UPMC’s recent spectacular deal-making careen through central Pennsylvania (picking up the big Susquehanna and Pinnacle systems as affiliates and Tower as a joint venture partner all in under a year) contrasts oddly with its tentativeness at home: in mid-September, UPMC unexpectedly scuttled plans to build a 90-bed, $211M hospital in the South Fayette suburb of Pittsburgh just a week after signing a deal with a developer which would have launched construction. Spokespeople said UPMC is “pursuing other, more significant strategic options” (per Pittsburgh TribLive).

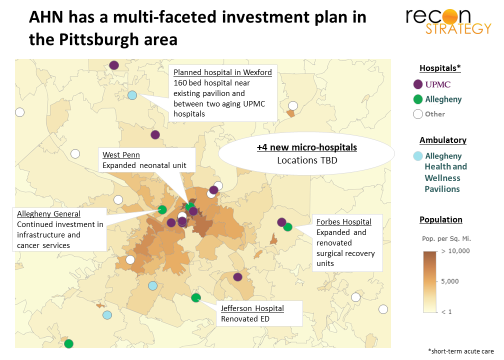

Perhaps UPMC caught early wind of the latest contrivance of its local rival – Allegheny Health Network (AHN): on October 18, AHN announced plans for $700M investment including refurbishing existing hospitals and constructing five new ones. The largest new hospital will be in Wexford, a well-off suburb about 15 miles north of Pittsburgh where AHN already has substantial ambulatory capability (a newly built 174K sq. ft. so called “Health and Wellness Pavilion” sandwiched between UPMC’s two aging Passavant hospital campuses).

Most innovative from a strategy point of view, AHN is introducing the micro-hospital model in Pennsylvania. The four other new hospitals will be of this type. They are being built through a joint venture with Emerus, the private-equity backed leader in the micro-hospital niche with active partnerships in Texas, Colorado, New Mexico, and Nevada.

Micro-hospital economics

The typical micro-hospital has 30-60K sq. ft., housing a 7-9 bay 24/7 emergency department, 7-9 inpatient (I/P) beds along with labs, x-ray, ultrasound and CT. Medical offices and ancillary services (physical therapy, ambulatory surgery centers, etc) can be co-located, attached or set up on the second floor.

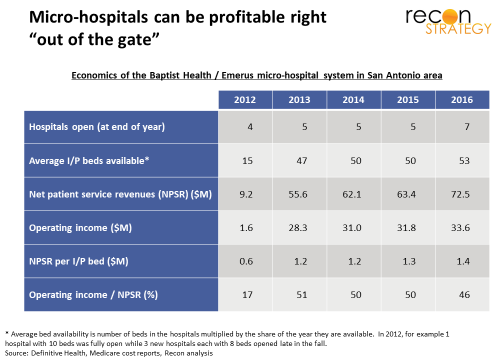

And these hospitals make money straight out of the gate! Take a look at the aggregate economics of Baptist Health’s joint venture with Emerus (which is one of the longest standing in the Emerus portfolio: the first micro-hospital opened in December 2011 and six more were added since so the economics reported below include ramp-up time). Also, keep in mind this is the facilities view and does not include professional charges or costs and is also based on Medicare cost reporting.

How do they do it? Here’s my take of how the economics work:

- Bite-size capital investment. Micro-hospitals are relatively inexpensive ($15-25M in capital expenditure) and quick to build (12-14 month build times). This overstates the investment required, because Emerus and partners sometimes use real estate investment trusts (REIT) to defray the CapEx (for example, the 4 facilities of SCL Health’s micro-hospital network were bought by Healthcare Trust of America REIT for $135M and then leased back). These construction parameters allow for a “swarm” approach: standing up multiple facilities in parallel and over a short time to achieve strategic surprise and block competitive response.

- “Inpatient-optional” operations. As some might guess: at their core, micro-hospitals are emergency departments: I/P bed occupancy rates are low-teens at best and I/P care makes up 4-5% of gross charges. A geographically focused network allows a centralized staffing pool to shift as needed to support any admits, lowering the break-even volume for each site. (At the same time, by the way, an I/P operation – even if more theoretical than real — should preserve facilities rates on technical services from the site-of-service adjustments which threaten off-campus sites.)

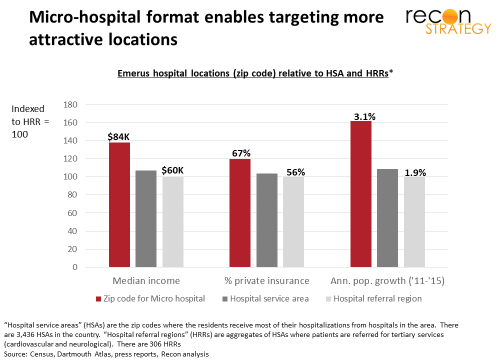

- Excellent payer mix and growing populations. Surgical siting allows operators to place micro-hospitals near patients with attractive reimbursement. Emerus micro-hospitals are in zip codes with materially higher median incomes, higher rates of commercial coverage, and are rapidly growing relative to their local markets.

No surprise that, while Medicare and Medicaid make up 27% of net patient service revenue of the overall Baptist system, these government payers together are just 9% of the net revenues of the Baptist/Emerus micro-hospital network. And, once these commercially insured patients enter the system via the micro-hospital ED “front door,” it is far easier to keep any referred care within the system.

No surprise that, while Medicare and Medicaid make up 27% of net patient service revenue of the overall Baptist system, these government payers together are just 9% of the net revenues of the Baptist/Emerus micro-hospital network. And, once these commercially insured patients enter the system via the micro-hospital ED “front door,” it is far easier to keep any referred care within the system.

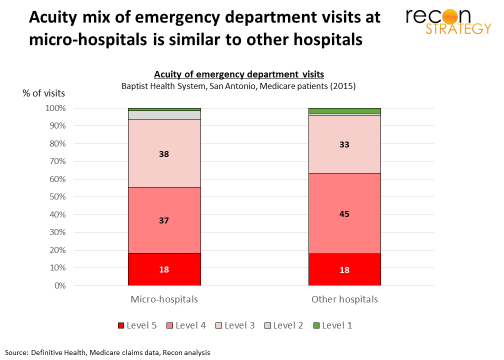

- Robust acuity of care. There is some debate about the acuity of cases attracted to free-standing and off-campus emergency departments (in its June 2017 report, MedPAC suggested CMS consider changing payments to free standing and off-campus emergency departments to reflect lower acuity of patients). Micro-hospitals do not appear to have that issue – the acuity of their ED visits is, on average, about the same as those of other hospitals (this is not true of their I/P case mix which averages 0.85 for the micro-hospitals s. 1.70 for the flagship Baptist Medical Center; however, given the very small share I/P care appears to play in micro-hospital economics, this may be a minor issue). Perhaps having I/P care capability directly attached to the ED (even if it lacks patients) adds a level of credibility for patients or may avoid the kind of patient confusion about appropriate acuity levels that free-standing EDs experience.

- Consumer friendly model in a destination package. Big hospital systems may have locally recognized brands, but with their large, often bureaucratic workforces, broad spectrum clinical capabilities and aging, “physician-centric” infrastructures, they are often ill-equipped to deliver a great consumer experience. By operating in a joint venture, however, micro-hospitals couple that brand with a good patient experience delivered by Emerus running the nursing, administrative staff and day-to-day operations in a brand new building. ( Emerus boasts 4 consecutive years of winning Press Ganey Guardian of Excellence in various individual hospitals). Further, by having a mix of services (emergency plus medical offices and diagnostics) located in the neighborhood, consumers will have multiple opportunities to get to know the site and quickly fit it into their mental inventory of preferred clinical resources.

Obviously a lot has to go right in the placement, roll-out and operations of the micro-hospital network to capture all of these advantages. What is intriguing is that they are small enough to enable targeting to the precise conditions where they can thrive.

Shifting provider competition to a battle for zip codes

In delivery system competition, hospitals have been a key way to “seize and hold” ground. By acquiring hospitals, affiliating with them, renovating them or just building them, a delivery system can (usually) secure the means to (in effect) set terms to local providers and shape the price of entry for integrated competitors. For that reason, it takes only 5,500 or so hospitals to define the 3,500 geographically distinct hospital service districts into which the analysts at Dartmouth have carved the US.

Historically, hospital power was a function of scope and scale. But innovation in technology and clinical practice has hacked away at the scope of hospital care by shifting more to ambulatory. Micro-hospitals can help shift the unit of scale from hospital to network, while shifting the geographic lens from service area to zip code. With the Emerus joint venture, AHN can test whether a value proposition of excellent consumer experience coupled with “just around the corner” convenience delivered in small packages can win vs. one of the nation’s most powerful academic brands.

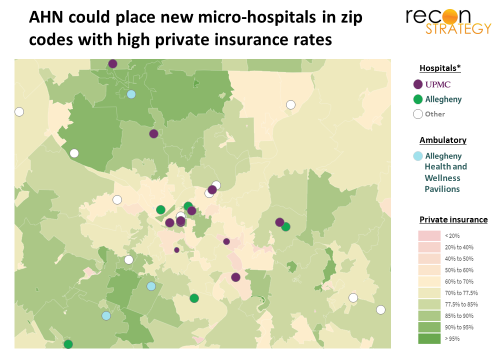

There is good reason to bet on this asymmetric competitive approach: take a look at the map of Pittsburgh in terms of share of commercial coverage. Not surprisingly, the big academic and community hospitals of UPMC located in more urban areas as is traditional – tend to site where the share of commercial coverage is low:

It is easy to see the zip codes where micro-hospitals could bleed off (as it were) commercially covered patients and feed them into AHN. Keep in mind, even if Highmark and UPMC health plans are pushing narrow networks, the big national plans have both AHN and UPMC in their networks so there is opportunity to shift share within existing plan products. AHN micro-hospitals may not only contribute a lot of profit; they may help disproportionately grow AHN’s share of commercial business, and burden UPMC economics with a growing share of government-funded business. (Worth noting: Pittsburgh neighborhoods lack the demographic dynamism of the ones Emerus typically targets, so it will be interesting to see if that difference hampers their success).

Highmark’s health plan business can benefit too. Having an array of newly built, consumer friendly healthcare destination sites within the neighborhood can go a long way toward reassuring employees facing a choice among narrow network plans that the Highmark product focused on the AHN network can be right for them.

No wonder UPMC needs to rethink its Pittsburgh strategy.