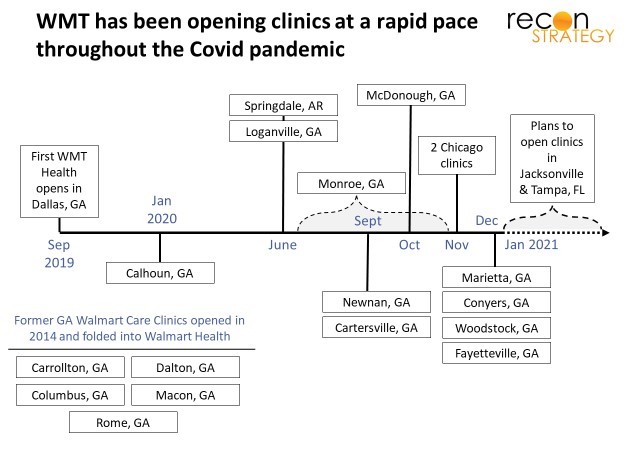

Eighteen months ago, WMT opened its first Walmart Health clinic attached to a supercenter in Dallas, GA. The operation combined multiple services – primary/urgent care, dentistry, behavioral health, optometry, and audiology – with WMT’s Every Day Low Price philosophy (for example, $30 total for a primary care check-up, $40 for a sick visit) in one ~11K sq. ft. site.

Boosted by typical supercenter traffic (~5K visits a day is our estimate), and a scarcity of primary and dental care in the local area[1], the clinic got to 2.3K visits-per-month within 90 days of opening[2] (pre-Covid). More clinics opened in quick succession. There are now 16 sites in Georgia, 2 in Chicago, 1 in Arkansas and plans to launch in Jacksonville (7 sites), Orlando and Tampa this year. Notably, many were opened, and plans were announced after we were well into the pandemic.

If you would at last prevail, try, try again…

This is not the first time WMT has put clinics in supercenters. Not the second time either. By our count, this is the fifth time WMT has publicly disclosed (once inadvertently) a big push into primary care delivery in the last 15 years[3]:

The model has varied: first, WMT rented space to entrepreneur physicians who proved unstable business partners, then rented space to delivery systems which, it turned out, had their own agendas. This was followed by owning the clinics and partnering for staff and now, owning the clinics and employing the staff[4]. So there has been learning along the way. But, given this track record, a big announcement and a couple dozen site launches are not evidence of strategic commitment. An enterprise as vast as WMT has an understandably hard time paying attention to something as operationally complicated and top-line immaterial (relatively) as care delivery.

Going where the money is

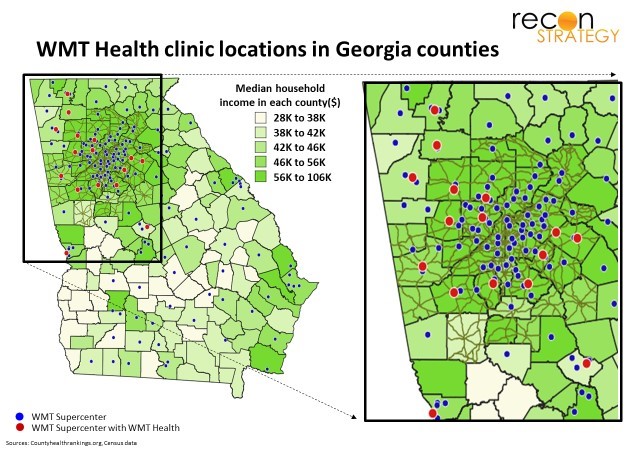

Public discussion of the Dallas siting decision emphasized the lack of local primary and dental care options. Addressing access constraints with a low-price model bringing together clinically synergistic services is both a worthy public health goal, and – evidently, given the speedy ramp in visits in Dallas – a surefire way to get patients. But, as Walmart Health launched more clinics, local scarcity of care seemed to fade in importance[5]. The more consistent focus has been on locating in counties which were populous, suburban, and relatively wealthy[6].

While low prices for basic services would appeal to any income bracket, people in higher income areas can also afford all the optional services and upgrades on dispensed items. Thus, the business strategy appears to be focused on cross-selling and upselling to “disposably incomed” supercenter traffic with an operating model otherwise stripped down with classic WMT operating efficiency.

But are Walmart Health clinics, in fact, making money? Barely…maybe….

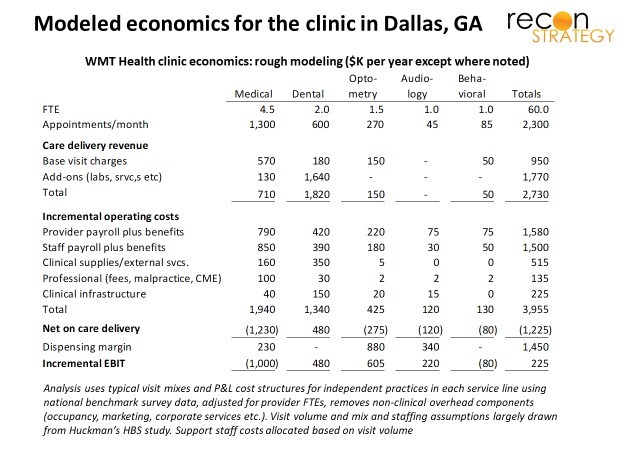

Given the size of the Dallas provider team, 2.3K clinic visits per month is probably near capacity. Most clinics – with heavy fixed costs – would be highly profitable with that kind of operating leverage. WMT’s model trades low prices for the base visit (e.g., $30/40 for primary care vs. the median commercial rate closer to $100+) for sharing infrastructure with a supercenter. Assuming those sharable costs (rent, marketing, etc.) are effectively zero and encumbering the clinic P&L only with clinically incremental costs, there does appear to be a path to make some money. Guesswork derived from national benchmark data and various rules of thumb shown in the exhibit below:

This view of clinic economics is a best case in that it assumes the clinic will

- Sustain 2.3K visits per month

- Upsell high margin add-on services (e.g., diagnostics, teeth whitening) and dispense high margin devices (eyeglasses with all the trimmings and some spares, custom fit hearing aids), and

- Get full credit for dispensing prescribed drugs (some WMT customers would have filled scripts at WMT pharmacies irrespective of where the prescriber sat)[7].

Putting this all together, we guess the clinic earns ~$5-10 margin per visit or ~$15-25 per square foot.

These economics are, in several senses, artificial and vulnerable:

- The margin is dependent on the non-clinical overhead (which would cost a stand-alone medical or dental office $20-30 per visit) being absorbed into the supercenter P&L

- Optometry is already a proven stand-alone business within many supercenters. Folding its earning power into Walmart Health is another kind of subsidy

- With the pandemic, telehealth has become a more broadly adopted platform for delivering minor acute care at a convenient time and place — competing directly with an important part of Walmart Health’s value proposition[8].

Synergies for the supercenter also seem small. “Amazon-hardening” 2.3K visits a month won’t mean much to the bottom line of a supercenter built for 5K visits a day. Also, traffic generation requires clinics, not necessarily clinic ownership. That business case would require that ownership is a prerequisite for operational success within WMT — a real question given the various partnership models for primary care WMT has tried and abandoned over the last 15 years.

Dallas (GA), meet Dallas (TX)

It happens to also be a question which WMT is testing again right now. While launching its own clinics in the southeast, WMT has also been setting up an alternative model in Texas. In September 2020[9], they announced a partnership with Oak Street Health (OSH) to put clinics in three supercenters in the DFW metro area.

On one level, the model is a throwback to WMT’s 2005-10 forays with established providers leasing space and putting own branded clinics inside supercenters as nodes in a broader network[10]. OSH is, however, different from these past partners in that it:

- Is well-capitalized to drive nationally scaled ambitions (vs. the one-off local partnership models used before)

- Takes risk on Medicare populations rather pushing up visit volume or capturing patients for procedural care and guiding them offsite.

OSH’s high touch approach[11] is designed to manage patients out of avoidable hospital visits, resolve gaps in care and fully document underlying clinical issues. It works great in Medicare (but is less suited for younger populations[12]) and, by taking risk, can turn primary care into a highly profitable business[13].

Walmart Health is trying to get closer to Medicare Advantage (MA). In October last year, WMT launched a co-branded health plan (LiveHealthy PPO) with Clover in a handful of Georgia counties with Walmart Health locations. A greenfield start in MA is hard, though. By January 2021, Clover attracted only 900 MA lives in those counties (for reference, HUM has 58K lives in those same counties, 12K more than the previous year). Even if Walmart Health grows its panels enough to support a risk deal, the operating model is structured to deliver fast, efficient access – very different, perhaps fundamentally at odds with the kind of deep relationship building needed for winning at capitation in MA[14].

Path forward

Comparing the two paths, the OSH partnership likely “spreadsheets” better. The $15-$25 EBIT per square foot per year which we guess the Dallas Walmart Health clinic generates under optimistic assumptions roughly equals the typical medical office rent. Assuming some share of visits also generate incremental shopping at the rest of the supercenter, you might see a return under best case assumptions better than average rent. But, unlike rent from a big public company, the profit stream would also need to be adjusted for operational ramp and business risk[15].

Could Walmart Health create a stronger value proposition for the mothership? The recent departure of the Walmart Health senior team suggests there may be an opportunity for a rethink. We see three possible options:

Fix primary care model value capture

Consider how low does the every day low price really need to go to conform to the Walmart value proposition. Does Walmart Health need to charge $40 for a sick or injury visit when an urgent care center will charge more than twice that?

Unbundle the template, stop the cross-subsidization and drop full primary care

While primary care loses money, dental looks like a financial winner because of the broad potential for add-ons. One can easily imagine Walmart Dental standing up beside Walmart Optical as a store-within-a-store model and being rolled out across hundreds of supercenters. Stripped of onsite providers, Walmart Health could expand various technical services supporting primary care which are unavoidably in person (diagnostics for example), thereby serving as a nationally scaled “last mile” solution for the emerging cohort of virtual first plans and telehealth vendors seeking wrap-arounds[16].

The potential for clinical synergies across the Walmart Health bundle (dental <-> primary care, optical <-> primary care, behavioral <-> primary care) would be sad to lose, but unleashing Walmart’s operational strengths and low-price philosophy on dental care or distributed access for technical services across the country could be transformative.

Get out of the suburbs, dive deeper into rural care

Most FFS primary care is actually pretty cheap and now more available with the broader adoption of telehealth. There is just not that much opportunity for Walmart to apply the game it knows so well (every day low prices and nationally scaled operational efficiency). This is especially true in the suburbs.

Rural markets, on the other hand, are seeing healthcare hollowed out as providers struggle with spreading big fixed costs and antiquated operational models across subscale catchment areas. WMT knows this well. Many of its customers and employees are ensnared in the issue.

Over the past 5 years or so, however, a variety of highly innovative concepts with clear potential for the rural environment are emerging: telehealth, centers of excellence/medical tourism, ambulatory and micro-facility models, and @home. What if WMT backfills declining rural care with creative combinations of these concepts built on supercenter platforms? Its distributed network and the vast space in each node make it uniquely suited for such a move. WMT could take a large slice out of overhead by supplying readily accessible locations, management infrastructure, procurement and logistics (including now in-home delivery) all at low marginal cost.

In a broader scope of care, there would be many more opportunities for WMT’s capabilities in operational efficiency. The arbitrage on site of service could fund a nice profit stream while helping high value local providers by extending their geographic reach. Finally, the bigger top line arising from participating in a much larger share of care delivery will help hold onto senior management attention[17].

* * *

Walmart Health’s approach to primary care is too small and conflicted to work long-term (and risks dragging down dental – which we guess to have high potential as a stand-alone). But the potential for WMT in healthcare is enormous: its management team has been visionary with regards to its own employees and public health minded in general (e.g., setting up access points in stores for the VA, and for behavioral health – no money maker! – in collaboration with Beacon Health Options starting in 2018). Despite its size, it has been transformational, innovative and agile (e.g., responding to AMZN, Covid).

Five bites at the apple show that WMT is committed to finding a path into healthcare. Please, WMT, don’t make us write a few years from now about how attempt #5 faded and a sixth new attempt is being put in motion. Make this one work!

Anja Schempf

Associate Consultant

Tory Wolff

Managing Partner

[1] Paulding County has ~6.4K+ people per primary care provider and ~6.3K for every dentist compared with about 1.6K people per primary care provider and 2K people for every dentist average for all of Georgia.

[2] Per Huckman et al “Walmart Health: Scaling During a Pandemic”, HBS, September 24, 2020.

[3] Not including WMT’s public flirtation with acquiring HUM back in the spring of 2018 – a concept we liked mostly as a way to turbocharge HUM’s commercial business. We would guess one thesis behind the deal was to put clinics inside supercenters to accelerate the growth for Humana’s owned network of clinics. Once they went separate ways, WMT went on to launch Walmart Health (Sean Slovenski who led the initiative joined Walmart in the summer of 2018) and Humana put together a “complicated, expensive” deal (per Broussard) with Welsh Carson to grow its Partners in Primary Care clinics.

[4] The providers appear to be independent.

[5] For example, Bibb, Fayette, Floyd, and Muscogee all have <1K people per PCP; Fayette, Muskogee and Bibb have <2K people per dentist (Floyd has 2.4K people per dentist).

[6] Our statistical analysis of what distinguishes counties where WMT set up clinics vs. just had supercenters looked at population, population density, population growth, primary and dental care access (measured as inhabitants per local provider), hospital beds per capita, share of Medicare and Medicaid coverage, median income and number of supercenters in the county. Of those, only population, growth, income and supercenter number were significant. Population and income were positively linked with clinics, population growth and supercenters were negatively correlated. The population growth relationship was surprising given that most of the counties where WMT located clinics saw growth. However, many Georgia counties with high median income also saw population growth. WMT appeared to locate clinics in those counties within that subset with slower (but still positive) growth.

[7] The modeling also assumes primary care would collect regular Medicare FFS pricing for those patients.

[8] WMT does have experience with telehealth both for its employee (for example a program to give employees in some markets access to a personal primary care physician and behavioral health services from Doctors on Demand for a $4 per visit co-pay) and to the VA (since 2018, WMT has donated sites and equipment which VA providers can use to deliver primary and other routine care including behavioral to veterans), Integrating that experience and capabilities into the Walmart Health clinics, however, will take time. CVS, for example, began piloting telehealth integration with Minute Clinics in 2015.

[9] For the Kreliminologically minded, this was one month after Sean Slovenski who was running Walmart Health up until that point, announced his departure from WMT.

[10] Oak Street has launched 3 other clinics in stand-alone sites (not in supercenters) in the DFW area.

[11] Oak Street is not unique here – broadly the same approach is used by a growing cohort of advanced primary care practices such as Iora, ChenMed, WellMed and VillageMD.

[12] Oak Street emphasized its focus on Medicare Advantage patients in the press release announcing the WMT deal (“While all members of the community – from toddlers to seniors – are welcome at these clinics, Oak Street Health’s focus in its growing network of more than 60 primary care centers remains adults on Medicare.”)

[13] Oak Street’s interest in CMS’s new primary care models for Medicare FFS suggests that they won’t just be focused on WMT’s seniors with Medicare Advantage coverage either.

[14] In some senses, the Walmart Health model is trying to have both a convenient, transactional urgent care (walk-ins welcome!) and deeply engaging medical homes at the same site. The Dallas site for example, per the HBS study, there are community health workers (CHWs) who counsel patients on health habits (e.g., nutrition) and basics (e.g., navigate diabetes supplies) and are very popular and provided at no charge to the patient. CHWs are powerful assets in a true medical home (funded by a risk model) but can add cost without some funding model (it is unlikely that the shopping baskets of counseled patients are incrementally large enough to pay for the cost of the counseling.

[15] Keep in mind, our modeling for Walmart Health economics was a best case based on traffic achieved pre-Covid. It is hard to imagine those kinds of volumes were maintained through the pandemic while all that capacity had to be kept up and running.

[16] Walmart is already experimenting with serving as specimen collection points for Quest Labs with reportedly great success. Digital front sore / digital first models and plans are now struggling with how to manage the care models with require.

[17] With the reshuffling of people’s location preferences post Covid and broader adoption of remote work, small town and rural populations may stabilize and perhaps even grow and clinical talent may be easier to recruit.