Summary

- Highmark and the West Penn Allegheny Health System (WPAHS) are not aligned on their vertical strategy to counter UPMC in the Pittsburgh market

- WPAHS can only absorb a portion of Highmark’s care demand now being met by UPMC. So its upside on the success of Highmark’s vertical strategy is capped

- Highmark would prefer a deal with UPMC if it get reasonable rates: the status quo looks better than the uncertainties of a vertical model build

- A large share of UPMC’s business still comes from Highmark which makes UPMC vulnerable. Ironically, the more credible Highmark’s vertical model threat, the more likely UPMC will be willing to strike that deal

- Highmark and WPAHS need to create a set of options whereby — even if Highmark cuts a deal with UPMC — WPAHS is significantly better off as well. This may diminish Highmark’s negotiating flexibility, but will increase the likelihood that UPMC will come to the table which is the key strategic point

Earlier this month, a West Pennsylvania judge put a temporary patch over the most recent crisis in the Highmark and WPAHS relationship. In August, the new Highmark CEO privately pushed for bankruptcy to clean up the WPAHS balance sheet before acquisition. WPAHS countered by publicly accusing Highmark of violating their agreement and reopened themselves to other bidders. Highmark then took WPAHS to court. The judge ruled that Highmark had done no incurable damage to the deal and enjoined WPAHS from seeking other acquirers. Both parties are back at the negotiating table.

It is a puzzle why two partners who need to cooperate to succeed vs. UPMC are shooting at each other instead. This is more than just a ripple. The decline in trust since the summer will require significant reassurances to get back on track. Otherwise, WPAHS may continue to be “difficult” and the cost in lost time and opportunity may well exceed what Highmark was hoping to save through the bankruptcy.

Brief recap

Pittsburgh has two large tertiary systems – the large and highly successful UPMC and the much smaller and struggling WPAHS. Last year, Highmark and UPMC contracting negotiations broke down (Highmark claimed UPMC was looking for 40% increase in its rates) and Highmark launched a strategic effort to build its own provider system with WPAHS as its tertiary crown. UPMC signed contracts with Aetna, CIGNA and United (February 2011) giving them competitive footholds vs. Highmark. Western Pennsylvania is now seeing “unprecedented competition in the local health insurance market as a result of national carriers re-entry into the local market at the invitation of UPMC”. Most recently, Highmark had a change in CEO. Dr. Ken Melani, the former CEO who architected the strategy and the deal with WPAHS, has been replaced by Dr. William Winkenwerder who initiated the push for WPAHS bankruptcy.

Highmark’s bankruptcy proposal

Highmark reportedly wants to reduce the $1.5B acquisition price for WPAHS ($1B in assumed debt and $475M in facilities upgrades) by $600M through a bondholder haircut and transferring retiree obligations to the federal Pension Benefit Guaranty Corp. Of course, the balance sheet restructuring won’t solve the core operational problems — WPAHS is losing a lot of money before interest expense (see chart) — but it will help.

Bankruptcy would relieve the Highmark business plan of paying for the grievous consequences of WPAHS’s previous strategy. Restructuring could also (perhaps) free up those same funds for completing the vertical provider model it is building to compete vs. UPMC: right now, Highmark and UPMC are in a bit of a Jerry Maguire / Bob Sugar type race for providers and so far Highmark seems to losing. This past year, they bought a number of prominent practices including Premier Medical Associates (65 doctors) but the total so far is around 100 doctors while UPMC added 300 to its roster over the same period.

What’s the real game?

Highmark and WPAHS are in a complex, multi-stage game right now. They may look irrational but, in fact, what Highmark and WPAHS have been doing over the past couple months is fully rational given the potential pay-offs of this game. That’s why we argue that this most recent legal patch-up will prevent the recurrence of feuding and posturing between Highmark and WPAHS.

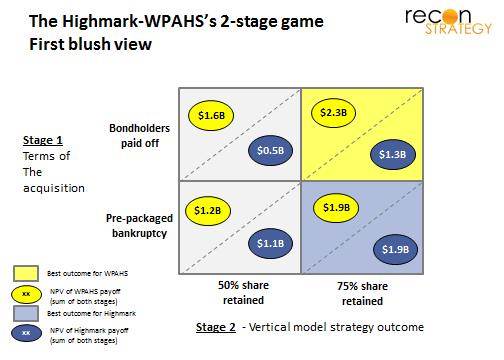

First, let’s start with a simple (as we will see: simplistic) specification of a two-stage game: The first stage determines how big the one-time payoff to WPAHS will be for joining Highmark’s vertical model. The second stage – the battle for lives between Highmark’s vertical model and UPMC – will determine how much share Highmark retains (once the Pennsylvania Governor-enforced deal which kept UPMC in the Highmark network expires December 2014)

The first stage has two possible nominal outcomes: Highmark pays various WPAHS stakeholders either $1.4B without a bankruptcy or $900M if there is a bankruptcy. Payment to bondholders will probably not be valued by WPAHS as much as new investments or securing the employee pensions. The bankruptcy would cripple WPAHS’s standing among investors (already severely damaged with recent downgrades) and cut off prospects for independent access to capital and a future uncontrolled by Highmark. What WPAHS really loses is the value of opportunities enabled by good access to credit.

The second stage payoffs are the profit streams earned on Highmark lives earned from insurance and from care delivery. The profit depends on how much share Highmark retains once UPMC leaves its network (we use either 50% or 75% of share retained for the analysis) and how much of that care is delivered by WPAHS as part of the vertical model (we simplify by assuming all the former UPMC care is up for grabs for WPAHS but do not consider other care delivery profit streams Highmark will earn from the vertical model (e.g., from other provider practices they purchase) as they are not relevant for this game.

Add it all up, here’s what you get (we won’t specify the detailed assumptions here because there’s a lot going on in each payoff calculation – please email if you want to discuss specifics):

A few points: The payoffs look skewed in WPAHS’ favor because of:

- Highmark’s big payment for WPAHS in the first stage (negative drag on Highmark’s payoffs and partially positive for WPAHS) and

- the relatively high profitability of incremental Highmark lives for WPAHS in the second stage (these are commercial lives, after all, and WPAHS is operating at 60% capacity, so the marginal profitability will be high).

Of course, the new vertically integrated Highmark parent will formally earn the profits of WPAHS in the second stage – but the provider profits will largely get WPAHS back to modest profitability as a business unit so cannot be extracted for other uses by the parent – we have left them in the WPAHS payoffs because they will go to sustaining the system.

In this game, the best outcome for both sides is to make the vertical model successful irrespective of what happens in the first stage. WPAHS would rather get the $1.9B in present value from a successful vertical implementation and a bankruptcy (lower right hand outcome) rather than the $1.3B it would get if there was no bankruptcy and the vertical model fails (upper left hand outcome). Yet, WPHAS chose to very publicly disagree with its partner, damaging confidence among physicians that Highmark / WPAHS is the better home for them vs. UPMC. (Note also that WPAHS’ threat to find other bidders is not really credible. Any acquirer will want the same balance sheet clean-up as Highmark and would discount the value of Highmark patient flow given that the break-up was not amicable.) Is WPAHS behaving irrationally?

Although it sure looks that way, the answer is no. The first blush view is missing two key points:

First, WPAHS payoffs are, in fact, not very sensitive to the success of the Highmark vertical strategy. Right now, Highmark buys $1.5B of care a year from UPMC but WPAHS has capacity to deliver only another $600M of care a year in care. The WPAHS upside is capped far below the tertiary system care demand of Highmark’s membership. As a result, the WPAHS payoff if Highmark retains 75% of its current lives will be no better than if it retains 50%.

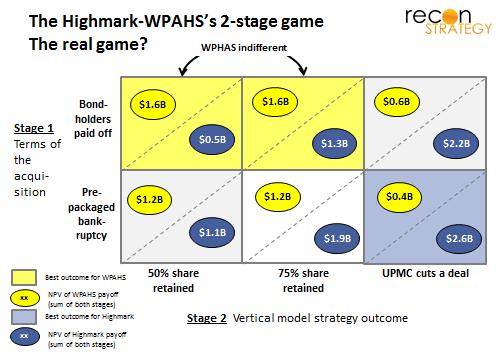

Second, there may be an additional outcome to the second stage of the game which looks dramatically worse for WPAHS and dramatically better for Highmark. One point came out of the court testimony: WPAHS asked the Highmark leadership to commit to completing the acquisition after the bankruptcy and Highmark pointedly refused to do so. The implication is that the vertical strategy is still a negotiating ploy to get UPMC to cave on pricing (e.g. rolling back its reported request for a 40% rate increase). UPMC would likely insist that Highmark not compete with UPMC so the WPAHS deal not be consummated or WPAHS would be put back on the block. WPAHS could be lucky to be left with their current slice of Highmark annual care revenues (about $300M/year) and perhaps the already committed $400M in investment.

So the real game looks something like:

Very little alignment across WPAHS and Highmark under these payoffs! WPAHS may fear being left at the altar with a ruined credit reputation (Highmark’s preferred lower right box outcome). It makes, therefore, perfect sense to stir up some doubt about the vertical model’s success to achieve a better outcome in stage 1. A court mandated patch up is not going to ease those anxieties.

What’s next: changing the payoffs

How can both sides re-align their interests during the next set of negotiations?

To get a different outcome in game theory, you need to change the game or change the pay-offs. To my mind, it is not really credible that Highmark would walk away from a deal with UPMC despite the investments to date in the vertical model. To get WPAHS cooperation in the vertical build, therefore, Highmark needs to sweeten the payoffs to WPAHS whether the vertical model succeeds or a deal with UPMC is struck. How? Here are a few thoughts to consider:

(1) Increasing WPAHS payoff if the vertical model is successful

- Commit portions of funds Highmark retains through the bankruptcy process to expanding WPAHS capacity to absorb more of the potential patient flow — conditional on vertical model deployment and reaching certain share targets

- Commit portions of the funds Highmark retains through the bankruptcy process to continue the vertical model build now and purchase more physician practices which can be integrated into WPAHS

(2) Increasing the WPAHS payoff if a deal is struck with UPMC

- Commit portions of the funds Highmark retains through bankruptcy to jointly invest in increasing capabilities even if the vertical model falls through (thereby reducing the risk of WPAHS being left stranded without access to capital) – especially around care quality and increasing sophistication of care via partnerships with national top-tier providers.

- Provide WPAHS some right-of-first-refusal purchasing option on the Highmark-acquired practices if the vertical build falls through.

- Help WPAHS develop an ability to manage with risk (ACO, capitation) perhaps together with Highmark owned practices. Put a long-term contract in place moving them down this path. Commit to allowing all-payer approaches if the vertical build does not happen. Eventually this should enable WPAHS to secure attractive rates from other insurers in the market.

- Build an attractive narrow network product with WPAHS as its center; commit to making this product compatible for Essential Health Benefits and putting it on the Exchanges (Highmark’s private exchange, any broker-led exchanges and Pennsylvania public exchange)

- Orchestrate a partnership between WPAHS and a branded nationally ranked player (on the model of the Mayo-Heartland Health or the Columbia-Sarasota deal) now to help address perceived quality gap vs. UPMC. Cleveland might be the obvious candidate, given previous talks about collaboration post acquisition

- Support telemedicine and cross-referral opportunities across Highmark’s overall service area (e.g. West Virginia University hospitals in Morgantown down I-79), allowing WPAHS to reach beyond its current catchment area.

The trick is this: Highmark must remember that, even if it can strike a deal with UPMC, a stronger WPAHS is still in its best interests. So finding ways to lock in enhancements to WPAHS viability in ways which cannot be circumvented by a contract with UPMC is a win-win. And WPAHS must plan to play a “long game” focused on cost effective care and use the Highmark partnership to get on that path, no matter what the outcome of the vertical build.

(This note was written by Tory Wolff and Shan Soe-Lin of Recon Strategy)