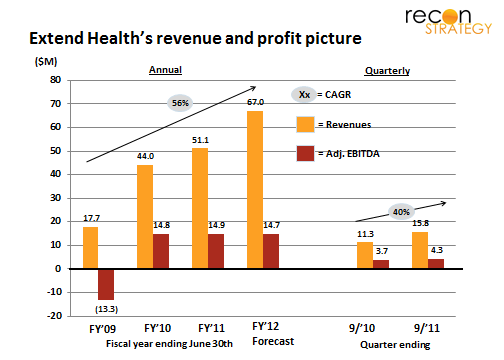

With its acquisition of Extend Health, Towers Watson has ensured that (1) PHIXs will be a key competitive arena among the major benefits consultants and (2) that it has taken the lead. Extend Health serves 170K members and has annual revenues of ~$50M+, EBITDA margins of ~30% and a growth rate in the most recent reported quarter of 40% vs. a year ago (all taken from the S-1 filing and acquisition press release).

Two leading competitors have been publicly discussing their capability building:

- Aon Hewitt began their exchange in April 2011 with a goal of serving retirees first (in 2012) and opening it to current employees in 2013. They are committed to spending $75M over the next couple years on a category that includes exchanges (and hinting in the Q1 2012 analyst call that it would be mostly spent on exchanges).

- Buck Consultants (part of Xerox) built a retiree exchange likely leveraging the capabilities of its parent Xerox and, in particular the ACS subsidiary. (I am guessing this exchange is the My Medicare Advocate offering associated with ACS, which, if this is the case, suggests 4 major customers: ConAgra, Heinz, Telcordia and Xerox). Note that Xerox/ACS are also active in the state health insurance exchange market

Up until last week, the other big benefits consulting houses — Towers Watson, Mercer, Gallagher, Lockton and Willis — had been content with an alliance arrangement with Extend Health (in fact, the Towers Watson and Mercer partnerships are less than a year old). Not anymore.

By buying the asset, Towers Watson has achieved several objectives:

- Ensured that it can capture more value from advising employers to transition retirees into Medicare Advantage (on average, Extend Health earns between $350-390 per member per year in commissions from the health plans)

- Ensured it can capture value from advising employers to transition into defined contribution plans for regular employees (which Extend Health and other retiree-focused PHIXs can support with some investment) – and likely also enhance stickiness of these accounts

- Leapfrogged Aon (which is still in early stages with its Exchange) by owning the largest operating retiree exchange which has achieved at-scale operations and profitability

- Disrupted Mercer and others that may have been relying on a partnership approach to PHIXs (note that Mercer announced its own ambitious plans for PHIXs in March but how they are doing it and the degree of reliance on Extend Health has not been publicized)

- Created a cross-sell opportunity: per Extend Health’s S-1 filing, only 1-2% of their sales are through partners, the rest of their employer relationships are direct and include 150 public and private companies of which 30 are F500. Stands to reason that a significant share of these is not Mercer customers today and therefore cross-sell targets.

Towers Watson will also need to have an interesting discussion with United Health. Back in 2010, Towers Watson and United partnered on something called the “Retiree Health Collaborative” which sounded very much like a private exchange focused on a single health plan’s products. At the time, Towers claimed seven clients and 25K retirees but not much has been publicized since 2010. With the Extend Health acquisition, Towers Watson appears to be betting on PHIX’s with multiple plan offerings. Fine. Except: with the Extend Health acquisition, their (former?) partner is now the second largest customer: Extend Health gets ~20% of its commission revenues from selling United’s retiree products (behind Mutual of Omaha with ~35% share of commissions in the most recent periods).

Implications

- Brokers should not expect much of a commission bump from retirees being rolled off corporate benefits: the PHIXs will allow their benefit consultant parents to capture these members and the commissions

- Expect Mercer, Gallahger and others to seek alternative options on a PHIX quickly. The good news for them there is that there are plenty of private label suppliers / capabilities sellers out there.

- If the biggest benefits consultants are committed to integrating PHIXs in their business model, they are going to aggressively counsel against health plan-specific PHIX (hence, I suspect, the relative quiet regarding the Towers Watson/United Retiree Health Collaborative). Plans seeking to offer their employer clients plan-specific PHIXs will need to be very clever in creating a compelling value proposition.