Please see update at end of post.

If value-based care broadly delivers on its promise to reduce hospital admissions by providing more timely ambulatory care, a lot of today’s bed capacity will end up redundant and stranded. How can we navigate to a new equilibrium? Recent developments in the New Orleans area (whose population size still has not recovered from Katrina and is potentially therefore a model case of oversupply) may offer some window into future endgames for resolving the supply-demand imbalance.

Acquire, unbundle, and selectively shut-down

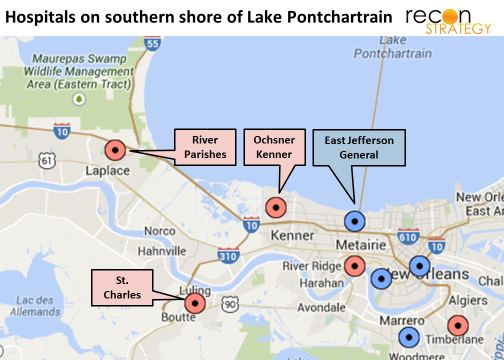

One approach is for an integrated system to acquire ailing assets, keep the viable services, and, for the rest, redirect patients into neighboring sites with free capacity. This is the approach that Ochsner (the largest and — of late – boldly acquisitive delivery system in New Orleans/Baton Rouge area) has taken with 93-bed River Parishes Hospital, which was acquired from Lifepoint earlier this month.

The plan is for inpatient services at the hospital to be closed and 60% of the staff let go. Ochsner will maintain select ambulatory services such as emergency, outpatient diagnostics, and primary care. Unstated is what will happen with the specialist offices Ochsner was operating at River Parishes (cardiology, neurology, obgyn and women’s services) and it may be contingent on the extent to which they depend on inpatient volume (e.g., the tele-stroke program Ochsner operated at River Parishes). Ochsner already had plans to build ambulatory services in the St. John the Baptist Parish where River Parishes Hospital is located. Those plans will continue and River Parishes’ legacy services will be relocated once the new site is complete.

Rationale

Why acquire only to dismantle? Two thoughts: By maintaining the current ambulatory footprint, Ochsner is preventing a competitive entrant from filling the vacuum before the new Ochsner site is up and running. Also, by controlling key ambulatory services, Ochsner can guide referral volume into their system. It would make sense for the more sophisticated diagnostic, surgical and inpatient volume to be shifted to Ochsner Kenner, a 160-bed facility 20 miles east on I-10.

Kenner has had stubbornly low utilization since Ochsner acquired it from Tenet in 2006 (and despite reducing licensed bed capacity from 200+ shortly before the Ochsner acquisition to 110 in 2014 per Ochsner quarterly filings). If all of River Parishes’ admissions could be redirected, Kenner occupancy could go from ~50% to north of 70%, and the volume of treating some conditions (heart failure, major joint replacement) would increase by ~55-65%. The added volume would enhance Kenner’s economics and competitiveness – important given that the 420-bed East Jefferson General Hospital is just a few more miles down I-10 from Ochsner Kenner and probably could just as easily absorb River Parishes’ patients.

Add in a deal strategy dividend

Interestingly, Ochsner has been in discussions vs. a few other entities to acquire East Jefferson for a year, but appears most recently to have walked away from further talks. The East Jefferson sales process has been marred by controversy – but that does not seem to have stopped East Jefferson from expanding services (such as a low acuity track in the ER to speed care or opening a new oncology wing). By solidifying control over referral volume from the west (including taking control of the 59 bed St. Charles hospital to the southwest earlier this year), Ochsner has bolstered the position of Kenner. Any other buyer for East Jefferson than Ochsner will now also be buying an uphill battle with Ochsner for referrals from the west. Ochsner will have more leverage should it return to the negotiating table with East Jefferson.

Is St. Charles Parish Hospital a counter example?

Earlier this year, Ochsner took over the management of the struggling 59-bed St. Charles Parish Hospital a few miles to the south of River Parishes in Lulang, but has so far kept the hospital intact. In fact, shortly after the River Parishes acquisition was announced, Ochsner also announced that there would be no staff reductions at St. Charles. Yet St. Charles’ occupancy does not seem that much better than River Parishes (AHA data has River Parishes with 1,583 discharges over 93 beds implying a 22% occupancy, while St. Charles has 1,153 discharges over 59 beds for a 26% occupancy over the same timeframe). Granted, press reports do have River Parishes most recently at only 10-12 patients a night for a 12% occupancy, but there is no data on what the St. Charles occupancy is today – it may have declined comparably). Was St. Charles Parish Hospital just faster to cutting a deal and therefore spared River Parishes’ dismantling?

I would argue that the same logic that left River Parishes struggling applies to St. Charles, but right now the terms of the St. Charles deal are different and it is still early on in the process. It appears that Ochsner is managing St. Charles, but the parish still owns it and the hospital board retains the same “responsibilities and oversight” including intervening in Ochsner’s managerial decisions. Both Ochsner facilities that “bookend” St. Charles (Kenner in the north, St. Anne in the southwest along US 90) have plenty of free bed capacity. If St. Charles occupancy does not turn around, losses will add up and, at some point, I would speculate that the parish will offer Ochsner a firmer hand and will do similar “surgery” to the St. Charles business model – keeping ambulatory services in place while directing inpatient volume north or south on US-90 to other Ochsner locations. Let us see what 2015 brings.

Implications

- Being the only community hospital in a local market (Lifepoint’s strategy exemplified by their initial acquisition of River Parishes in 2004) is no longer a safe bet. Inpatient catchment areas – and with them the competitive set – will expand as value based approaches take hold.

- Joining up with integrated value-based systems does not assure a community hospital’s future. The integrated systems may have their own “beasts to feed” and, as these systems take on more risk, payers will have less incentive to drive site-of-service trade-offs that benefit community hospital settings. It is up to the provider to optimize site of service within their system and they may choose overhead absorption over lowest acuity.

- While the minimum catchment area for inpatient is growing, the catchment area for ambulatory services is remaining the same or shrinking: hospitals that have built up operating models and infrastructures to support both will be challenged to preserve their economics.

- If “decoupling” inpatient and ambulatory services becomes a common practice, delivery systems will need to figure out the right model for operating stand-alone ambulatory services in a cost effective and consumer-oriented way. Legacy hospital strategies (and perhaps managers) may not be readily redeployed to the new challenge.

- If the River Parishes scenario becomes common and patients must travel longer distances for inpatient stays, they may – on the margin – become more interested in services that get them out of the hospital faster or keep them out of the hospital altogether. Home monitoring, nurse home visits etc. will benefit from the long-term trend.

Update

On May 27, 2016 Ochsner formed a JV with Acadia to build an 82-bed behavioral facility on the River Parishes site, expecting 2,500 inpatients and 3,100 outpatients a year. At the time of the announcement, Ochsner reported their EDs transferring 4,000 patients/year out for psychiatric care and area shortages in psychiatric capacity. The River Parishes story appears, therefore, to also be a case of care consolidation (general I/P care out of River Parishes) and facility specialization (focusing River Parishes on psychiatric allowing for an economically viable scale) enabling expansions of care access.

Also: St. Charles lingers on: occupancy continues to sag (average daily census of 11-12 inpatients in F16 vs. 14-15 in FY16) and finances weaken ($17M loss between 8/15 and 12/16 with cash reserves going from $7.9M to $1.2M over the same period). And, although outpatient revenues are up 23% (vs 6% for inpatient) between FY14 and FY16 and the hospital has been equipped with Epic integrated with Ochsner, Ochsner seems to still be figuring out a management team to turn the operation around. There have been 3 Ochsner-appointed CEOs over 2 years – the current one announced in February 2017 (along with new chief operating and nursing officer in June, 2017). Since the St. Charles losses do not appear to be consolidated into Ochsner financials, perhaps they can still be patient until St. Charles Parish sees the need for a sustainable solution.