves popular with state Medicaid authorities for pushing the boundaries of eligibility for prisoners before being released (e.g. for specialty care that takes place outside of the prison). Centene may need some time to demonstrate how this works in Florida and Mississippi before being able to roll it out elsewhere.

If Centurion can build the case, the next steps in the strategic plan seem clear: of the ten states with the largest incarcerated populations, Centene has a sizeable base of “free world” lives in six of them (California, Texas, Florida, Georgia, Ohio, Illinois). It won’t be easy: California has stuck with its insourced model despite extensive litigation and court ordered independent oversight; Texas and Georgia’s commitment to the state university systems for prison healthcare delivery is long-standing. But a lifetime care management strategy for offenders coupled with long-standing credibility with state Medicaid authorities might just enable Centene to change the models.