(For background on Pennsylvania market, please take a look at previous note here)

Summary

- The UPMC/Highmark rivalry continues to open new fronts in Pennsylvania

- Highmark’s response to UPMC is differentiated in two ways: first, Highmark is using a coalition building strategy and, second, it is controlling its exposure to big in-patient assets; in contrast, UPMC is building an integrated, single-brand system and happily taking over hospitals (and building more) along the way

- When UPMC and Highmark make major investments in a region, local systems will be caught in the capex arms and feel the pressure to affiliate. Credibly threatening to respond in kind may defuse the arms race. But unaffiliated systems may struggle to find partners willing to bankroll a battle with both Highmark and UPMC, leaving no option for unaligned systems than to pick sides

- Philadelphia systems – so far largely neutral to Highmark vs. UPMC – should be able to stay neutral as the fight develops in their western backyard. If the battle moves into northeastern Pennsylvania or jumps into south Jersey, however, the Philadelphia systems will have to develop a response.

* * *

A month ago, the Penn State trustees agreed to affiliate their Penn State Health (PSH) system with Pittsburgh-based Highmark. With this deal, Highmark has gained a provider footprint in Pennsylvania’s Capital District and an interest in the 540-bed Hershey Medical Center (the #4 ranked hospital per USN&WR in Pennsylvania). The affiliation is a predictable outcome of competitive moves in the region and tells us a lot about how Highmark is responding to UPMC’s push east. It also brings the epic Highmark/UPMC competitive struggle much closer to Philadelphia. How long can the big Philadelphia systems stay out of the fight? Let’s take a closer look.

Why did the Penn State/Highmark affiliation happen?

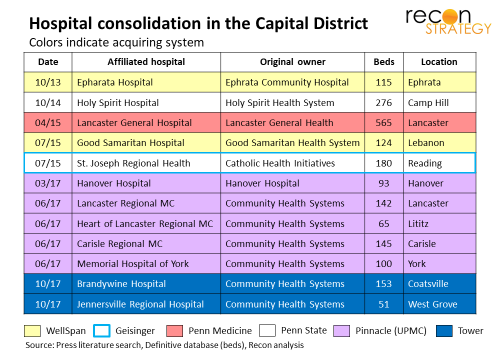

Last year, hospital consolidation sharply accelerated in the Capital District, driven, in particular, by the partition of six Community Health Systems (CYH) hospitals:

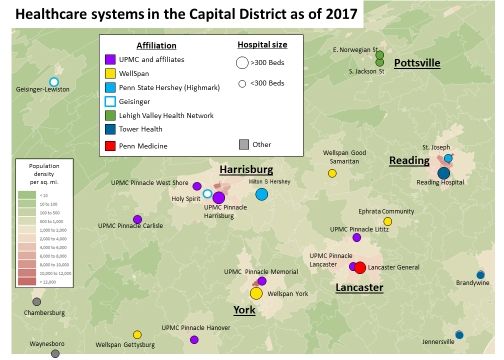

The Capital District is now served by a handful of systems with strong vertical orientations (employed physicians and clinics <-> secondary hospitals <-> tertiary hospitals). And, while two consolidators were local systems (WellSpan, Tower) and two others are really just beachhead builders (Geisinger, Penn Medicine), UPMC’s entry via Pinnacle is very consequential: first, UPMC has the academic wherewithal to make Pinnacle’s Harrisburg flagship a credible threat to Hershey and, second, UPMC can use its health plan subsidiary as a competitive lever.

Penn State had long recognized the precariousness of being a stand-alone academic center. It tried merging with Geisinger back in the nineties. In 2016, it tried to combine with Pinnacle (dropping the effort in the face of regulatory push-back). It did affiliate with the much smaller St. Joseph in Reading in 2015 and acquired a major independent physician practice in Lancaster in 2017 (shortly after Penn Medicine made its appearance). But neither move is adequate to the radically changed referral landscape.

Suddenly surrounded by UPMC, Penn State agreed to help from Highmark.

Highmark expands its coalition approach to responding to UPMC

The Capital District is just one, newly-opened, front in the competitive struggle between Highmark and UPMC. Western Pennsylvania has been the primary theater ever since Highmark purchased West Penn Allegheny system and transformed it in the Allegheny Health Network (AHN). More recently, Highmark formed a joint venture with Geisinger to build ambulatory capabilities in north central Pennsylvania in part as a counter of UPMC’s takeover of Susquehanna.

Key terms of the affiliation with PSH are:

- Highmark would appoint 3 of the 15 directors on the PSH Board

- Highmark will invest only in PSH as its provider partner in the region while PSH would not own any health insurance companies; on the other hand, both PSH and Highmark can contract with other insurers and providers respectively

- Penn State Health would invest over $1B to grow in the region and Highmark is described as being expected to support specific community projects within this initiative

A few implications of this arrangement:

- Highmark appears taking a “coalition” approach to respond to UPMC’s eastward sweep. Highmark itself (not its AHN provider subsidiary) was the partner in both the Geisinger joint venture and the PSH affiliation. In contrast, with UPMC’s full control/rebranding model for Susquehanna and Pinnacle, Highmark’s approach allows the provider partner to retain significant autonomy and keeps the partners’ branding in the forefront. Highmark cannot be as directive as UPMC, but also, thereby, may attract stronger allies to its camp.

- Highmark is choosing an ambulatory-focused response to UPMC: Under the PSH terms, Highmark can selectively invest in the $1B expansion with a particular focus on community care. It could be that the ownership model for individual investment projects may vary from the overall affiliation. Also, the focus on ambulatory care is consistent with the joint venture deal Highmark struck with Geisinger last year. Highmark appears to be carefully minimizing its exposure to big inpatient centers just as UPMC is doubling down on inpatient.

- The promise of $1B in building out new care capability is a lot of potential negotiating leverage pointed at somebody. Who is the target? UPMC isn’t going to back down and Tower sits on the periphery. My bet is that the $1B promise is designed to encourage the one big non-aligned system, WellSpan, to consider collaborating – and thereby direct that $1B towards to attracting Pinnacle rather than WellSpan patients.

Can WellSpan stay neutral?

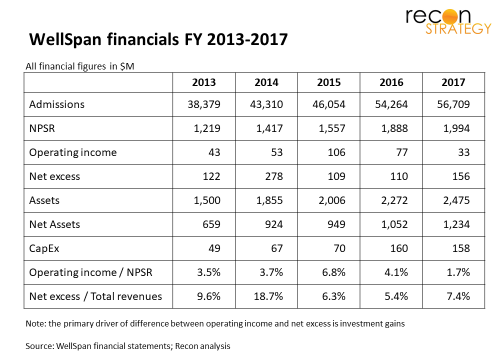

WellSpan is a $2B health system with nicely positioned hospitals: the largest hospital in York and others are distributed in the region without any co-located competition (Ephrata, Lebanon, Gettysburg). It has also been able to maintain a strengthening set of financials (note in particular the improvement in net asset position):

To add strategic robustness, it has pursued several partnerships to gain capabilities without compromising independence. Two prime examples:

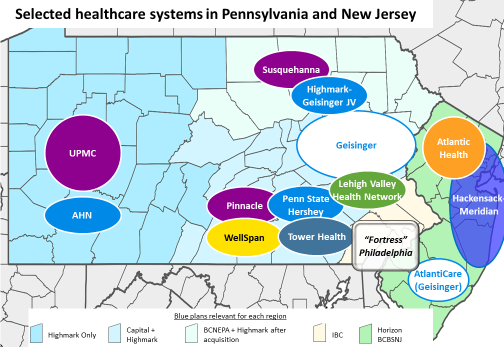

- Founding member of AllSpire, a 2013 alliance for finding operating efficiencies (e.g., procurement) and sharing clinical best practice. The current partners are three Pennsylvania systems (WellSpan, Tower, and Lehigh Valley Health Network) and two New Jersey systems (Hackensack-Meridian, and Atlantic Health System). See PA/NJ map above. Notably, AllSpire members “surround” Philadelphia but studiously avoided any Philadelphia participation (Lancaster General was originally a member of AllSpire but appears to have dropped out once it affiliated with Penn Med).

- Clinical collaboration with Johns Hopkins Kimmel Cancer Center launched in 2016 to access clinical trials and second opinion services for complex cases. The collaboration is similar to the one AHN has with Johns Hopkins (and has been recently expanding with a new Institute and satellite cites.

However, these resources can’t match either Highmark or UPMC. To some degree, they are being stretched already: WellSpan has launched a major investment program for its size ($150M a year over five years starting in 2016) to put Epic in place, expand the York hospital ED and build a health Pavilion at Ephrata. These investment levels have attracted the notice of bond rating agencies (though they have kept the rating at Aa3 and stable given the strong market position and historically reliable finances) and may, therefore, be approaching the upper bound of the possible.

Both the AllSpire partnership and the capex commitments were put in place before WellSpan’s competitive market was turned upside-down by UPMC and Highmark. Capital Blue Cross (the local Blue plan in the region which competes with Highmark that also operates in the same territory) would likely want to do all it can to preserve WellSpan’s independence (indeed, a vertical combination between WellSpan and Capital Blue Cross would be interesting but may aggravate WellSpan’s situation by setting itself up in competition with both Highmark and UPMC on the plan side of the business without really addressing its care delivery vulnerabilities). But Capital Blue Cross’s help may not be enough once Highmark and UPMC start blanketing the market with advertising, buildings and compelling narrow network deals centering on their respective provider systems.

Our guess is that WellSpan won’t want to stand alone for too much longer. Once it decides to make a deal, I see two obvious options (though there may be others but it is hard to imagine a collaboration with a Philadelphia system given that WellSpan studiously avoided Philadelphia entanglements in the AllSpire membership strategy and going to Johns Hopkins for cancer):

- Transform AllSpire into a more substantial affiliation and secure credible access to enough capital go “toe-to-toe” with Highmark and UPMC. This would diminish the return to a capex “arms races” for everyone and perhaps leading everyone to adopt a less capital intensive approach. This option hardly seems feasible given the need to bring 3 to 5 partners together on major incremental capital commitments when only one is facing UPMC and Highmark (so far…)

- Come to terms with Highmark/PSH (perhaps while still retaining some independence – keep in mind Highmark’s coalition approach) to ensure that the looming $1B is spent providing new access options to Pinnacle territory.

Either way – a WellSpan-Highmark deal or a formation of a new mega-system out of WellSpan, Tower, and Lehigh Valley with perhaps New Jersey’s Hackensack Meridian in the background – Philadelphia providers are going to face a much stronger set of competitors in their western backyard.

Will “Fortress Philadelphia” start feeling the pinch?

Imagine a scenario where WellSpan starts toying with a Highmark alignment and Tower begins turning their current health plan joint venture with UPMC into a broader affiliation. How long can the Philadelphia systems remain agnostic to the structure of the delivery systems to their west?

My guess is quite a while actually. Philadelphia is a major market in its own right, much larger than potential referral volume from the Capital District. And, the west seems to play a fairly small role in referrals to Philadelphia care volume. Take a look at the map below which shows patient county of origin data for cardiac patients at Penn Medicine’s flagship hospital (relativized as raw Medicare FFS $ claim over total population):

The Philadelphia systems get more referrals from northeastern Pennsylvania and south Jersey than they do from their western backyard. As long as the southern Jersey “route to the sea” remains open, the systems inside “Fortress Philadelphia” have a supply line for referral patient volume.

I see three major scenarios which would make the Philadelphia systems get anxious about the periphery:

- One of the big New Jersey systems such as Hackensack-Meridian and RWJ-Barnabas turns its attention to southern Jersey

- One of the bigger northeastern Pennsylvania systems decides to make a play for southern New Jersey (modeled on Geisinger’s affiliation with AtlantiCare)

- The UPMC/Highmark rivalry shifts further east into northeastern Pennsylvania, leading to a reshaping of that market and threatening referral flow south into Philadelphia.

Notably, none of these relate directly to what is happening in the Capital District.

In my view, the biggest impact of the Capital District events for Philadelphia systems will be a sense of urgency that the speed with which a market restructuring can happen should inspire. All that change in a little over a year is remarkable. The Philadelphia systems may not want to wait for the signposts that one of those three “nightmare” scenarios is coming to fruition. By the time they recognize the signposts and get themselves geared up to respond, the market may already have shifted under their feet. Better to be proactive and lock in those referrals by more formal affiliations now. We’ve seen a first move by the Thomas Jefferson system in Philadelphia and Kennedy Health (in New Jersey) just recently. There will certainly be more deals like that!