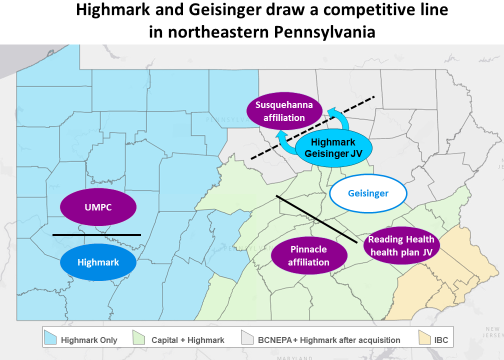

On May 10, Highmark and Geisinger announced plans for a clinical joint venture to create community-based care in four rural north-central Pennsylvania counties. The target counties are small (200K lives total), largely peripheral to Geisinger and Highmark core markets, and are already served by the Susquehanna Health system. Why all this complexity and investment to launch a battle for 1.5% of Pennsylvania’s population?

Look at the whole board

The move should be understood in the context of the widening struggle between Highmark and UPMC. Consent decrees have temporarily fixed some dimensions of competition in western Pennsylvania by requiring in-network access to UPMC for Highmark members under various conditions (e.g. when continuing treatment with a UPMC provider). With these decrees in place, UPMC needed to look for opportunity around Highmark’s flanks.

Moving west would be heading straight into the jaws of several high-performing, strongly-branded Ohio systems and Highmark’s publicly-held counterpart, Anthem.

East, on the other hand, would take UPMC into markets with dense populations (if you go far enough) and build out a state-wide delivery platform to advantage its health plan business. Further, the powerful Geisinger system in northeastern Pennsylvania had been expanding west (acquisitions of Lewiston Hospital and the Holy Spirit Health System in Harrisburg in 2013) and south (partnership with St. Luke’s in 2016). These moves may have persuaded independent delivery systems central Pennsylvania to consider affiliation talks. A collateral competitive benefit is that central and eastern Pennsylvania is also Highmark country.

Race to the Sea (…at least to New Jersey)

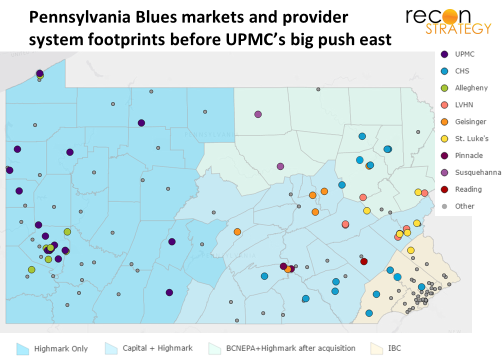

UPMC got started in 2016 in a quick series of alliance deals:

- May 2016: UPMC announces plan to acquire Susquehanna Health and invest $500M in enhanced emergency, cancer, cardiovascular, neurological and rehab services. Shortly after, UPMC Susquehanna announced a deal to buy nearby 118–bed Sunbury Community and 47-bed Lock Haven hospitals from Quorum.

- November 2016: UPMC Insurances Services and Reading Health agree to form a health plan joint venture starting with administration services for the Reading employees but eventually building out across lines of business. (Reading Health recently agreed to acquire five CHS hospitals on the outskirts of Philadelphia).

- March 2017: UPMC announces plans to acquire Pinnacle Health (six months after Pinnacle’s attempt to merge with the academic Penn State Hershey system was blocked due to anti-trust) while Pinnacle simultaneously acquires four hospitals from CHS to grow into a seven hospital, 905-bed system across four counties. The deal will be subject to anti-trust review.

These thrusts (assuming the Pinnacle deal goes through) have three major strategic implications:

- UPMC has acquired strong provider platforms in the central part of the state which threaten to replicate the powerful provider branding and health plan member “lock-in” formula which cost Highmark so dearly in Pittsburgh.

- The new provider platforms can serve as bases for further expansion east into New Jersey or southeast into Philadelphia.

- UPMC now stands at the gates of Geisinger, threating them from both the northwest (via Susquehanna), the southwest (via Pinnacle) and south (via Reading Health).

Response: Highmark partners with Geisinger in the north central frontier

Under the May deal, Highmark and Geisinger will build a new care model in four counties on Geisinger’s northwestern frontier where Susquehanna has strength. The model is to be centered on community-based sites and a new comprehensive campus in Montoursville (right in the backyard of UPMC Susquehanna Williamsport Hospital). Notably, Highmark and Geisinger described the collaboration as potentially the start of something bigger. Also, shortly after the deal was announced, Jersey Shore Hospital announced plans to integrate with Geisinger. Minimally, this collaboration should help preserve Geisinger’s competitive position vs. UPMC Susquehanna in the region. And in doing so, Highmark will help preserve some diversification of the provider base and avoid dependence on UPMC Susquehanna.

But why a joint venture? Couldn’t Highmark have just promised a long-term contract for the new infrastructure and simplified the governance? My guess is that threat to referral flows into the Danville hospital implied by UPMC’s upgrade plans was not great enough for Geisinger to counter-invest on its own. Capital is in short supply: Geisinger was given a negative outlook from Moody’s which might have also constrained its capital allocation to just the highest priority uses. Probably, the ROI calculations only worked for Geisinger if the capital costs were shared.

Highmark, too, must have bigger fish to fry than pouring capital into a small region of the state and executive time into a complicated governance. A community-based primary care infrastructure is hardly likely to make money (Geisinger will presumably reap most of the profit from the referrals). Putting competitive pressure on UPMC Susquehanna’s rates is valuable, but the impact will be also enjoyed by competing insurers.

In my view, Highmark is likely placing more emphasis on the potential for broader collaboration with Geisinger. Just as the UPMC affiliations with Susquehanna and Pinnacle systems look like platforms for competing with Geisinger, Geisinger can serve as a platform for counterthrusts westward- indirectly benefiting Highmark. Geisinger had recently focused its attention eastward in the New Jersey direction (demonstrated by its acquisition of New Jersey based Atlanticare in 2015 and the 2016 partnership deal with St. Luke’s, whose hospitals are concentrated to the east of Geisinger in Pennsylvania). The joint venture could be a test of whether Highmark can use capital to lure Geisinger’s attention back towards its western flank. How far could it go? UPMC clearly has ambitions set on the whole state. Geisinger might be considered outmatched vs. UPMC on its own, but once you add Highmark’s Allegheny Health system to the mix, the odds become more even. Perhaps – after having tried and failed with Cleveland Clinic and only gotten a cancer affiliation with Johns Hopkins — Highmark will find the affiliation partner for its Allegheny system with Geisinger.

Much to be decided in Pennsylvania over the next few years

The Pennsylvania market is at a very dynamic point. Beyond the issue of how the Highmark-Geisinger collaboration evolves and the FTC review of the UPMC-Pinnacle deal, the choices these new strategic constellations imply for the rest of the market are strategic:

- Capital Blue Cross in south central Pennsylvania has previously resisted a merger with Highmark and competes with it currently. Now that UPMC is landing in its market, bringing capital, brand, plan capabilities and a strong commitment to winning big. Will Capital Blue Cross reopen discussions with Highmark (and will Pennsylvania take the penultimate step to becoming a one-Blue Plan state)?

- The Penn State Hershey Health academic system which tried to merge with Geisinger back in 1997-1999 (which failed due to managerial and cultural issues) and most recently with Pinnacle Health (announced in June, 2015 but called off in October 2016, due to anti-trust considerations). The system will be effectively landlocked in Harrisburg if Pinnacle can complete its acquisition of CHS hospitals. Hershey’s own recent acquisitions (St. Joseph’s from CHS, and independent physician groups) are unlikely to be sufficient. Will it seek ways of working with UPMC which regulators can accept or reopen discussions with Geisinger?

- Lehigh Valley Health Network sitting between Geisinger and Reading Health has flirted with both UPMC and Highmark on network deals. Now it faces stiffer vertical competition with the Geisinger Health Plan-St. Luke’s deal in its home turf and the Reading Health-UPMC Health Plan joint venture to its south. Will it continue to try working with both the UPMC and Highmark sides as a provider, pick one, or seek its own insurance partner?

- CHS plans to sell hospitals to Pinnacle and Reading Health. Assuming this goes through, CHS will continue to have 6 hospitals and over 1,000 beds in northeastern Pennsylvania. Will CHS look to sell more Pennsylvania hospitals as part of its restructuring, potentially further destabilizing the competitive dynamics?

- Philadelphia healthcare has long been able to stay agnostic to what goes on in the rest of the state. But as the surrounding players start to consolidate, the attraction of partnerships to secure referrals and scale will become hard to resist. Which Philadelphia provider will be the first to make an alliance with a state-wide partner — and which will be the last, perhaps finding itself with no partners left to cut a deal with?

Depending on which way these choices are made over the next couple of years, we will know if UPMC’s push east in 2016/17 was a bold stroke that locked in an unassailable state-wide leadership position – or if these moves just expanded the competitive battlefield and stimulated the formation of a worthy state-wide, vertically integrated competitor.