Here’s what we surmised in the original post on this topic:

“That leaves United. A leadership position in C-SNPs would fit well with United’s leading position in Medicare Advantage overall, #1 position in D-SNPs and #2 position in I-SNPs. The capabilities would also seem to be readily applicable to the broader Medicare population (given, for example, the potential transfers back and forth across between C-SNP and regular Medicare Advantage). The curious thing is that United dramatically reduced its C-SNP business last year (went from about 35K lives to 5K lives this year). It would be, well, interesting to see them spend billion+ to get back in.”

And here’s the full original post:

Summary

- XL Health, the leading chronic special needs Medicare Advantage plan, is up for acquisition with three suitors identified: United, Aetna and Wellpoint.

- XL’s incremental market share would probably strengthen Aetna’s negotiating clout the most (though not to a point of advantage).

- The leading capabilities in managing chronically ill seniors most logically fit with United’s overall leadership in Medicare Advantage….but they would be paying a big price tag to get back into a niche they retreated from just last year.

- Wellpoint would appear to derive the least benefit: Wellpoint lacks a Blue license in many of XL’s service areas and XL’s care management approach to chronic special needs plans is quite different than the one Wellpoint got with Caremore.

- It is curious that Humana has not been identified as being interested. The market share and capability synergies seem to be quite attractive at first blush and, perhaps, stronger than for any of the three identified suitors.

Public reports suggest XL Health is in play for $1.5 to $2 billion with three potential acquirers named: United, Aetna and Wellpoint. The synergy logic for each is different, probably most compelling for Aetna, least compelling for Wellpoint, and most mysterious for United (given that they pulled back from the same Medicare Advantage niche that XL operates in just last year). Let’s take a closer look:

XL Health is a Medicare Advantage Special Needs Plan (SNP) with about 110K Medicare Advantage lives total (98K are in SNPs) in Texas, Georgia, South Carolina, Arkansas and Missouri. (SNPs are a category of Medicare Advantage focused on eligibles with unique support and care coordination needs and falling into one of three categories: (1) low incomes and dual-eligible for Medicaid and Medicare (D-SNPs), (2) living in nursing homes and similar institutions (I-SNPs) and (3) with severe chronic conditions (C-SNPs). SNP members are generally heavy utilizers with average risk scores about 20% higher than average FFS Medicare. 80+% of total SNP lives are in D-SNPs. Also, the number of lives in chronic SNPs has declined over the past few years as Medicare tightened the rules on member eligibility and players such as United pulled back).

XL is the #3 player among SNPs with about 7% of the national market (behind United and Aveta); importantly, almost 90% of their SNP lives are in chronic conditions (not surprising given their origins as a disease management company), making them far and away the largest player in this sub-category (with 45% of the national market). See the very useful overview on SNPs and market shares from Kaiser here.

Three major sources of value for an acquirer:

(1) The existing economics and growth trajectory. Not a lot of transparency on profitability, but XL Health did grow lives about 27% between October 2010/2011 in a shrinking C-SNP market. Also that growth was pretty evenly distributed across markets which suggests an operating model with legs (can be successfully deployable in a variety of state contexts). Not bad and likely equally valuable to all three players.

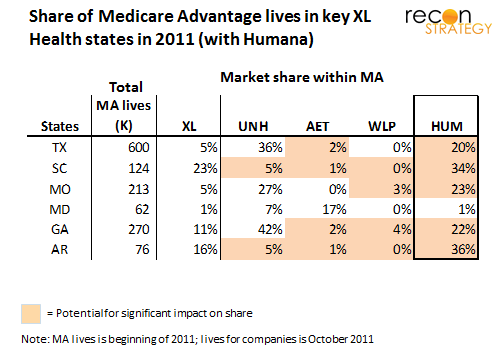

(2) Enhanced local market share to improve contracting leverage in Medicare Advantage and possibly for the broader commercial business. Compared with D-SNPs (which typically share provider networks with Medicaid) or I-SNPs (which have their own unique networks), the providers treating C-SNP members are likely to have the greatest overlap with traditional Medicare and even commercial networks. The potential market share synergies here appear to favor Aetna. (Note: in chart below, add XL market share to any of the others for an estimate of pro forma combined share; the estimates are conservative given the higher average utilization of C-SNP members).

United

United has a strong Medicare Advantage position in two of XL Health’s largest markets already (Texas and Georgia), The two states where XL Health would have the biggest incremental impact on United’s share are the smallest markets over all (South Carolina and Arkansas). One point in United’s favor is the looming prospect of SNPs having to disenroll members who no longer fit the eligibility criteria by 2013: a larger incumbent will likely be able to pick up more of these members (though it is unclear how many XL Health may have in its book). In addition, there might be more local operating cost synergies with United. But given the unique needs of the C-SNP population (and United’s apparent lack of skill with these patients), these are probably going to be relatively small.

Aetna

For Aetna, XL’s incremental market share is unlikely to create a structural advantage. However, it would make the playing field a bit more level (e.g. taking Aetna share in Texas from 2% to 7% and in Georgia from 2 to 13% — enough to get on providers’ radar screen). In TX and GA, Aetna and United have roughly comparable shares in the overall market (both have shares in the high teens in Texas and low teens in Georgia), so getting better balance within the Medicare market would be particularly valuable for Aetna to enhance parity among high utilizing lives.

Wellpoint

For Wellpoint, the picture is less clear. Wellpoint does not hold the Blues license in Texas, Arkansas and South Carolina, so would be competing with the local non-profit cousins and without the benefit of the Blue branding. The most interesting upside may be in Georgia but it appears that even post acquisition, Wellpoint would be well behind United within the Medicare Advantage market.

(3) Leading C-SNP capabilities. XL’s leadership position among C-SNPs would bring its future owner just about half the lives being managed under this model across the country. Presumably, XL Health’s relative position will only grow stronger with the tightening standards for C-SNPs (e.g., CMS is looking to review SNP care models). Which player would most value being “King of the C-SNPs”?

Wellpoint

Wellpoint has acquired a decent position in C-SNPs via its Caremore acquisition (about 20K lives). However, I suspect the model for managing the members is very different and hard to reconcile: Caremore has a primary care-led model focused on a narrow network of care centers while XL Health (hypothesizing) takes a more standard managed care route through direct plan-to-member interactions and orchestrated non-PCP support (e.g. pharmacist counseling, home visits and social services). In some sense, the XL model might be more scalable to other states (i.e. not require the construction of the full Caremore infrastructure) But, given that XL’s service area is focused on non-Wellpoint states, Wellpoint would need to create a kind of Blue utility model for C-SNP services to avoid aggravated the non-profit Blues. It is possible (after all, they jointly acquired Bloom with HCSC which controls Texas) but tricky.

Aetna

Aetna has been positioning itself as deeply capable in care coordination and management which fits well with XL’s model. However, the value of C-SNP capabilities if you don’t have a lot of lives in broader Medicare Advantage isn’t obvious. There may be some opportunity to deploy XL capabilities to complement ACO providers but it seems like a big price tag (paying for all those Medicare Advantage premiums) for what remains a fairly uncertain market. The payoff for XL would appear to be linked with aggressively growing its broader Medicare Advantage position.

United

That leaves United. A leadership position in C-SNPs would fit well with United’s leading position in Medicare Advantage overall, #1 position in D-SNPs and #2 position in I-SNPs. The capabilities would also seem to be readily applicable to the broader Medicare population (given, for example, the potential transfers back and forth across between C-SNP and regular Medicare Advantage). The curious thing is that United dramatically reduced its C-SNP business last year (went from about 35K lives to 5K lives this year). It would be, well, interesting to see them spend billion+ to get back in.

One last note:

It is curious that Humana has not been named as an interested player. The incremental impact an XL acquisition could have on Humana’s share in each of these markets is attractive (perhaps more so than for Aetna, given that Humana has much fewer commercial lives to bolster its negotiating leverage in these markets).

Further, XL’s care management capabilities would likely fit nicely into Humana’s “15 Percent Solution” for reducing costs and making Medicare economics work (of which 1-2% cost reduction comes from early identification, 3-4% from clinical integration and guidance — both presumably central to what XL Health does — and 1-2% come from claims cost management and effective coding – important for getting fully reimbursed for chronically ill patients). The only draw-back I can see is that C-SNPs do have some overlaps with dual eligibles and Humana has historically not been interested in Medicaid. But – per the latest earnings call (see Mike McCallister’s answer to Charles Boorady’s question on duals), they are “looking at duals really, really carefully.” Seems to me Humana should be looking at XL.

Further, XL’s care management capabilities would likely fit nicely into Humana’s “15 Percent Solution” for reducing costs and making Medicare economics work (of which 1-2% cost reduction comes from early identification, 3-4% from clinical integration and guidance — both presumably central to what XL Health does — and 1-2% come from claims cost management and effective coding – important for getting fully reimbursed for chronically ill patients). The only draw-back I can see is that C-SNPs do have some overlaps with dual eligibles and Humana has historically not been interested in Medicaid. But – per the latest earnings call (see Mike McCallister’s answer to Charles Boorady’s question on duals), they are “looking at duals really, really carefully.” Seems to me Humana should be looking at XL.