Last month, Warburg Pincus closed on previously announced plans to acquire a major multi-specialty practice in northern New Jersey (Summit) and combine it with an urgent care network centered in the New York metro area (CityMD). The deal reflects private equity’s recognition that, as the stand-alone urgent care business model is increasingly vulnerable, the valuations in accountable care are increasingly compelling.

Urgent care’s evolution

Early on, urgent care entrepreneurs focused on filling the gap between overscheduled primary care and expensive ERs. Ramp the visits per day high enough and the profits on URIs and simple fractures could be enormous. Over time, delivery systems recognized urgent care’s potential for growing market share. The lifetime value of a patient to a system far exceeds the margins on their minor acute care alone. So, urgent care has become increasingly tied to systems, either through greenfield growth, acquisition, or staffing take-overs. The door for urgent care exits to strategic acquirers opened wide.

CityMD did not walk through that door. Instead, they tried a delicate dance, slicing up the metro NY market by borough and forming strategic alliances with the local leader in each. That was the strategy when Warburg acquired a majority position in 2017. But there were three issues: first, as CityMD’s system partners push into each other’s boroughs, they would expect CityMD to choose sides, creating conflicts among its partners. Second, fragmented alliances meant no clear buyer to fund Warburg’s exit. Third, telemedicine was making deeper inroads and eating into urgent care stand-alone economics. Where is Warburg’s path out?

In parallel, evidence was accumulating – from players such as ChenMed in Florida, DuPage in Chicago, portions of OptumCare such as WellMed in Texas and Florida – that stand-alone physician practices can turn accountability into profits. The formula:

- shift panels to capitation (especially Medicare Advantage)

- document and manage the patient risks meticulously

- reengineer operating models to drive big reductions in hospital care (and pull the associated hospital margins into the practice’s P&L).

Summit Medical Group is an ambitious member of this emerging cohort of “anti-systems” (executive interviews at the end of last year described 65% of their patient panels being in “full risk” arrangements and nationally scaled ambitions) and well regarded by its health plan partners. Warburg’s plan appears to be to dramatically grow Summit and remake CityMD into a metro New York anti-system powerhouse.

Racking and stacking the components

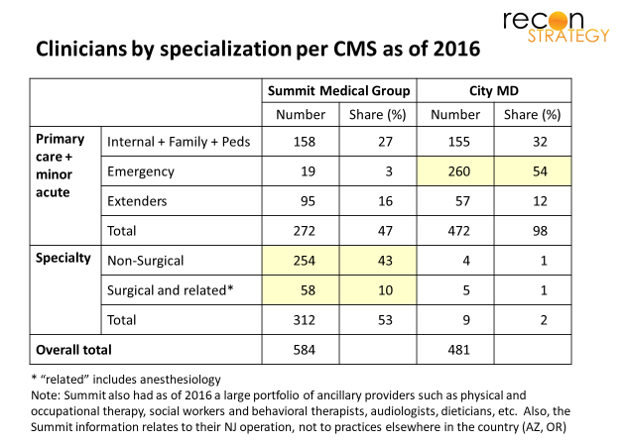

CityMD and Summit seem highly complementary. First, look at their clinicians[1]. CityMD’s focus on minor acute (with emergency medicine 54% of the total) contrasts sharply with Summit’s specialty-rich staffing (53% of total)[2].

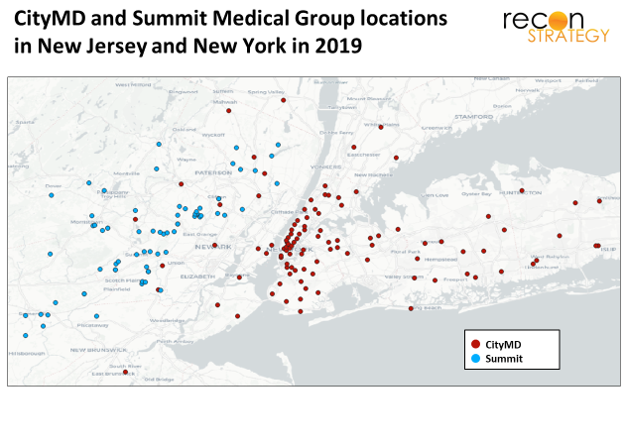

Second, look at their respective geographic footprints (including clinics, urgent care and other specialty care delivery points). Summit’s northern NJ position and CityMD’s NYC and Long Island position are two halves of a very big apple (as it were).

CityMD as Summit’s beachhead across the Hudson

What could be the plan? Start simple: most of Summit’s patient base are wealthy suburbanites, many of whom likely commute into NY for work. Save them taking a half day off by addressing minor acute issues or getting ancillary services such as labs or basic imaging during lunch hour at CityMD. And, for CityMD patients who live in northern NJ but lack a preferred provider, integrated scheduling will allow these patients to get more complex care needs met at Summit.

Over time, additional clinical services can be provided on the CityMD network such as:

- On-demand virtual specialty consults for patients whose condition falls outside of CityMD’s minor acute scope, and

- Build-up of primary care and specialty serving that portion of CityMD’s New York patients who are seeking a new primary care relationship.

This won’t come cheaply: capacity will need to lead demand a bit until panels fill out, adding operating cost. CityMD sites will need upgrades to accommodate both virtual and traditional appointments side by side with walk-in flows. Also, Summit will eventually run out of docs that are licensed in both NJ and NY and are willing to split practices. They will need to either recruit or support dual licensing for others.

But the scale-up costs and implementation risks are far less together. Summit should allow CityMD to build up these capabilities without incurring a strategic dependence on a local partner and allow it to do so taking advantage of Summit’s scale (e.g., having appropriately licensed physicians come into town for 1 or 2 days a week at selected sites as the panels are built). And CityMD can provide Summit with many convenient access points and a flow of patients lacking a strong care relationship in New York.

In the out-years, Summit/CityMD will have a powerful offering to take to the market: an integrated ambulatory group with specialty depth across metro NY and northern NJ, the convenience of ubiquitous urgent care access and an operating culture well versed in delivering an experience that affluent commercial patients expect.

By integrating Summit’s risk management capabilities, the new organization can strike capitation deals with the top Medicare Advantage plans in metro NY. If Summit/CityMD can get enough capitated patients into its panels and manage them effectively, the company could see several hundred thousand $ per primary care doc in incremental margin (we’ve done the math: they only need achieve a portion of ChenMed’s documented reductions in hospital-based care and earn a reasonable lift from more complete documentation of the risk of their patients).

Challenges

Of course, the strategy will face execution issues:

Tricky integration: Summit operates on Athena while CityMD operates on eClinicalWorks[3]; some integration solution will be needed. More important, the clinical and operating cultures of “risk-taking multi-specialty” practices and “convenience and efficiency-oriented” urgent care won’t be easily consolidated. Strong physician leadership on both sides will be important.

System partners become competitors: While CityMD’s partnerships with local systems appear relatively dormant[4], there will likely be some reaction to the deal. As Summit’s clinical capabilities are stood up east of the Hudson, referrals to CityMD’s partner systems will decline. These partners may invest more in their own urgent care networks or (given the relatively saturated NY market) drive harder down telehealth alternatives. Either way, CityMD can expect more of a fight for its urgent care bread-and-butter. The plan may suffer a setback if Summit/ CityMD mistime their roll-out and system partners drain away CityMD’s urgent care traffic before CityMD can convert them to Summit patients.

Exit path

While the implementation path seems feasible, it may take more time to complete than Warburg wants to wait before exiting. Fortunately, at least one logical strategic acquirer – United’s OptumCare — will likely be impatient to bring in Summit/CityMD. In fact, OptumCare might want to tweak the integration strategy to suit its own ends.

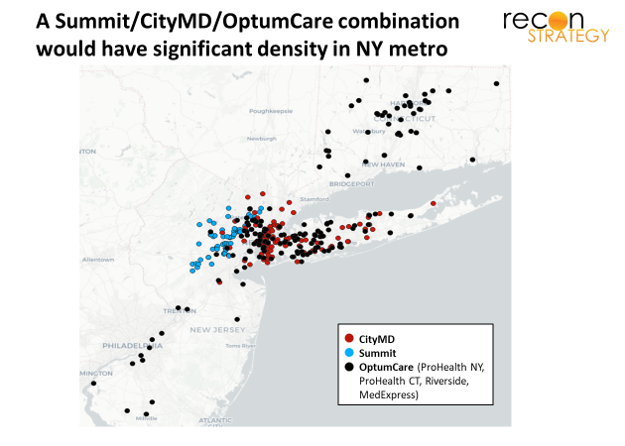

While OptumCare is already a presence in the greater New York area, a Summit/CityMD acquisition would create substantial value for at least three reasons:

Northern New Jersey. OptumCare’s presence is thick on Long Island and somewhat thinner in western Connecticut and southern New Jersey. There are two major gaps: northern New Jersey and Westchester. Acquiring a Summit/CityMD combination would fill one of those gaps (see map below).

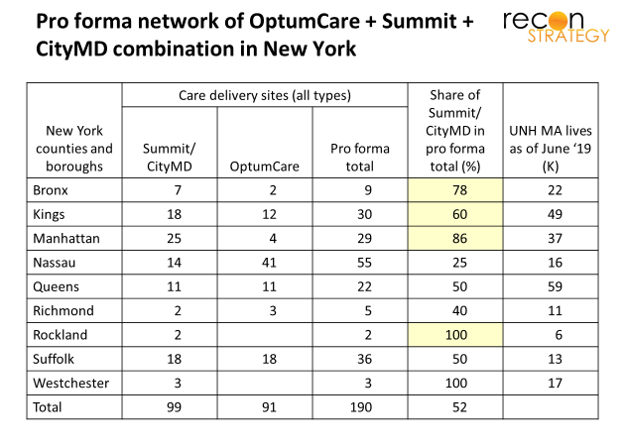

Tuck-in in the boroughs. Optum’s ProHealth practices in New York have depth in some counties (especially Nassau), gaps in others. The current CityMD network – especially if these sites were upgraded to provide a broader range of specialty and primary care coverage – would make a nice complement by adding access points in the Bronx, Kings, and Manhattan (see chart below). More access points allow for a greater overlap between United’s Medicare Advantage lives and OptumCare clinical care delivery. Further, more physicians will add to OptumCare’s leverage over referral partners to ensure alignment on clinical strategy and – as a result – better performance on capitated agreements

Platform to expand United’ Medicare Advantage position and drive transformation of OptumCare’s New York tri-state clinical culture. United is the largest MA plan in the New York metro area but, today, only a portion of their lives have access to the OptumCare delivery system. Further, OptumCare’s acquisition-based growth and nationally scaled ambitions has forced compromises; they have had to buy the practices that were available, not always the most risk-ready. From what we hear anecdotally (so take this with a few grains of salt), OptumCare’s ProHealth practices in NY and CT still have a long way to get to an operating model ready to take full risk. It is hard to drive that kind of change from a distance. However, Summit could serve as a central anchor and a demonstration platform to support transformation out along the Long Island and Fairfield County axes.

Given these potential synergies, Optum would be wise to take Summit/CityMD off Warburg’s hand well before Warburg completes the hypothesized strategy.

Implications

- Urgent care as a stand-alone business is approaching the end of its run. Investors should exit soon or find ways to significantly modify the business model to try to catch the next valuation wave

- Anti-system models (full risk ambulatory care) is attracting significant attention but the formula for scaling the operating model and building the clinical culture is not well understood. Doctors are a challenge to manage! If we are correct in our assessment of Warburg’s strategy, the Summit/CityMD integration will provide a great test case of a new approach (adjacent operations, expanding on an urgent care platform)

- New York systems can anticipate a significant heating up of the “anti-system” dynamic in their market over the next 3 to 5 years as Summit/CityMD and OptumCare mature.

[1]Based on 2016 data – the latest readily available from CMS Provider Utilization and Payment data for public use which we access through Definitive Healthcare.

[2]Summit’s depth in surgery is interesting. 27 of the 50 surgeons at Summit in 2016 were specialized in orthopedics. The opportunity to provide the facilities-based care for all those knee and hip replacements which can’t be done at an ASC must provide Summit with a lot of leverage over its hospital partners.

[3] Ironically, Warburg has stakes in and is bringing together two EHR companies specialized for the urgent care business – DocuTap and Practice Velocity.

[4] There’s been little publicity about them since the alliances were struck in 2016.