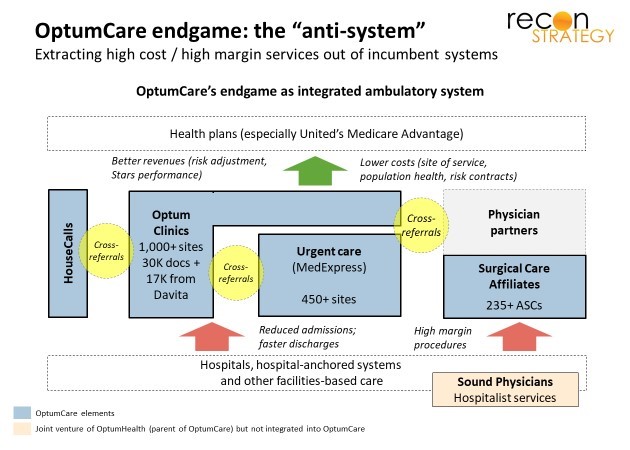

By bringing together accountable-minded physicians, urgent care and ambulatory surgery centers (ASCs) on a national scale, OptumCare could prevent a lot of avoidable hospital care and move much of what remains to lower cost sites of service. Wrap a capitation business model around it and you have a powerful “anti-system” – profitable for itself and toxic to hospital margins.

OptumCare has a long way to go to put this theory into practice. It is still in only ~35 of its target 75 markets. And, within many of those 35 markets, OptumCare has a major remodeling job: it lacks critical mass; has some practice groups that still operate with an “old school” FFS/RVU mindset; and lacks tools to effect quick transformation (because OptumCare’s relationship with physicians is through an IPA rather than employment).

In some markets, OptumCare also has incentive misalignments

Like many hospital systems, OptumCare has, in some places, “one foot on the dock and one foot in the canoe.” OptumCare was largely assembled through a series of acquisitions. Legacy business relationships in individual markets contributed to the valuation of the targets and continue to help managers in these businesses meet “UNH-grade” operating targets. And some of this legacy business is bound up in lucrative hospital partnerships which create conflicts with the “anti-system” philosophy.

Let’s look at a specific example. Indiana is, in many ways, an ideal market for “anti-system” disruption. First, it is very expensive. Commercial rates on hospital-based care run 180-200% of inpatient Medicare (per CBO[1]) nationally; in Indiana, however, commercial rates for hospital inpatient run 215-220% of Medicare and hospital outpatient department care (HOPDs) runs at 328% of Medicare (per Rand[2]). Second, Indiana Medicare Advantage is growing fast and concentrated[3] so a few capitation deals could cover a sizeable part of the market. Finally, OptumCare has the makings of an “anti-system” platform: 200 physicians spread across Indiana and Ohio from OptumCare’s American Health Network acquisition; multiple urgent care sites under the MedExpress brand; and twelve ASCs[4] with 38 operating rooms and 16 procedure rooms through its SCA subsidiary.

These ASCs are operated in joint venture with IUHealth with Optum ultimately owning ~25% share. Combining with IUHealth must be economically attractive: IUHealth’s rates on HOPD care average 382% of Medicare and one can suppose, as majority-owned sites, comparable mark-ups apply to the joint ventured ASCs. A minority share also likely means IU Health decides how much effort to put into shifting the clinical habits of surgeons on HOPD vs ASC site-of-service.

Indiana penetration of ASC site-of-service far from best-in-class

Current penetration of ASC site-of-service in Indiana and at IUHealth appear to be well below best-in-class. Medicare makes up 30%+ of ASC cases today (per VMG[5]), large enough to provide an indication of underlying patterns of care. We evaluated the share of CPT codes which Medicare reimburses at ASCs and HOPDs. We compared this share in Indiana and IUHealth vs. averages for 6 major MSAs in Florida, Nevada and Texas with high penetration of ASCs. By using benchmarks for MSAs rather than institutions, we are using actual practice as a benchmark, avoiding selection bias in patient risk and, therefore, mostly measuring differences in clinical and business practice.

In Indiana Medicare FFS, about 33% of CPT procedures which Medicare pays for at both ASC and HOPD (weighted by claims value) are done at ASCs. Composite best-in-class share across these procedures would be 77%, implying the potential to more than double the volume of ASC activity[6]. For OptumCare/IUHealth, the realized share is somewhat higher (38%) but so is the best-in-class target (78%) given IU Health’s mix of procedures.

Capacity is not the issue. Based on state utilization data (which covers all payers, not just Medicare), the OptumCare/IU Health ASCs perform an aggregate of 74K surgeries/procedures or about 3.9 surgeries/procedures per day across a mix of operating and procedure rooms. Nationally, top ASCs can perform 8.1 surgeries per day in each operating room and 12.2 procedures per day in each procedure room (VMG data for 2016). The issue then must be clinical habits and the limited incentive to adjust those clinical habits to lower cost site-of-service if your parent also has a lot of HOPD operating rooms to fill (and can generally do so at fantastic rates).

Taming the disruptor with a fat margin annuity: a back-of-the-envelope calculation

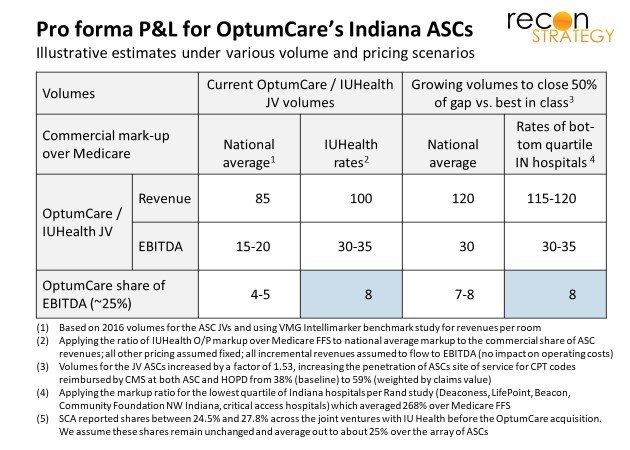

If the OptumCare/IUHealth JV is structured traditionally, OptumCare only shares in the ASC margin and should have every incentive to expand utilization. Let’s run a few back-of-the-envelope guesses using national data and see what the alternatives look like.

At 74K surgeries/procedures across 75 rooms, OptumCare’s ASCs in Indiana operate at somewhat below the median volume for ASCs across the country (per VMG’s benchmarking study). We can use VMG data to estimate the joint venture P&L in three steps: first, convert the average volume per room into revenues and EBITDA by matching the volumes to P&Ls across quartiles reported for the VMG sample; second, adjust the revenues to reflect the higher mark-up over Medicare the commercial share of revenues likely enjoyed vs. national ASC participants in the VMG study[7]. Given that Indiana’s operating costs for providers are unlikely to be very different than the national average, we assume that all the incremental revenue from exploiting IUHealth’s high commercial rates fall to the EBITDA bottom line of the ASCs. The results suggest that OptumCare’s Indiana ASCs make earn $100M in revenues and $30-$35M in EBITDA of which OptumCare (at 25%) would take home around $8M. Not bad.

Now suppose OptumCare swapped in another partner much more pliable in terms of directing surgeries to ASCs. If OptumCare could increase ASC penetration from 38% to 58% of applicable procedures (closing 50% of the gap vs. best-in-class), it would raise room utilization closer to the 75% percentile and improve operating margin. More pliable hospital partners, however, would likely have lower commercial markups over Medicare. If we use the average mark-up of the lowest quartile of hospitals in Indiana per Rand, we would still have a mark-up at 268% of Medicare (vs. 189% for the nation).

Under this scenario, OptumCare would be no better off than it is now, still earning about $8M in EBITDA. OptumCare would need to effect a massive change in expectations among referring doctors and clinical habits across many surgeons – no easy feat – just to get to where they are now. See exhibit below:

If these back-of-the-envelope calculations are right and could be adjusted for the implementation risk (and the incremental investments required to change physician practice), OptumCare would be far better off capturing the annuity on the current volume at its ASCs while enjoying IUHealth rates vs. trying to disrupt its partner and the market by pushing growing the ASC volume towards best-in-class.

In these kinds of situations, OptumCare may be ready to benefit when partners like IUHealth start facing irresistible pressures to radically change site-of-service (e.g. from payers, benefit designs, consumers). But they are unlikely to be the ones pushing for radical change beyond what they can influence within their health plan membership.

Implications

- There are vast differences in ASC penetration rates across the country in Medicare. There are no obvious clinical reasons for this variation. If the gap in Medicare is replicated across other lines of business, their closure vs. demonstrated best-in-class is a major opportunity. However, the differences are likely bound up in clinical culture and surgeon habit – not easy to shift!

- If OptumCare integrates clinics with urgent care and ASCs, it could be very disruptive of high-cost hospital systems. However, legacy incentives for component businesses in local markets will affect OptumCare’s strategy. Payers should expect variation on a market-by-market basis and may find that OptumCare is not the partner in driving lower costs they might expect.

- Disrupters going after site-of-service arbitrage should not assume OptumCare will have the “disruption opportunity” sewn up in all markets where they are present. There will be plenty of opportunity – including, maybe, a chance opportunity to disrupt Optum-owned assets slowed down by big local partners – in multiple markets.

Tess Niewood, Consultant

Tory Wolff, Managing Partner

[1] CBO, “An Analysis of Hospital Prices for Commercial and Medicare Advantage Plans” presented at 2017 Annual Research Meeting of Academy Health, June 26, 2017. Data is from 2013

[2] Rand, “Hospital Prices in Indiana – Findings from an Employer-led Transparency Initiative”, 2017

[3] United’s share has ~27%, HUM has ~30%, Anthem about 15%.

[4] The ASC varies by source as some ASCs have multiple locations but are considered one ASC (e.g., Beltway). We use Indiana state reporting as basis for the ASC, O/R and procedure room calculations.

[5] We use the VMG Intellimarker Multi-Specialty ASC Benchmarking study for 2017 which provides 2015/16 data for a large sample of ASCs as the basis for several calculations in this section.

[6] This is close to the national average. We estimate about 30% of the applicable CPT codes are done at ASC settings, although, interestingly, given the mix of CPT codes done at either ASC or HOPD nationally, the best-in-class target is lower (only ~65% of procedures weighted by charges) could be done at an ASC vs. the 77% for Indiana.

[7] The CBO data on commercial to Medicare mark-up was for inpatient only; we developed an estimate for outpatient markup using the difference between inpatient and outpatient markups in the Rand study.