OptumCare’s acquisitions usually make headlines. But what happens when the reporters leave? How is clinical capacity managed? What role do micro-acquisitions, recruiting and retirements play in advancing OptumCare capabilities? This is important because OptumCare is a risk-taking engine. Perhaps by understanding post-acquisition moves, we can reverse engineer United’s view on how clinician capacity and specialty mix can maximize value.

We looked at two mature OptumCare geographies, Nevada and Texas with large physician presence and healthy United Medicare Advantage market share (just below 50%). Our analysis primarily uses the Medicare Physician Compare database. The Physician Compare database is a great resource for quantifying provider structures though it does have some limitations: reliance on self-reporting for some provider characteristics and periodic updating means it may not be consistently up to date[1]. We primarily examine changes over time, so these weaknesses should not affect our core conclusions. We also relied heavily on the published WellMed network database. This data source is also limited by its “user-friendliness,” but still helped us understand the partnership strategy in Texas.

Optum Nevada: building out employed specialists

In 2007, United acquired SouthWest Medical, one of the largest group practices in the state, based in Las Vegas. Around 2012 OptumCare also acquired Urology Specialists of Nevada (USONV), which at the time was just beginning to strengthen its Oncologist capacity. Since 2016, OptumCare has continued to strengthen their specialist presence and has strengthened the OptumCare branding of USONV. We observed:

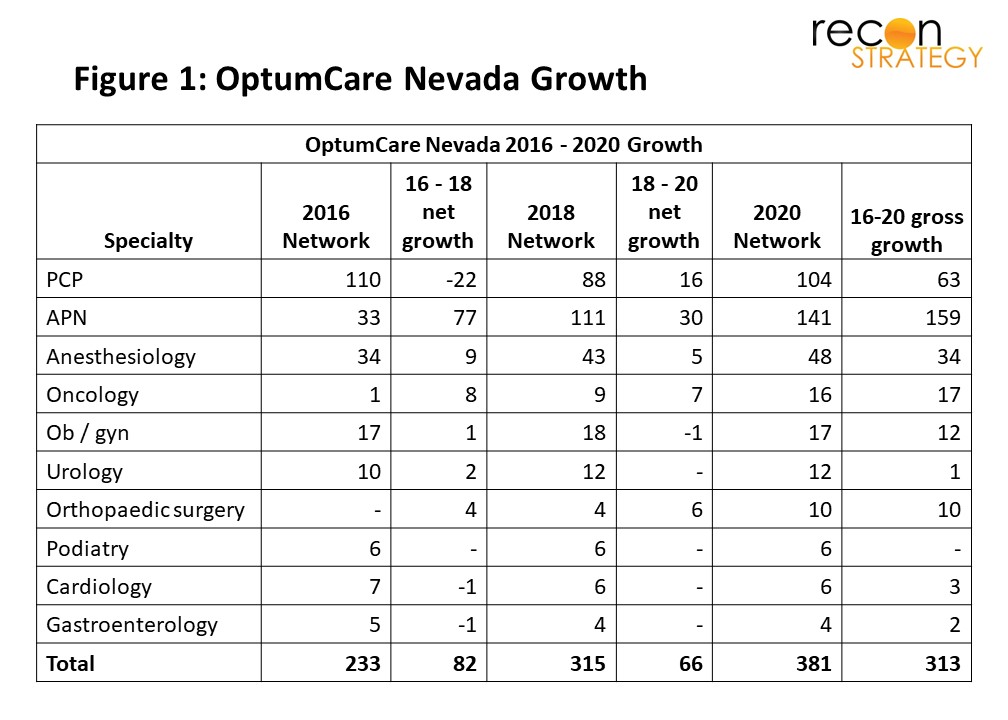

- Massive growth in overall clinician capacity (63% over the four years)

- Significant shift towards APN staffing in the delivery of care (though the full extent of this shift is difficult to quantify[2])

- Added just overt 40 specialists (including 14 anesthesiologists but also oncology and orthopedic surgery) to staff the OptumCare ambulatory clinics (Figure 1), a doubling of employed specialty care.

Actual hiring was even more extensive because of large turnover: overall, 313 providers joined the network and 170 left (60% turnover of 2016 clinicians).[3] Growth was driven primarily by recruiting individual providers rather than practice buyouts. Individual recruiting at that kind of rate would allow Optum to completely reshape the talent and working culture of the practice. Optum has retained consistent leadership, however: Robert McBeath has been CEO of SouthWest Medical since 2013 when his urology practice was acquired by the group.

The growth of specialty care is clearly deliberate and Optum is investing in the technical infrastructure for its specialists. For example, it grew its complement of oncologists from 1 to 16 and recently opened a 55,000 sq. ft OptumCare Cancer center in the heart of Las Vegas, which will also support a clinical research enterprise.

Optum Texas: shedding specialties and partnering outside the practice

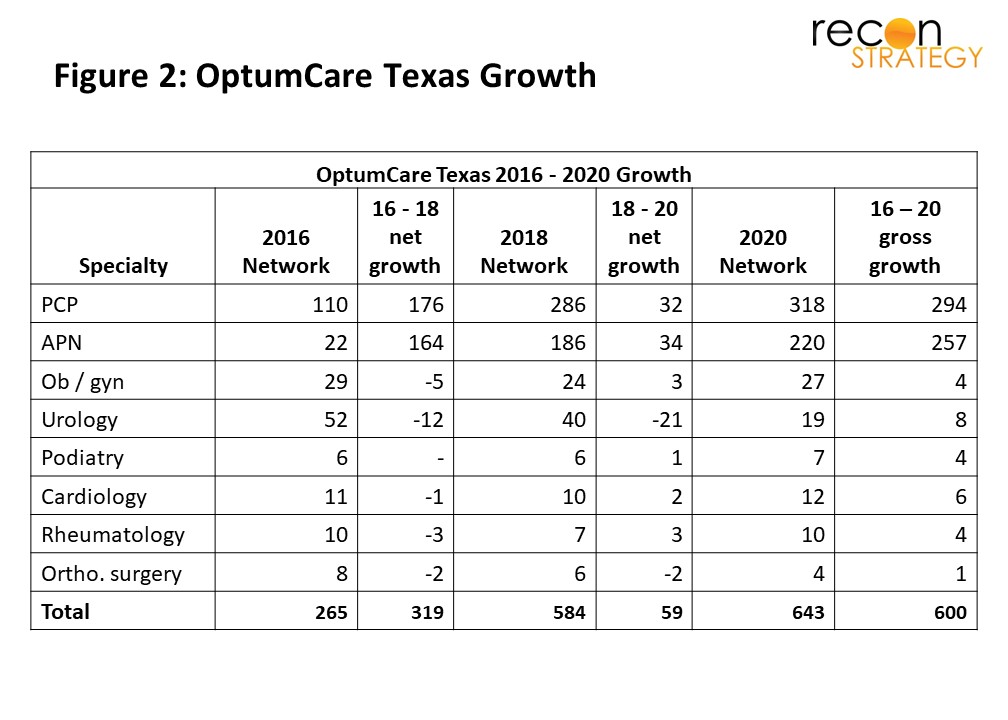

WellMed has been the centerpiece of Optum’s Texas network since it was acquired in 2011. Between 2016 and 2020 Optum’s employed physician network saw 140% growth (Figure 2) concentrated in Bexar County and Tarrant County. This growth was driven both by individual PCP recruitment, and the acquisition of USMD Health, a primary care focused group about 200 providers.[4]

Like Nevada, we see rapid growth in APN capacity, adding almost 200 of them between 2016 and 2020. However, in contrast to SouthWest Medical, WellMed has not only not grown its specialist complement in line with the more than doubling of its primary care capacity; it has, in fact shed specialists attached to practices it acquired (particularly urologists) and has not hired replacements.

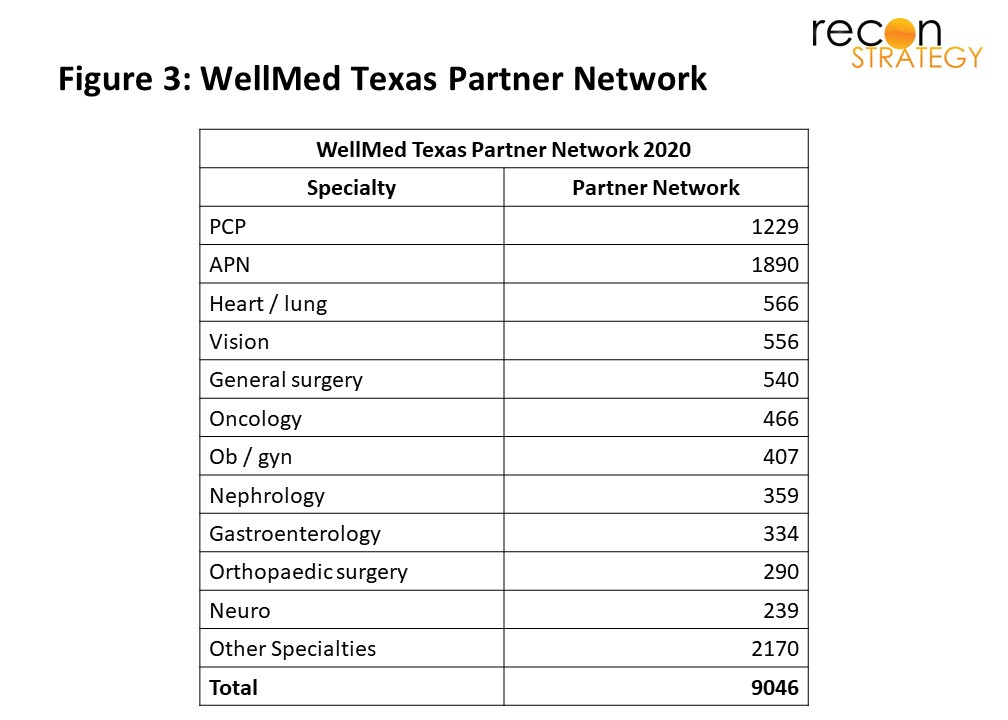

Where do WellMed patients go for specialty care? WellMed appears to rely on its partner network. Partner network physicians are described as trained in the WellMed preventative model of care and supported by its proprietary technology. The 9,000 providers in WellMed’s partner network cut across all the medical specialities (Figure 3). Unlike in Nevada, the WellMed online database includes these partner physicians together with its employed physicians, and the group advertises that they contract for risk-based payment models.

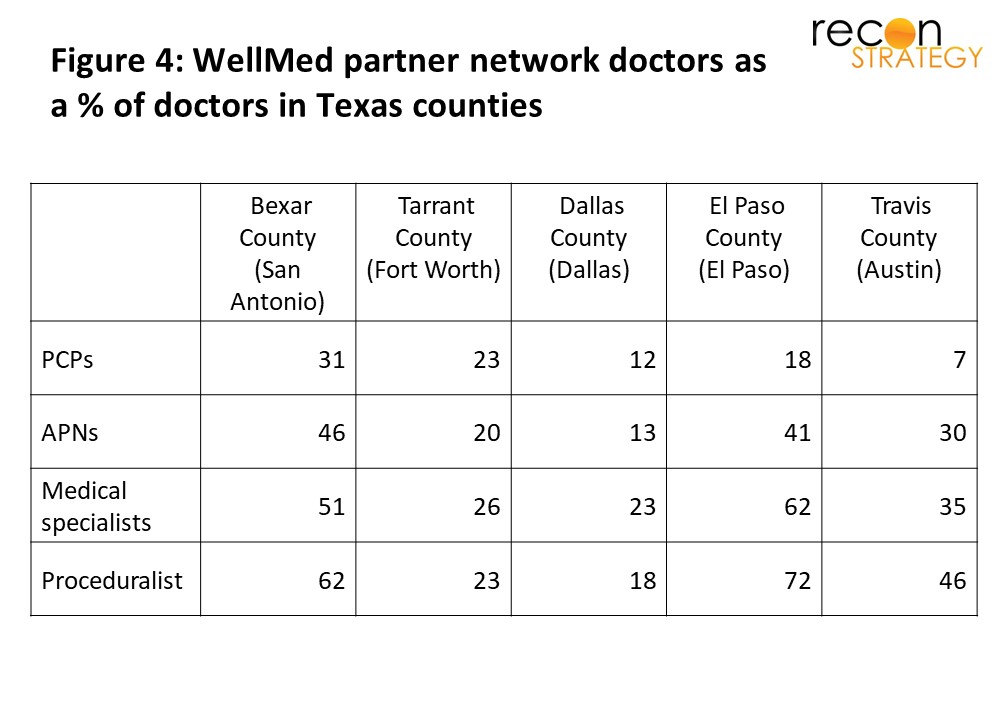

Optum’s partner network expands well beyond Bexar and Tarrant counties, where its owned network is concentrated. Our analysis showed that Optum also contracts with a substantial proportion of physicians in Dallas, El Paso and Austin[5]. The WellMed network seems to be somewhat selective (Figure 4), showing that OptumCare is being intentional about who it partners with to provide care.

How Nevada and Texas are the same, how they’re different

Given the UNH Medicare Advantage market share in both regions, we can assume OptumCare is working to improve its ability to take risk. In California the organization has introduced an integrated product it’s calling Harmony, and Andrew Witty (Optum’s CEO) has announced plans to expand this offering to Texas and Seattle, and then more broadly. In both geographies we see an increase in employed APNs, also a likely helpful move to be able to take risk and still make a profit.

We see consistent shift towards APNs in both markets which suggests OptumCare broadly sees value in top of license practice and allowing physicians to focus on more complicated conditions and patients while preserving access for routine care.

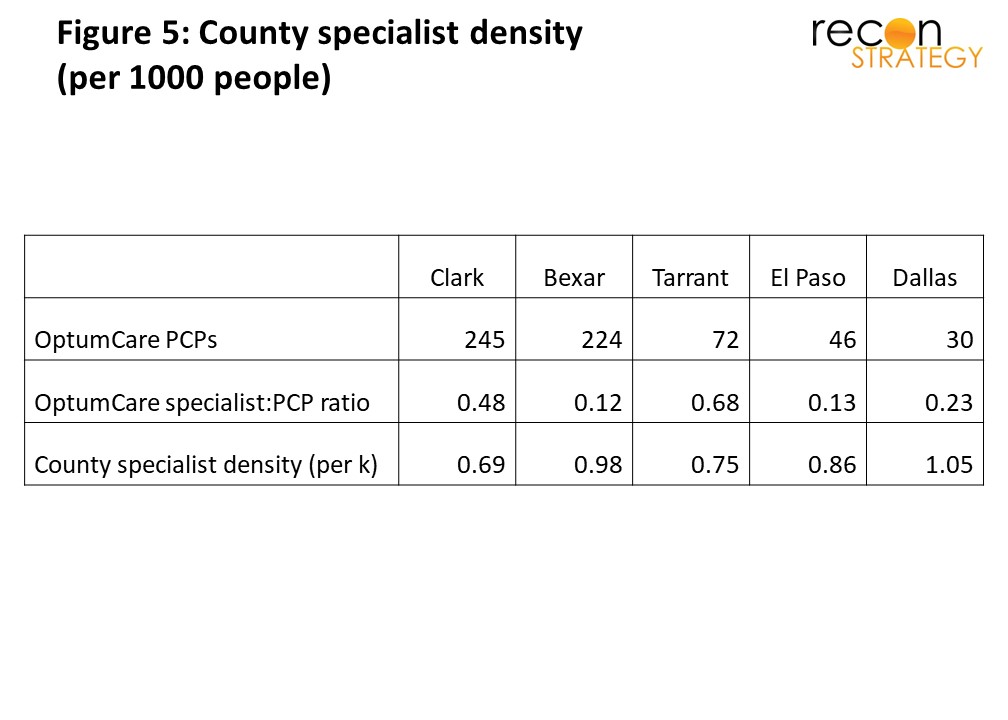

But how do we explain the stark difference in specialist strategy? Notably, in Clark (Nevada) and Tarrant (Texas), OptumCare has between 0.5 and 0.7 specialists for every primary care clinician, while in the remaining Texas counties, the ratio is closer to 0.10 to 0.25 specialists per primary care clinician.

Our hypothesis is that the difference is driven by difference in specialist capacity constraints. We analysed the broader physician landscape in both places. While both Texas and Nevada overall lack appropriate physician density, the Las Vegas area (Clark County) and Forth Worth area (Tarrant) has a lower specialist presence per capita (0.70 to 0.75 specialists per K inhabitants) than San Antonio (Bexar County), Dallas or El Paso (0.86 to 1.05 specialists per K inhabitants).

How would this difference in specialist capacity encourage the two different strategies we see? In counties with a lack of specialists, access to specialists will be constrained and they will have plenty of leverage. By employing more specialists, OptumCare can protect specialist access for its patients, have more control to guide care towards high value pathways and potentially get more leverage over hospitals. In markets where there are more specialists, however, primary care referral relationships will be more potent and OptumCare may be able to create in its preferred network, the kind of access and influence over treatment pathways that deliver the value it is looking for.

As United and Optum grow their combined presence across the country, we can expect them to build out their ability to deliver fully integrated products; however, OptumCare will have to pick and choose where to build out networks through owned physicians, and where to rely on the existing physician landscape in order to partner. We expect market capacity across specialties to be an important driver of their strategy.

Tess Niewood

Consultant

Max Holle

Summer Associate

[1] We have had occasion to test Physician Compare vs. more accurate data in individual markets. In our experience, any one snapshot of Physician Compare is about 90% accurate relative to the current view. To avoid “double-counting” of physicians listed at multiple locations we assign an FTE value to each location (i.e. a doctor with two practice locations would be listed at both as a 0.5 FTE). Further, the data quality is not great for pediatrics (given the Medicare focus).

[2] The dramatic increase in APN capacity according to the physician compare database seems to stem at least in part from a shift in reporting standards, and so may exaggerate the actual increase. Notably, however, Nevada expanded the scope of independent practice for nurse practitioners in 2013.

[3] “Total” row includes a handful of other specialties of which Optum employs a provider or two

[4] “Total” row includes a handful of other specialties of which Optum employs a provider or two

[5] It is easy to assume that Optum will continue to grow its primary care capacity in these counties given the deep specialty care network in place.