Market for outsourced revenue cycle management could be big

The revenue cycle management (RCM) vendor industry is about $2.0B for hospitals and $11 billion for physicians today. The market is constrained because most providers do their own RCM. Vendors only have a ~10% penetration among hospitals and a 25% penetration among physicians (implying that the potential combined hospital and physician market is $60-70B). However, RCM as a function is getting more complex and outsourcing could quickly start looking more attractive:

- Value-based contracting models raising the stakes in documentation, reporting, benchmarking, and dispute resolution

- Continued proliferation of high deductible plans increasing patient financial risk while expanded coverage through ACA is reducing the appropriateness of charity care designation

- New coding standards (ICD-10) requiring large system and talent upgrades

- Continued pressure on the administrative cost structure (revenue cycle management can add 1 employee to a hospital for every $5-6M in NPR)

- New EMR implementations requiring retrofit of the RCM approach

- Rapidly evolving provider affiliations and combinations creating challenges with multiple legacy systems, operating models and contract terms

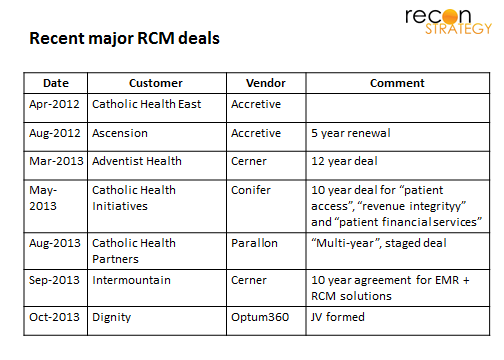

The big bet for RCM vendors is that the increasing complexity will drive a surge of outsourcing in the coming years. The fast pace of deals among major hospital chains supports that view:

Incumbents are a bit of a mixed bag

Today, the market is split across a few larger scale players (e.g. Accretive, Conifer, MedAssets), big software vendors (e.g. Optum) and a long tail of 200+ vendors. Here’s a quick breakdown of the major player segments:

Accretive Health is the leading player in this market, earning $1.0B in annual revenues, operating large offshore processing and call centers and its key customer relationship (Ascension Health, the #1 non-profit chain with 100 hospitals) solidified by an ownership stake. The company has been struggling recently with the taint from a Minnesota AG lawsuit alleging violation of consumer protection laws (recently settled but at the cost of a major account – Fairview), an on-going delay in financial filings because of a review of revenue recognition policies, and a change-out of its C-levels. Despite these challenges, Accretive renewed the Ascension business, won the Catholic Health East business and, in April of 2013, won Salem Health in Oregon (2 hospital system).

RCM subsidiaries of major hospital systems such as Conifer (a subsidiary of Tenet and serving its parent along with the #2 non-profit chain Catholic Health Initiatives) and Parallon (subsidiary of HCA and serving among others, Catholic Health Partners and Lifepoint). These players have the scale and credibility from serving their parents and, in Conifer’s case, references for serving ACOs (CHI has several underway). But some hospitals might be reluctant to sign up if they compete with the parents (Note:, the overlap between CHI and Tenet and between HCA and CHP is very limited, consistent with a view that systems don’t sign RCM deals with the subsidiaries of competitors).

EMR vendors have been getting into the game notably Cerner (with its 2013 deal with Adventist — the #4 non-profit system — and possibly encroaching on Accretive’s turf with its 2013 deal to roll out RCM software across Intermountain sites) and Allscripts (for example its deal with Mercy in Maine). These deals are attractive extensions where the providers have the vendor’s EMR in place; the value proposition for other systems (most importantly, market-leading Epic, is a lot less clear).

The long tail. There are a large number of other vendors in the market offering component RCM services, technology and performance improvement consulting. These largely serve to prop up providers retaining in-house solutions. Included in their number was, until a few weeks ago, the United subsidiary Optum which mostly sold software to support component services in RCM but had little traction in end-to-end outsourcing (its most widely touted reference dates from 2010 with Bethesda Healthcare, a 550 physician, 400 hospital bed provider). This status changed with the Dignity deal.

Enter Optum360

The Dignity-United deal to form an RCM joint venture is designed to position Optum to win in end-to-end outsourcing market. Dignity will provide its experienced, large scale processing centers with 1,700 employees in return for a minority share. Optum will contribute its technology expertise and 1,300 employees in return for a majority share. The business will have a starting platform: Dignity will pay the new venture $250M a year for end-to-end RCM (or about 2.3% of its net patient revenue, in line with Accretive’s deals with Ascension and the Henry Ford Health System).

The RCM JV, Optum360, will have:

- A major reference client putting Optum on a par with the other major end-to-end outsourcers: Dignity is the #5 non-profit chain of 38 hospitals – among the largest still available given that #1-#4 of the nonprofit chains are already sewn up (#1 Ascension and #3 CHE/Trinity with Accretive, #2 CHI with Conifer, and #4 Adventist with Cerner). The reference also helps mitigate concerns about using a United subsidiary for their RCM as United is also one of their customers.

- A domestic processing capability and a model of integrating legacy employees. Some customers are cautious about (1) laying off their RCM employees without an option to be rehired by the outsourcer and (2) handing over the sensitive business of healthcare bill collections to offshore call centers. If Optum360 retains the strategy they used for Dignity, it would differentiate its offer from Accretive.

- The sophisticated technology capabilities and payer relationships of Optum which could help differentiate particularly vs. the Conifer and Parallon, constrained by the capital budgeting and strategies of their hospital parents

- EMR neutrality (Dignity is an Epic system) which will prevent their customers being limited to those on a particular system (a feature of Cerner’s and Allscript’s RCM strategy)

- A qualified lead list, given Optum’s footprint among providers.

Of course, Optum already had or could have had most of these components (except #1) in place before the deal. The Dignity reference client is the game-changer. That’s why, despite the potential baggage of having Dignity as a JV partner (I doubt Sutter in California or Banner in Arizona – which appear to be two insourcers today – are going to sign with Optum360 anytime soon, Dignity’s disaffiliation from the other Catholic systems may leave some lingering mxed feelings), United was willing to take on a partner and share the profits. There just was no feasible pathway through organic growth or vendor roll-up which would match the power of a major hospital chain reference (and someone else would have gotten the Dignity business in the meantime).

Above all, United was probably focused on speed: recall the pace of big deals with big systems has been remarkable over 2012 and 2013. Big pieces of business are getting locked up now. By marrying into the Dignity family, Optum hopes to spring itself into respectability among system CFOs as a credible partner in end-to-end outsourcing right at the time when they will want to hand RCM headaches over the someone else.