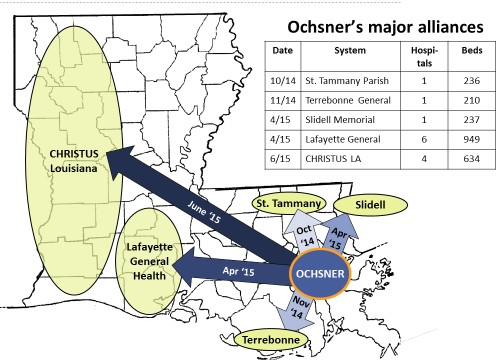

Over eight months between October 2014 and June of this year, Ochsner formalized alliances with five major provider systems in Louisiana. The first wave (with St. Tammany Parish, Terrebonne and Slidell) reinforced Ochsner’s stronghold in New Orleans. The second wave (with Lafayette General and CHRISTUS) secured pathways to markets west along I-10 and the coast and northwest along the I-49 corridor to Shreveport.

This collection of alliances — dubbed the Ochsner Health Network (OHN) — is effectively statewide with ~30% of the hospital beds and ~30% of the physicians. Key components of the alliances include: a joint clinically integrated physician network, joint investments to enhance local access to clinical resources, operational collaborations to remove cost (e.g. procurement), retention of local control and governance. Sir Bernard Montgomery – famous British general and architect of Operation Market Garden which landed three paratrooper divisions behind enemy lines to secure a sequence of three critical bridges to and across the Rhine in 1944 — would have admired Warner Thomas’ boldness.

Taking ground fast via partnership

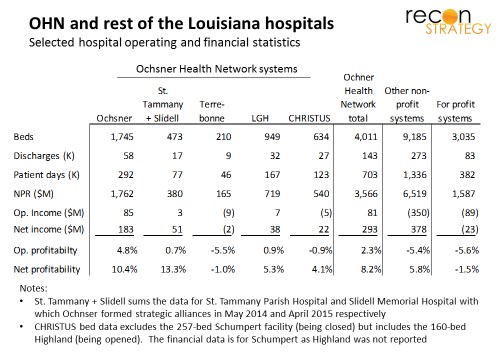

Coming together without a change of control is an increasingly noted model for system growth. Change of control is fairly irreversible, therefore usually involves a motivated “seller” (struggling with performance or strategy) and takes time as irreversible decisions weighted carefully by owner and regulators. By contrast, Ochsner has moved quickly to assemble a strong set of partners (at least by Louisiana market standards): each (with exception of the smallest partner, Terrebonne) are within sight of operating breakeven while the rest of Louisiana’s hospitals average a -5 to -6% operating margin (whether for-profit or not for profit).

Partnerships can open a broad swathe of scale and capability-sharing opportunities while also allowing commitment levels to evolve as partners to gain familiarity with each other. Avoiding change of control also has the benefit of keeping the existing governance structure – focused on local success and community relationships – intact.

Value-based care as bulwark versus the coming storm

Louisiana is over-bedded (3.4 beds per thousand vs. 2.5 national average despite comparable population density of 107 residents per square mile vs. 90 national average). Each of the major systems outside of the OHN are deeply preoccupied: some swallowing former LSU hospitals privatized by Jindal (e.g. the 6-hospital Franciscan Missionaries of Our Lady Health system and the 5-hospital LCMC system), some hanging on by fingernails in corporate status limbo (e.g. East Jefferson General which was being courted by Ochsner and HCA but missed the boat with each and now bleeding red) or others locked into traditional share/rate leverage mindset (Willis-Knighton in Shreveport whose contract disputes with BCBSLA have spilled out into the press). The Jindal administration’s closure of several LSU hospitals has made a dent in the overcapacity but more painful restructuring (and the various second order effects as the underinsured reallocate around remaining systems) is inevitable.

To date and as a market, Louisiana has been slow to adopt value-based reimbursement (less than 25% of Louisianans can access an ACO per Oliver Wyman, vs. the national average of 70%), but Ochsner has been at the forefront:

- Second of four Medicare ACO shared savings agreements in Louisiana (and the only one centered on a major delivery system — the others are ragtag conglomerates of physicians)

- Capitation with Humana MA generated $267M in premium revenues in 2014

- Shared savings agreements with BCBSLA, United and Aetna (pending for 2015)

At the heart of the OHN appears to be a “clinically integrated network,” (CIN), an FTC-approved model for enabling competing providers to come together around common clinical strategies and shared financial risk. The CIN encourages investment in common clinical IT (which may explain the planned rollout of Epic at Slidell to match Ochsner. Slidell is nested among several Ochsner sites and the collaboration on individual cases is likely to be quite close; elsewhere, Ochsner will likely rely on its preferred HIE vendor Informatica as Lafayette General uses Cerner and CHRISTUS appears to have both Cerner and Meditech). The CIN also allows for joint risk contracting with payers. Ochsner can use the CIN to roll out its shared risk models with the major payers statewide. A critical mass of shared risk economics can also become a powerful engine for change through an alliance by lining up incentives to harmonize on clinical strategy, encourage new cost-effective models and rationalize the overall infrastructure (something Ochsner knows how to do as they demonstrated at River Parishes).

Competitors may take a while to reconcile themselves to the need to play their part in restructuring and will fight for share in the meantime. Ochsner has a the only set of nationally ranked clinical capabilities in Louisiana (per US News and World Report) and will need consistent access to a large volume of patients to maintain them. By locking in value-based arrangements over a larger population base and creating an engine to drive restructuring within the network now, Ochsner should be able to protect itself from some of the economic agony which Louisiana hospitals face.

Arnhem in the bayou?

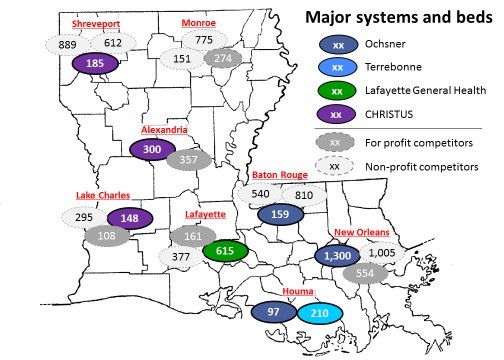

The OHN now covers seven of the eight major markets in Louisiana with the strong positions in New Orleans, Houma and Lafayette . CHRISTUS has presences in three markets (most important Shreveport) but is leader in none of them.

In Lake Charles and Alexandria, this may be fine. In these markets, CHRISTUS is competing with for-profit players (HCA and CHS) and local hospitals operated by the local governments, not major systems — and doing it successfully (achieving zero to positive operating margins and 4-8% net margins).

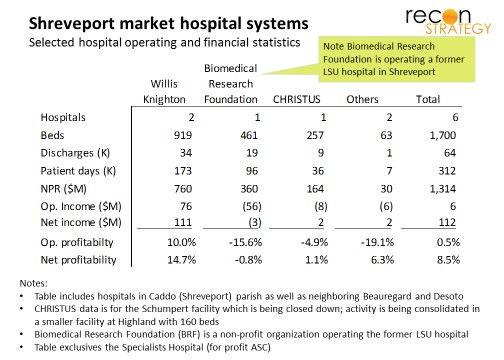

Shreveport is a different story. The Willis-Knighton (WK) system has 65% market share, very strong economics and a fierce competitive reputation. CHRISTUS is a distant #3 in the market. Rumor is that WK bled patients and doctors heavily from CHRISTUS in recent years, forcing them to close down their 256-bed Schumpert Hospital and transition operations to the smaller 160-bed Highland Medical Center. Latest data (before the Highland move) has CHRISTUS with a negative 5% operating margin (vs. 10% positive for WK).

Operation Market Garden famously went a “bridge too far” and, while capturing two major bridges, met with disaster at Arnhem. In Shreveport, will Ochsner find itself similarly combatting hospital-sized tanks with clinic-based PIATs and machine guns?

Too early to say, of course. Easier would have been to avoid Shreveport (hard to see a lot of referrals travelling down I-49 to New Orleans), but Ochsner may not have had a choice. Helping to solve Shreveport was probably part of the “package” for CHRISTUS. (A faith-based strategy might have put Catholic CHRISTUS together with the Catholic Franciscan Missionaries of Our Lady Health System in Baton Rouge and Monroe, but that system is deep in turning around former LSU assets would have nothing left to support a battle vs. WK.)

Ochsner and CHRISTUS have two options now: build on the beachhead organically while WK turns its competitive attention on the ailing Biomedical Research Foundation (BRF) managing the local legacy LSU hospital or team up with BRF and build up a credible defensive lines for a long duopolistic campaign. Intriguingly, Ochsner and CHRISTUS are reported to have met with BRF back in May (with no publicized result). Since then, the BRF, the state government, LSU and WK have become mired in legal disputes (accusations of breach of contract and anti-competitive practices).

Ochsner and CHRISTUS would be smart to focus on standing up the alliance along the coast, quietly completing the transition to the new Highland facilities in Shreveport and letting the legal dust settle before making a decision. However, if BRF can retain control of the LSU assets through the legal fight without too much damage, my guess would be that they will join the OHN before long (albeit on Ochsner clinical terms). Ochsner is moving too quickly to wait for organic plays.

Many ways across the “Rhine”

Either way, the contest in Shreveport won’t stop Ochsner just as the surrender at Arnhem did not stop the Allies (in fact, Arnhem wasn’t liberated until 6 months later shortly before VE day). Warner Thomas has said he wants to take OHN across state-lines. CHRISTUS – which owns a large number of hospitals in Texas including a few just to the west of Louisiana (on a north-south bend from Beaumont/Port Arthur to Texarkana) – could provide the bridges necessary to start advancing towards Houston. From a big picture perspective, Shreveport – however the market shakes out – may not be more than a footnote.