Summary

- NaviHealth is a leader in post-acute care management; since it manages but does not provide care, its impact is constrained by quality of available providers

- By aligning with Optum clinical and technology assets, naviHealth can raise the capabilities of post-acute providers, direct more cases to be discharged directly to the home and speed up the return home for others

- Given inpatient stays often mark the start of sustained needs for help in the home, a post-acute navigator like naviHealth could be well-positioned to orchestrate longer-term “aging-in-place” support

Overview of naviHealth

NaviHealth manages post-acute care (PAC) mostly for health plans. It develops personalized care plans for each patient before discharge, and then uses a field force of care coordinators to ensure the plan is followed and no patient gets “stuck” in any one setting or stage. NaviHealth built its leadership in PAC management arose from two key advantages:

Analytics. NaviHealth’s “LifeSafe” analytics first emerged at an analytically inclined (but now defunct) physical therapy chain, then incubated over a decade with Kaiser (under the SeniorMetrix brand). When naviHealth purchased SeniorMetrix in 2012, the data set had 700K patient histories – and has been growing ever since. The larger the underlying data set, the greater the precision in the personalization of PAC plans.

Local operational scale. Being big in a region allows for better use of the field force, stronger relationships with hospitals (both electronically via links into the EMR and with key personnel such as case managers, discharge planners), and – as a “utility” – the opportunity to sell supporting services (such as referral management software). Most important, local density allows for enough data to reliably assess local post-acute provider performance and referral volume to command attention of the top performers.

From a twinkle in Tom Scully’s eye back in 2011, naviHealth has grown to (reportedly) over a billion in value. MA plans have handed over 4.5M lives to it to manage in various guises (one can buy just the LifeSafe package, the SNF package, for example, or the full post-acute suite) including the big ones – UNH and HUM – plus a selection of major regional Blues.

Medium-term synergies with Optum

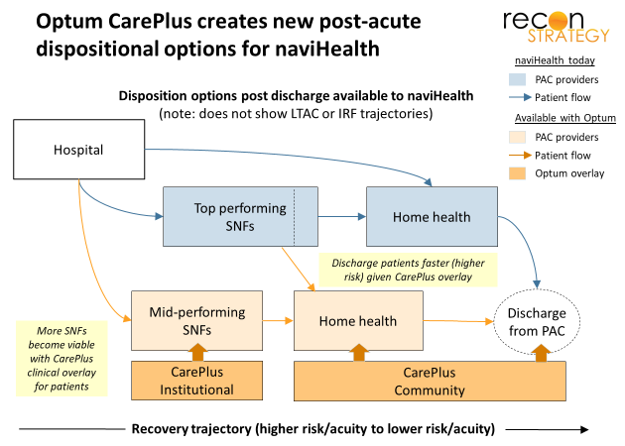

UNH is doing more than just buying a favorite vendor[1]. There are strategic synergies in play. Ultimately, there are limits to what naviHealth can achieve in reducing post-acute care costs and improving outcomes. NaviHealth manages PAC delivery but does not actually deliver the care. Thus, the outcomes it can achieve in any one market are constrained by the quality of post-acute providers available.

Optum’s CarePlus can relax that constraint and open up a new layer of potential value. CarePlus has APNs trained in complex populations who provide onsite care in nursing facilities (“CarePlus Institutional”) and homes (“CarePlus Community”)[2]. Optum’s House Calls capability could play an important role as well. A clinical overlay in skilled nursing facilities (SNFs) and the home for the more complex patients could expand the number of adequately performing SNFs in any one market and make the home a safe setting for riskier patients, enabling more direct discharges to the home and earlier return for those starting their post-acute episode at SNFs.

NaviHealth competitors without the same capabilities will struggle to stay at par because they will not have the same levers to improve upon the performance of local providers.

The Optum acquisition should also help NaviHealth go after the provider bundles opportunity. Effective PAC is a key success factor in episode bundles. Yet, as of 2018 (latest data from CMS), naviHealth had only a limited role as a convener in the Medicare BPCI. Remedy Partners – with ~50% share – is the leader. What naviHealth lacks more greater penetration — strong marketing inroads with providers and of the capabilities to manage the business side of bundles — it can get from Optum. Notably, Remedy added care delivery capabilities last year when it merged with Signify Health. Signify’s clinician field force provides health risk assessments, gap closure and starting to provide longitudinal care at home and in facilities. This potential leapfrog advantage vs. legacy naviHealth is now also neutralized by the combination with Optum (via Careplus).

Building blocks for a leadership position in the @home revolution?

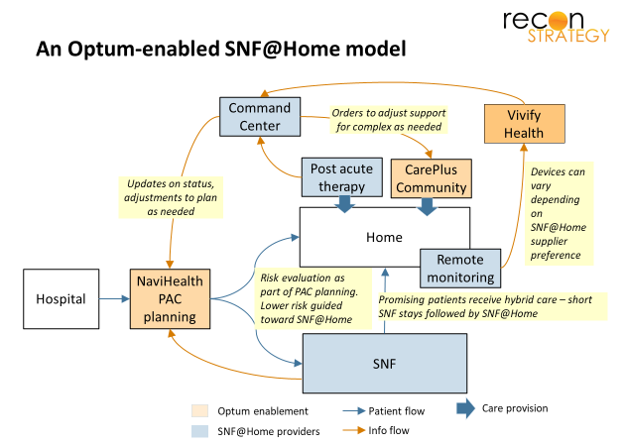

Optum’s clinical overlay is one major synergy opportunity for naviHealth. The other I see relates to technology enablement. Last year, Optum purchased Vivify Health, a remote monitoring and patient engagement platform which payer/providers in particular (UPMC, Geisinger) have been using to prevent readmissions. Because Vivify is device and protocol agnostic, it can support a variety of different providers and strategies for managing care at home.

There have been rumblings for a while about a SNF@Home alternative (analogous to the Hospital@Home), something a well-positioned PAC manager could help orchestrate. By adding in Vivify technology and the CarePlus clinical overlay, Optum would have the capabilities to assemble and support such a model in collaboration with local acute and post-acute providers — enabling more discharges to be directed to the home or hybrid stays (brief SNF stay followed by SNF@Home). This kind of capability will further enhance naviHealth’s competitiveness in PAC management (not to mention opening additional revenue streams for Optum).

Longer term, there is even greater potential beyond PAC. Major declines in health status and ability to live independently often start with the discharge from an inpatient episode. PAC managers are thus in a great position to not only define the trajectory of care over the 30, 60, 90 days post discharge; they also have the first opportunity to identify what support needs patients will have beyond the episode and the patient/caregiver relationship to help navigate to the highest value vendors and protocols (at least soem of which could be ongoing customers for a Vivify solution).

Of course, UNH will need more than just naviHealth and Vivify to drive @home and a lot needs to be developed in terms of analytics, regulation and business model. But, as UNH well knows from its successful plan and technology businesses, the ultimate winners in revolutions tend to be the orchestrators (naviHealth) and the enablers (CarePlus, Vivify and any other companies Optum picks up off of the shopping list naviHealth experience suggests).

With these two acquisitions, Optum has taken important steps to assure its ultimate leadership.

Viva la Revolucion!

[1] Optum does have its own Post-Acute Transitions program. Given that UHC uses naviHealth, I assume this program is not competitive so would end up being folded in (adding to local density)

[2] This model has been around a while (Institutional is legacy Evercare iSNP and Community is repackaged capabilities from INSPIRIS). It has been evaluated very positively in peer reviewed studies – most recently in McGarry et al “Managed Care for Long-Stay Nursing Home Residents: An Evaluation of ISNPs”, AJMC, September 2019 – and earned a call out in a 2017 MedPac report chapter in 2017.