Warburg Pincus, the new majority owners of CityMD, a 68 site urgent care chain, will need to bring plenty of capital to an urgent care industry approaching its endgame. CityMD competes on a national stage against the likes of TPG’s Access Clinical Partners and UnitedHealth’s MedExpress. And rapid shifts in individual markets are raising the strategic stakes: where once urgent care could remain independent, today it is increasingly being asked to take sides in the share battles among big delivery systems. In November 2016, for example, Banner completed its acquisition of 32 sites in Phoenix and Tucson and earlier this year, Ochsner acquired 16 centers in New Orleans.

Why is this happening? Urgent care provides low cost, low acuity, convenient care. But a portion of its patients — high-acuity patients in need of an ED, patients with newly identified specialist care needs, consumers lacking a primary care relationship – generate a flow of referrals and script filling opportunities. Because urgent care tends to disproportionately serve commercially insured patients, this referral volume can be economically attractive. The aggregate margin on this referred care can easily exceed the aggregate margin on the broader urgent care volume that generates it.

Given the low-acuity, transactional patient relationship, urgent care providers could operate as a strategically neutral triaging utility for big delivery systems in a market. As long as these referrals are distributed in an even-handed way (e.g. relying on patient preference or objective algorithms such as geographic proximity), urgent care doesn’t pose a threat.

Yet, as urgent care patient volume grows, the temptation to softly steer these flows to a specific in-network provider can become irresistible. And once one competitor starts tilting the referral flow, other systems are compelled to defend themselves in an urgent care arms race. CityMD’s home urgent care market became such a battleground among the big New York systems over the last few years.

Northwell’s game changing move

Until 2014, the major New York delivery systems appeared largely content for urgent care to remain in the hands of independent chains, independent physician practices and a long tail of single-site operations. Some delivery systems set up a handful of urgent care centers typically located within their existing catchment area and designed more to ease pressure on their clinics for after-hours care and EDs for low acuity care rather than as a market share play.

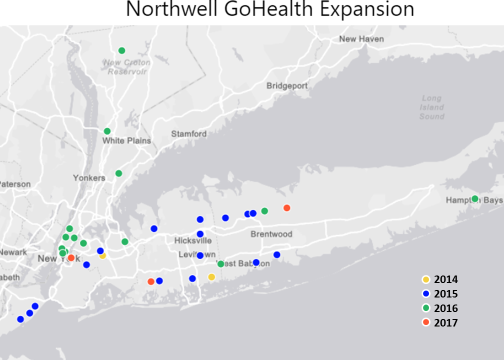

That all changed in 2014 when Northwell (formerly Northshore-LIJ) formed a partnership with Access Clinical Partners (dba GoHealth), a TPG-backed urgent care network builder focused on joint ventures with provider systems. The alliance launched a rapid roll-out of urgent care centers both within Northwell’s traditional Long Island market and building outsized beachheads in other markets. They are targeting to have 45 centers by the end of 2017.

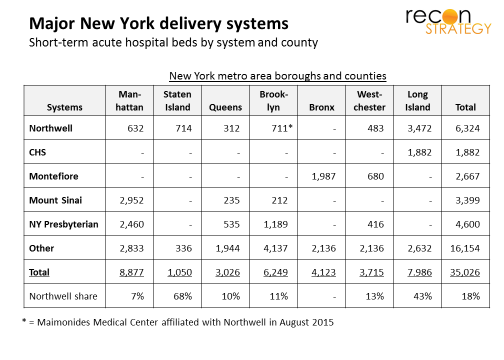

In several major markets, Northwell’s outsized urgent care share relative to its hospital bed share looks like a share grab. In Queens, GoHealth has 6 urgent care sites or 14% of the market but only a 300 bed hospital (10% of the short-term acute care beds). And in Manhattan, Northwell has just 7% of the beds but 16% of the urgent care centers.

The map is instructive: GoHealth sites are systematically closer to Mount Sinai hospitals (average 1 mile away) than Northwell’s Lenox Hill Hospital (average 2.6 miles away). The aggressive push seems not to have been mistake-free: Northwell managed to surround its Manhattan free-standing ED with three urgent care cetners which must be cannibalizing volumes.

Options to countering Northwell-GoHealth

How can the other delivery systems respond to Northwell opening a new competitive front in urgent care?

Greenfield was not really viable. Many sub-markets in New York are near saturation. Typically, 40-60K people generate enough minor-acute care episodes to keep an urgent care center profitable. Currently, there is one urgent care center for every 35-40K people in Manhattan and Staten Island, one for every 30K people in Westchester and one for every 25K on Nassau (Long Island). Being at these saturation points means that few prime locations are obtainable and the available economics are not attractive.

Acquisition was likely out of reach given expectations on multiples established by United’s acquisition of MedExpress and the limits on uncommitted capital at the delivery systems. Further, urgent care networks with ideally configured footprints are few and trying to stitch together a cohesive network from a number of single sites and small chains can be an intimidatingly complex exercise.

Alliance clearly seemed like the best choice. But with whom?

CityMD abandons strategic neutrality to become a strategic partner

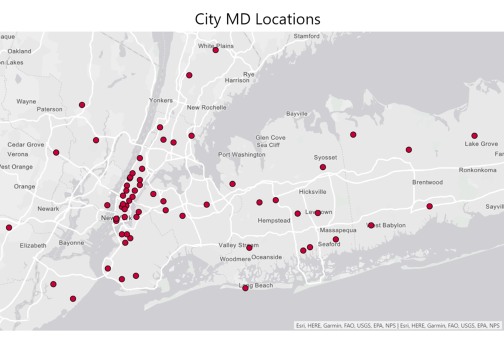

CityMD is the largest urgent care chain in the New York metro area and best positioned. And, CityMD appears to have reached a positive conclusion about the value of alliances with big provider systems. Logically enough: CityMD would not want the big systems to become competitors. An alliance can also preempt potential entrants (say MedEpress) from using delivery system alliances as springboards. Further, the New York systems in general are planning aggressive capital construction initiatives ($6.3B over the next 2 years per reports) including outpatient clinics. Better to have the planning for that spend assume the CityMD sites are “friendly” than competitive.

The problem for any one delivery system is that CityMD covers the entire metro area while the delivery systems (with the exception of expansive Northwell) are each focused on specific boroughs and counties.

CityMD’s strategic innovation was to slice up its network and form strategic relationships with the locally incumbent provider for each slice. It had already experimented with this approach when it opened a new market in New Jersey via a partnership with Hackensack University Health Network (3/2014). But now, CityMD rapidly lined up partnerships with CHS in Long Island (7/2016), Mount Sinai in Manhattan (12/2016) and, most recently, Montefiore in the Bronx and Westchester (3/2017). As a result, they have effectively matched the Northwell GoHealth network with their own delivery system alliances.

CityMD’s alliance model vs. Access Clinical Partners/GoHealth joint venture model

In these alliances, CityMD appears to retain full ownership, staffing and branding of its sites. By and large, the relationships are not described publicly as exclusive. The partnerships are primarily focused on enhanced referral relationships. In the case of Hackensack and Montefiore, joint growth initiatives also appear to be part of the deal (especially in Westchester with Montefiore – the only relationship that is publicly described as exclusive).

Time will tell if CityMD’s delivery system partners get enough value in the relationship without co-branding or if they see the alliances as just temporary fixes pending the full weight of their anticipated facilities investments coming online. The delivery system expansion strategies may also froce choices: For now, CityMD’s partners operate more or less in isolation (Manhatten, The Bronx, Long Island, New Jersey) but as they grow, they will start competing with each other. CityMD could try to stay neutral in the contested markets and they may have the leverage (location ubiquity, customer loyalty) to reuqire it. But the delivery system partners may then start looking for alternatives.

In the meantime, CityMD will be facing more challenging capital demands than Access Capital Partners while vying for a similar national scope (besides the Northwell relationship, Access Capital Partners also has joint ventures with Legacy in Portland and Dignity in San Francisco. CityMD recently formed an alliance with CHI in Tacoma). The joint venture model allows Access Capital Partners to share capital costs with its partners (and allows the provider partner to access capital for network growth while keeping control of the referral care economics). CityMD most likely funds its sites by itself. Hopefully, the Warburg Pincus investment was not all spent funding shareholder exits so enough remains to support growth.

Leapfrogging physical infrastructure with telehealth?

As provider systems and urgent care networks select dance partners, inevitably some players are left standing – perhaps because they did not want to join: developing an urgent care network is not the only way to respond to Northwell’s strategy.

So far, NY Presbyterian (NYP) – as exposed to Northwell’s urgent care strategy as Mount Sinai — has not publicly announced any material urgent care deals. In November, 2016, however, they announced the launch of an online service in collaboration with American Well (“Digital Urgent Care”) by which patients can connect with an NYP emergency physician and either be treated or triaged. The initiative is part of a more general effort by NYP to create online access to the health system.

There’s a strong overlap between the telehealth minor acute care scope and what can be done in an urgent care setting (big exceptions would be any episode requiring labs, an x-ray or a procedure such as a simple fracture). While telehealth still lags urgent care in consumer uptake, the adoption curves are not that widely separated. A digitally enabled urgent care offering could treat many ailments very cheaply and still direct referral care to convenient landing places either within the system or elsewhere .

If telehealth does end up supplanting much of urgent care’s current scope of practice, it will be far easier for CityMD’s partners to replicate the digital model and reduce their fixed asset exposure than it will be for Northwell, tied up in a joint venture structure. Perhaps, one day, CityMD may regret the flexibility it allowed its partners.

Implications

- The urgent care industry is approaching the endgame with emerging national leaders driving consolidation

- Growing volumes at urgent care centers are enticing major delivery systems to reel these patents into their orbits. More markets may be reaching the point where urgent care has sufficiently ramped that picking sides will be an essential strategic choice. Evidently, Walgreen’s transitioning its convenience care sites to local providers is not the only strategic “destabilizer”

- As urgent care becomes more strategically threatening, expect late-to-the-game providers (therefore lacking attractive partners) to try to blunt that strategic impact (for example by telehealth end runs). By picking sides in delivery system market share wars, urgent care may be accelerating the pace of change which could hollow out its own economics

- The value of academic system branding in urgent care still seems to be an open question. Northwell – along with Banner and Ochsner – thinks yes, having a network of co-branded sites helps build ubiquity and brand equity while Mount Sinai and Montefiore are sticking with the opposite hypotheses (for now). This may also reflect a more tentative strategy pending how urgent care survives the looming threat from telehealth.