Summary

- Two major hospital systems have agreed to a joint venture to explore growth opportunities on a “case by case” basis

- One system is a major non-profit, the other a PE-backed for profit serial acquirer; their strategies, capabilities and geographies of both partners do not overlap

- The venture is likely focused on sharing capabilities and allowing each partner to take those back to their core markets

- Given the complementary skill sets, competitors to either system would be wise to expect upgrades in traditional weak spots

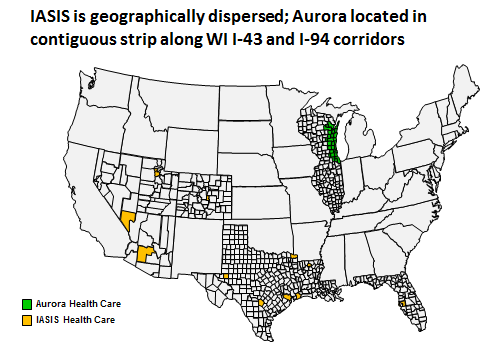

A few weeks ago, two major provider systems — IASIS Healthcare and Aurora Health Care — announced a “wide ranging” joint venture to pursue “acquisitions, new constructions, management of facilities and development of clinical services.” It is not an obvious partnership: Aurora is the largest non-profit system in eastern Wisconsin with 15 hospitals (several nationally ranked) operating in a single, contiguous geography, a large base of employed physicians and robust vertical referrals paths (clinic to community hospital to tertiary AMC to home health providers). IASIS is a PE-backed, for-profit serial acquirer with a portfolio of 19 unranked and often isolated hospitals scattered across 7 states (none near Wisconsin), a very nascent physician employment strategy and a mid-size Medicaid managed care plan in Arizona. (Feels like the premise of a classic Hollywood rom-com, doesn’t it? Classy “uptown girl” meets street-wise on-the-make “downtown boy”)

Not about capital

Given recent deals between non-profit providers and private equity (e.g., Ascension Health did with Oak Hill in 2011) and

IASIS PE ownership, you might think the venture is about access to capital. But Aurora has a better credit rating than IASIS and more cash ($305M vs. $64M). Given that IASIS PE owners put the company up for sale in March they probably don’t want to lock away yet more capital in a joint venture. Besides, if its capital it wants, Aurora is probably big enough to form a relationship with private equity directly (as indeed, Aurora’s CEO noted that Aurora could have financed the cancer center project on its own).

Clue: the first venture is a cancer clinic

The joint venture’s first announced project is a 10K sq. ft., $19M cancer center in Kenosha, WI. Aurora seems to be bringing all the assets: high-performing cancer capabilities in the system; an in-market referral base (given its nearby 73-bed medical center); and know-how: the center will be a smaller version of the one Aurora launched on its own in Grafton, WI, in March 2012.

While IASIS may not be bringing much, it is getting a lot out of this joint project: Cancer can spin off a lot of profitable procedure revenue, but in each of its major markets, IASIS faces tough competition (Salt Lake City: University of Utah Health Care; Phoenix: Banner/MD Anderson; Houston: MD Anderson; Tampa: Moffitt). Right now, IASIS is focused on other service lines (e.g. revitalizing the cardiovascular program in the recently acquired St. Joseph’s hospital with a new surgeon). By participating in the Kenosha project, IASIS will learn more about how to compete in cancer which it can roll out to its home markets afterwards.

Our theory – capability exchange

That is what we think lies at the heart of this otherwise odd partnership: it is a vehicle for sharing “up-market” and “down-market” expertise. Aurora and IASIS operate successfully in different provider segments making their skills complementary; but they also operate in widely separated geographic markets – so they are unlikely substitutes. Sharing capabilities carries few risks and can offer benefits for both. The partners said they would be evaluating opportunities on a case-by-case basis and spending time learning about each other’s capabilities. (worth noting that even if a particular opportunity is green lit for a venture, a lot of the know-how can be exchanged as part of wide-ranging due diligence).

Here are the intriguing capability “trades” which the joint venture could facilitate:

For IASIS (besides more service line expertise like cancer):

Physician strategy. IASIS employs a lot fewer doctors than Aurora despite having a physician employment strategy in place for 5+ years. Aurora has about 1500 physicians (~0.74 per bed) while we estimate IASIS has between 150-250 physicians (~0.04-0.06 per bed). Few aligned physicians coupled with the second-tier standing of IASIS facilities in most markets makes them easy to bypass. As a result, IASIS has both lower average inpatient occupancy (48% vs. 58% vs. Aurora in 2011) and lower share of outpatient revenue (40% vs. 62% for Aurora in 2011). Getting a closer look at Aurora’s successful models (e.g. Aurora’s joint venture with BayCare) may help IASIS turbocharge its physician strategy.

Commercial risk / ACO models. Aurora is a Pioneer ACO and has two commercial insurance product ventures (with Aetna and separately with Wellpoint). IASIS faces competitors pursuing similar strategies in its key markets (e.g. Banner in Arizona or Memorial Hermann in Houston). Looking over Aurora’s shoulders and learning about how these models work would help IASIS refine its competitive strategy (even if IASIS won’t be able to fully replicating such arrangements until it has a turbocharged physician capability). The Banner story is particularly intriguing given its alliance with Aetna: IASIS may be able to get a pretty good idea of the Banner-Aetna playbook from a “behind the scenes” glimpse at the Aurora-Aetna operation.

For Aurora:

Surviving on Medicaid. One of Aurora’s major headaches is the Aurora Sinai hospital in Milwaukee. It is a ~200 bed safety net hospital that lost $20M last year and is anticipated to lose $30M this year) (compare with system-wide operating income of $36M for the first half of 2012). Closing the facility is not politically viable so turning it around is key. IASIS has made its business acquiring under-performing hospitals and turning them around, often surviving potentially crushing body blows in Medicaid reimbursement rate and charity care share. Take, for example, IASIS experience in Arizona: three IASIS hospitals operate with an average 80% discount vs. charges while competing hospitals average 67%. Compare the financial trajectory of IASIS Arizona vs. Aurora’s Sinai hospital over the last three years:

Note that IASIS and Sinai had the same (negative) profitability in 2009, but then IASIS steadily did better than Sinai despite consistently 10% lower occupancy. Aurora would no doubt be interested in learning and deploying some of IASIS tactics in Sinai.

Stand-alone community hospitals. Despite its broadly contiguous service area, Aurora has a number of facilities in relatively isolated geographies (Lakeland, Manitowoc) or competing vs. small, local, unranked facilities (Summit, Hartford), both with low occupancy rates. Many of IASIS hospitals are similarly isolated and can offer expertise on how to management them most effectively.

Going forward

The venture is described in ambitious terms, but we expect it will remain largely incremental once the flurry of comparing capabilities is completed. The end game will be managing a portfolio of tuck-in businesses under the umbrella of one partner or the other (like the cancer venture). Some parent assets might be committed to the venture’s control (e.g. if joint venture were to get an Aurora Sinai hospital management contract or consolidating some shares services). It is also worth noting that all of the new ventures could be located in the Aurora core markets and still achieve the capability sharing opportunities noted above.

Aurora is already managing a broad enough portfolio of ventures and partnerships and will want to keep the borders between them very clear. Besides, it also has a history of bold alliance announcements followed by very specific and tightly defined business strategies (e.g., in 1996, Aurora made an alliance with Illinois’ Advocate Health Care for joint ventures, combined network and shared payer negotiations; in the end, the alliance focused on consolidated labs into a joint subsidiary ACL). The IASIS-Aurora joint venture will likely have the same “funneling down to a few specific businesses followed by focused execution” trajectory.

A focused portfolio of businesses may also be the right thing for IASIS. IASIS is already a complicated business for TPG to sell given its scattershot geography, limited physician depth and small bolt-on Arizona Medicaid business; indeed IASIS could be more valuable piecemeal than as a package. If such a “slice up” strategy were used to sell the business, the joint venture would be hard to value. The best thing this joint venture could do is add to IASIS skill sets in its core vs. being a real driven of bottom line and valuation.

And that it is well suited to do.

This note was co-written by Shan Soe-Lin and Tory Wolff, both of Recon Strategy