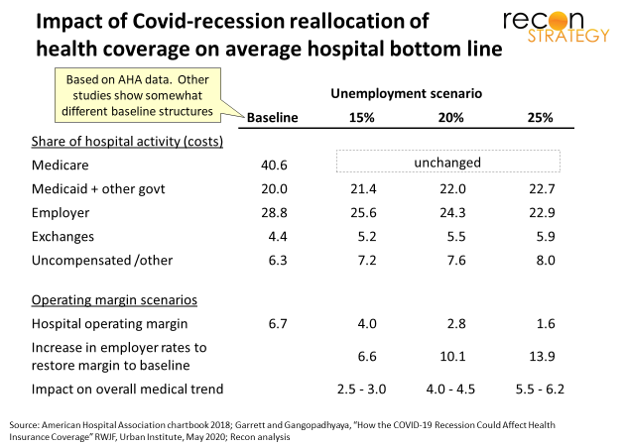

Among Covid’s many repercussions, the recession shock will drive a sustained degradation of provider payer mix. I estimate that each 5% added to unemployment will incrementally reduce hospital[1] operating margin by 1.0-1.5% and hospitals would need to charge 3-4% more on commercial care to maintain margins[2]. Given that hospital costs make up 40-45% of commercial total cost of care and we are facing unemployment scenarios of 15-20% (per Robert Wood Johnson – see table and source notes), we could ultimately expect this hospital rate pressure – if not averted or moderated – to contribute a 3.0-4.5% “tailwind” to commercial medical cost trend.

Why is this? Studies consistently show that Medicaid and Medicare do not fully reimburse hospitals for the cost of care they incur. The American Hospital Association (AHA) estimates that Medicare and Medicaid pay between 87-88 cents on every $1 of care costs[3]. Even after healthcare reform, hospitals deliver a lot of uncompensated care. By paying $1.45 for every $1 in generated hospital costs[4], commercial plans cover the deficits and leave hospitals with positive margins (averaging 6.7% in 2016 per latest from AHA). Now, with the Covid/lock-down induced recession shock, the unemployed are shifting out of commercial coverage and onto the exchanges (which typically pay providers less than employer coverage), Medicaid or going uninsured altogether. Delicately calibrated webs of cross-subsidization will be torn to shreds.

Despite CMS flooding the zone with one-off payments now, neither federal nor state finances will support permanent outsized increases in rates for government programs (likely the reverse if state Medicaid agencies repeat strategies from the 2008 economic crisis). So, hospitals can only practically ask their health plan customers about raising rates on the now smaller base to make up the difference.

Will they succeed in the negotiation? Even in 2016, when hospitals averaged 6.7% operating margins, ~30% of the industry saw losses. Accordingly, we have seen hospitals closing for a while mostly in rural areas. Add to this choked off elective care and Covid-retooling costs, and you have brewed some potent financial poison. We can expect rural exits to accelerate and some urban systems to start exiting as well. Every exit adds negotiating leverage to the surviving systems.

Yet plans cannot simply roll over. The Covid recession is expected to be brutal. Employers will rebel against large rate increases with coverage buy-downs, rebidding the business, shifting to self-insured to support custom solutioning, or cutting out health plans altogether by directly contracting with providers. Group risk – a traditional mainstay of plan profitability – could become a much more difficult business.

Thus Covid’s backhand blow: after a brief period of unprecedented collaboration in the crisis (telehealth reimbursement terms, regulatory relaxation, utilization management relaxation, extra payments under various guises), plans and providers could soon be locked back in their traditional roles and consumed in bitter rate feuds…that is, unless plans and providers take steps now to prep some more creative strategies for how to manage the deficit.

[1] I focus on hospitals here (inpatient and outpatient) but same logic applies to professional costs so the effect could be broader though physician practices will have lower overhead cost burden.

[2]All calculations done for the national average. Get in touch if you want to see the calculation details.

[3] AHA chartbook from 2018, chart 4.6. AHA consolidates DSH payments into Medicare and Medicaid resulting in rough net equivalents. Actual Medicaid rates are estimated to be well below Medicare.

[4] Per AHA (2016 data). More recent studies have suggested much higher rates relative to Medicare and some reconciliation between the AHA perspective and what these studies are showing would be helpful but is not undertaken here. We assume AHA has the data right for this high-level analysis.