United’s OptumCare promises a lot of value for health plans. An integrated system supported by Optum technology should be able to deliver consistent, analytically sophisticated care. Its ambulatory-focused configuration (clinics plus urgent care plus ambulatory surgical centers or ASCs) should keep patients out of high-cost settings through mutually reinforcing referral loops (where it has density[1]).

One obvious question is whether United can use OptumCare to materially advantage its own health plans. Is a new, nationally-scaled Kaiser in the offing?

If that is its endgame, United has a lot of work to do — at least as far as Medicare Advantage (MA) is concerned (our analysis did not look at United’s other health plan lives so the picture may look different there). While there is some overlap between the two businesses, it is limited in scope and targeted to specific geographies.

We compared the overlap of OptumCare sites[2] and United’s MA lives several ways:

- We estimated the distribution of MA lives in regions (1) without any OptumCare at all, (2) with a thin (below average density) OptumCare network and (3) with denser OptumCare networks (density is a prerequisite for a closed configuration like Kaiser)

- We compared the degree to which MA market share was correlated with the density of OptumCare sites in the same region

- We looked at both United’s overall MA lives (any product) and those just in HMO/POS products which offer the greatest opportunity for constructing a Kaiser platform (the other primary products – local/regional PPO — do not use a primary care to manage referrals across a tight network).

- We analyzed the data at both an MSA and county level; we also looked at all MSAs and counties where United has a presence and at the same data for just the top 75 MSAs measured in terms of population (and which we think are good proxies for Optum’s announced plan to build positions in the “top 75 markets”).

Let’s see what we found. [Please see methodological notes at the end.]

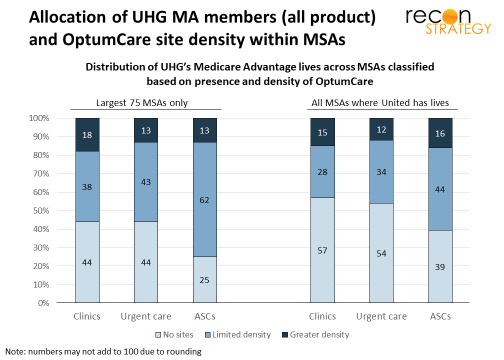

MSA lens

Most MA members have limited access to OptumCare sites. They either live in MSAs with no OptumCare at all — 57% are in MSAs with no OptumCare clinics, 54% in MSAs with no urgent care centers — or just a relatively thin network of sites — a plurality of 44% of members are in MSAs with a thin network of ASCs (see right side of exhibit below). This picture is no different whether looking at all MSAs or just at the top 75 MSAs (see left side of exhibit). Only a small minority live in MSAs with robust networks of OptumCare sites though in no case does this exceed 18 of all members.

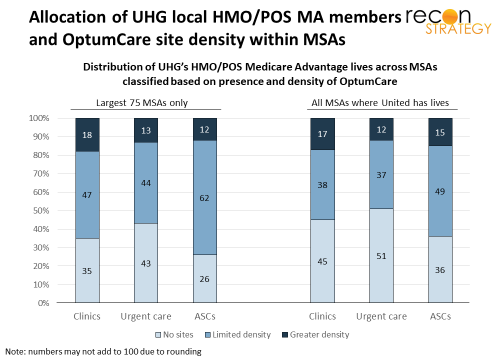

However, the picture is slightly more advantageous if we just look at United’s members in HMO/POS products (which represent 70-80% of their total Medicare Advantage lives within MSAs). Generally, a larger share of members are in MSAs with a limited network of sites which may serve as beachheads for further growth. Still, however, only a small minority (<=18% of members) are in MSAs with denser networks.

A correlation analysis confirms that the overlap between United market share and OptumCare site density is limited. In the top 75 MSAs, the correlation with United’s MA market share was 15% for clinic density, 4% for urgent care center density and 22% for ASC density: somewhat positive but still a long way from a Kaiser-enabling platform.

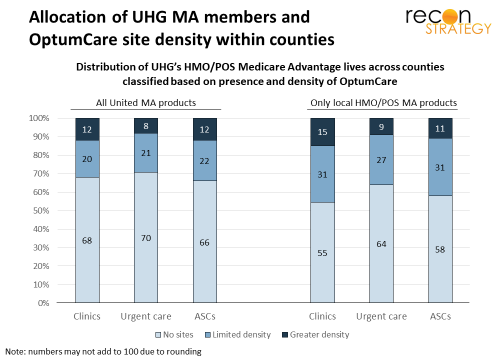

County lens

Counties – which are smaller geographic entities than MSAs – may represent a more reasonable definition of the geographic market for the kinds of ambulatory care that OptumCare offers. An MSA lens might implicitly assume that MA lives concentrated in one county will travel to another county in the same MSA to be seen at OptumCare sites. If we just look at overlap of lives and sites on a country level, we would avoid these kinds of issues.

Not surprisingly, the county lens significantly increases the share of lives in a geography with no OptumCare sites and reduces the number of lives in regions with denser OptumCare networks to between 8-15%. Also, at the county level, United’s MA market share and site density in each county are essentially uncorrelated (3% for clinics, -5% for urgent care centers and 2% for ASCs.)

Exceptions

While the overall view is of limited overlap, there are specific geographic exceptions: Seattle-Tacoma, Las Vegas, Indianapolis, Hartford, Colorado Springs, Cape Coral, and Corpus Christi are all sizeable markets where United has more than 25% share of MA lives and OptumCare has its denser networks of ambulatory care delivery (though even in these markets, the density is not consistent across the three types of ambulatory care Optum provides). OptumCare’s strength in several markets – Seattle-Tacoma, Las Vegas, and Colorado Springs — does depend on the DaVita acquisition closing (indeed, legacy OptumCare has no presence in the Seattle area at all).

The overlapping density in these markets might support some targeted experimentation. Note, too, that Kaiser has a very strong position in Colorado Springs and is making a big push into the Seattle-Tacoma area after its takeover of Group Health. So United may find itself pushed into using its OptumCare network in these regions defensively as part of a closed model product.

Implications

Overall, there is only a small overlap between United MA membership and its current OptumCare network. This is not surprising given that OptumCare has been, to date, assembled via fairly large-bite acquisitions which were themselves assembled on the basis of an all-payer strategy.

Accordingly, OptumCare’s public positioning that it wants to be a provider partner for any payer (not especially favoring United) appears credible (as least as far as MA goes). United does not have the market share to support OptumCare’s business and OptumCare lacks the network to meet United member ambulatory needs (again MA view only).

The overlap between United and OptumCare will inevitably increase though this will likely take years. Longer-term, United will have the strategic option to offer vertically integrated closed system products in many markets should that be needed (e.g. if the rumored Wal-Mart/Humana combination is followed by a massive expansion of clinic capability inside Wal-Mart stores). And we might expect some defensive experimentation pretty soon in selected markets where there is a vibrant Kaiser.

However, Optum’s real focus in the near term will be growing its network and this will require collaborative relationships with incumbent health plans. Health plans can breathe easy for now. Providers, on the other hand, should be paying close attention. OptumCare is coming for your joints!

Methodological notes

United’s Medicare Advantage share was derived from the most recently available data for 2018 from CMS. OptumCare network data was constructed by Recon Strategy from publicly available sources. Note that we measure the network in terms of sites or addresses. A Density was measured as sites per capita for the entire population in a particular region. We evaluated the median level of density for OptumCare across all regions (whether MSAs or counties). Regions were evaluated as having a thin network if the density was less than or equal to the median level of density OptumCare has achieved across all its markets. Regions were evaluated as having a dense network if the density was greater than the median national level. Note that the median level of density was defined for all MSAs and all counties and this metric was applied to classify the top 75 MSAs.

[1] Key is to have all three types of care available in sufficient density in a particular geography. While the geographic distribution of OptumCare is broad (we estimate about 70-75% of the country lives in an MSA with OptumCare presence of some sort), only about 14% of its potential patient population live in MSAs with all three types of care present. Accordingly, Optum has not been shy about still having a lot of network build out to do in their existing markets (in addition to building positions in the other 40 prioritized markets where OptumCare says it is not present).

[2] We have included sites from the DaVita acquisition although that is still pending regulatory approval. We did not include OptumCare sites that are associated with the House Calls business which sends clinicians to patient homes to review and validate diagnoses and provide counseling. This business is tied significantly with supporting Medicare Advantage risk adjustment rather than ongoing care delivery.