The PE firm TPG is reportedly considering investing in LHC, a publicly-held home health agency (LHC announced earlier this year they were exploring strategic options). PE funding could allow LHC to pursue a much bolder strategy in the wide-open post-acute care market.

Home health

With home health revenues of ~$560M, LHC is #3 behind Amedisys ($1.25B) and Gentiva (~$1.1B) and ahead of #4 Almost Family. These four operate in an incredibly fragmented industry of $70B/year (though most of their attention is on the $20B year Medicare FFS market). The vast majority of care is delivered by thousands of small, single-market agencies.

The key to home health is capturing attractive referrals and efficiently managing agency operations. Amedisys and Gentiva have developed and marketed disease-specific programs and expertise to doctors, seeking advantaged access to more severely ill (and profitable to treat) patients.

LHC Group’s model differs because (1) it focuses on rural markets and (2) about 50% of its revenues come from agencies operated in joint venture with hospitals. At the end of 2011, LHC had 62 of these joint ventures managing ~120 individual agencies. While the JVs do not get all the referrals for newly discharged patients (the doctor and the patient make the decision on agencies) the JVs can tap into the brand value (the JVs use the hospital name) and potential for tighter integration into the patient flow. LHC’s focus on achieving Joint Commission accreditation (per LHC, only 7% of home health agencies have) further strengthens its appeal for hospital partners.

Why go private?

It is easy to see why LHC might want time off the publicly traded stage. The industry has been under intensive federal investigation for billing practices linked to the delivery of unnecessary care. Further, policy makers have introduced multiple changes to govern utilization and reduce prices. Big changes include:

- reducing the base episode reimbursement by ~5% in 2011, and another ~2.4% in 2012 with further reductions planned for the coming years

- introduction of requirement for patients to have a face to face encounter with a physician near the time of initiation of home care as well as an assessment of patient’s course of treatment at least once every 30 days to be sure the (more profitable) therapy visits are required

And policy makers are not done: more cuts through 2017 are mandated by health care reform. MedPAC is also recommending shifting the balance of reimbursement away from (more intensive, more profitable) therapy visits to historically less profitable non-therapy visits (e.g. home health aide); and introducing a sizeable co-pay (e.g. $150) for care not preceded by a hospitalization.

All of this has taken a sizeable chunk out of the industry revenue growth, gross margins and valuation:

Industry leaders are changing their business models: for example, serving a broader patient lifecycle by a major move into hospice care (Gentiva bought hospice provider Odyssey for $1B in 8/10; Amedisys has been acquiring various hospice providers as well such as Beacon in 4/2011) or diversifying payer exposure by more aggressively pursuing commercial business (Amedisys getting contracts with Humana, United Health in Southeast and BCBSGA/Wellpoint).

LHC did not make these major kinds of moves when valuations were higher (pre Q2/2011 when the new CMS referral requirements hit) and an attractive diversification play as a public company may now be out of reach. PE investors, however, can see a longer-term trajectory and have the resources to fund the investments. Where could LHC be going?

What is the opportunity?

My view would be that LHC is uniquely positioned for a bold play in post-acute. Consider this opportunity narrative:

Value at stake

- Hospitals are on the hook for post-acute. Looming readmissions penalties are just the tip of the spear: Broader changes in Medicare reimbursement, comparable moves by commercial plans and the growth of risk-taking providers will intensify the pressure on top line (e.g. referral flow as a result of ACOs and PCMHs being selective in their hospital partners) and bottom line (e.g. penalties).

Barriers

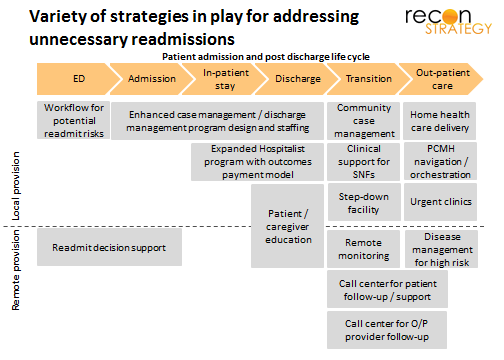

- There are no quick fixes. Top performing hospitals have invested years in building interlocking strategies that straddle the hospital walls (see exhibit). Piecemeal vended products/services inserted into an otherwise unreformed workflow will fail. Real solutions must be built on a solid understanding of and partnership with the local delivery system.

- Home health is currently underutilized in addressing post-acute: Home health could be a critical lynchpin for post-acute patients — not only because of the care delivered but also because the frequent patient contact during a critical part of recovery — but today’s incentives and operating models prevent agencies from playing an effective role in early warning and intervention.

How LHC can address the barriers

- LHC’s hospital joint ventures create a strong local platform through integration with the discharge workflow (enabling timely visits with post-discharge patients and alignment on care to be delivered) and tighter partnerships with physicians around patient management.

- LHC’s on-going roll-out of the market-leading point-of-care IT solution Homecare Homebase system may help support tighter integration with the rest of the delivery system from an information exchange, care management and workflow standpoint (in particular its Provider Link capability).

- LHC has tested the feasibility in post-acute: LHC is piloting approaches that have taken readmissions down from a national rate of ~20% for Medicare population to ~9% (Mobile Alabama pilot discussed during the Q4 2011 earnings call). Some simple math would demonstrate the near-term value of replicating these results elsewhere (for example, the four hospitals in the latest JV partner – the Baptist Health System in Alabama – all have readmission rates indistinguishable from the national average).

Potential roles of PE investment

- Funding the investments required to scale-up and roll-out the readmission reduction strategies piloted in Mobile.

- Coupling LHC with other “outsourced” parts of the discharge-to-readmit value chain such as a sizeable ER outsourcer or hospitalist/extensivist group. A combined organization could deliver a more comprehensive solution, take on larger performance-based contracts and open a cross-sell opportunity. For example, bringing LHC together with a sizeable ER outsourcer or hospitalist group.

- Outside of home health: LHC’s “hospital within a hospital” approach to long-term acute care could expanded beyond the Louisiana market where it is currently concentrated; or be used to opening other service lines among hospital partners.

Not a bad pitch! Be interesting to see if the eventual deal for LHC Group contains any of these points.