We identify four different business strategy rationales for hospital@home depending on each hospital’s specific market situation and each with clear predictive implications for local markets. These are: on-demand capacity expansion, bed capacity rationalization, competitive matching and system consistency. Almost all participants in CMS’s current Hospital@home program could find one of these four rationales applicable. If these rationales become compelling business cases, the future of hospital@home is bright and it is time to start the healthcare ecosystem to prepare for its disruptive consequences.

The cannibalization challenge

Hospital@home uses innovative protocols, technology, and in-home rounding to provide hospital-grade care to curated sets of patients – typically lower risk medical admissions – in their own homes. Results in clinical outcomes, patient experience and care cost have been impressive. Several systems (especially academic) have incubated programs for several years. With Covid, the model has become much more widespread.

Yet, by drawing patients out of hospital beds, the model creates a business strategy dilemma. Bed occupancy is a key driver of hospital profitability[1]. How can the business case for hospital@home be reconciled with the economic imperative to exploit the costly infrastructure thoroughly and efficiently inside the hospital’s four walls[2]?

If the implicit conflict between hospital@home and traditional hospital economics cannot be solved, then hospital@home – at least as provided by incumbent hospitals[3] – will remain a curiosity and side show. On the other hand, if there is a compelling business strategy which supports – or replaces – traditional hospital economics, then the model can become a long-term meaningful part of care.

Who is participating?

Last year, CMS launched “Acute Hospital Care at Home” and, as of April 30, 56 health systems have been approved for the program. Presupposing that participation in this temporary program indicates a long-term commitment to hospital@home, we can compare the strategic situations of these systems[4] with non-participating competitors[5] and speculate about the long-term business strategy which makes the cannibalization risk worthwhile. (Note: we are not asserting that any of these hospitals are undertaking hospital@home for any of the hypothetical rationales we describe, just that the posited rationales are ways the cannibalization dilemma might be resolved).

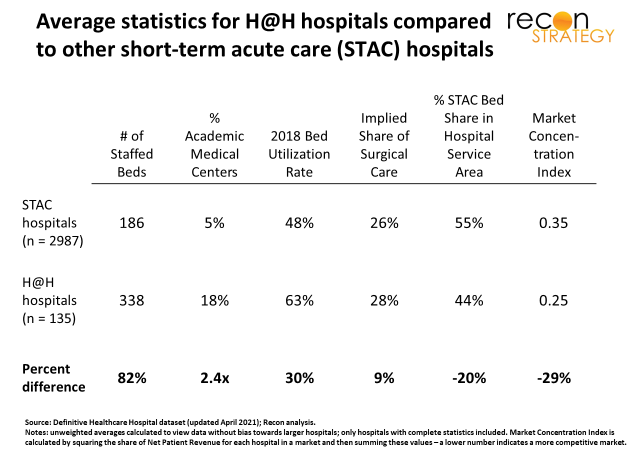

Overall, hospital@home participants skew larger, are more frequently part of Integrated Delivery Systems and more often academic – no surprise given the innovative energy and resources required to launch a major initiative like hospital@home. Intriguingly, they also tend to operate in more fragmented markets (as indicated by the lower Market Concentration Index[6]) and have on average higher bed occupancy[7].

Hospital@home as growth strategy

Medical admissions tend to be uncontrollable, so higher occupancy means a hospital may often be full. If a bunch of low-risk medical admissions come in, the hospital may have to divert more serious cases or delay/forgo schedulable admissions (often surgical and profitable). Adding capacity could help but requires a lot of regulatory navigation (e.g., CON), capex, and commitment to ongoing fixed costs. On the other hand, hospital@home converts patient homes to “on demand” capacity so beds inside the four walls can be kept free for additional admissions – either higher risk medical or profitable procedural ones.

Notably, hospital@home participants appear to have both the opportunity and incentive to grow procedural care[8]: Relative to counterparts, they tend to:

- Be in more fragmented markets, suggesting weaker competitors and more opportunity for share gain, and

- Have an advantaged payer mix[9] which would strengthen the business case to invest in hospital@home in return for more surgeries

Thus, one rationale for hospital@home is enabling on demand capacity expansion (and potentially case mix enhancement within the four hospital walls).

Case mix optimization may not be the game for everyone

While this logic could work for a lot of hospital@home participants, it does not apply for all. A sizeable number of hospitals (smaller ones to be sure) face very different situations and are still participating in the program.

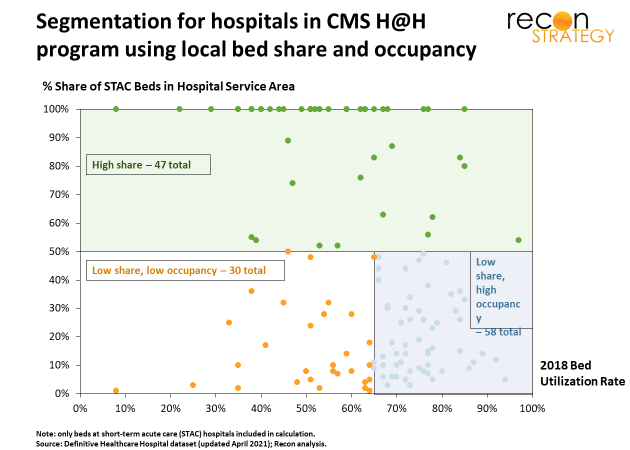

Look at the scatterplot below which shows all the hospitals participating in the CMS program scattered based on their bed occupancy (x-axis) and share of short-term acute care (STAC) staffed beds within their hospital service area (y-axis).

A lot of participants have high market share (and thus less opportunity to grow) or have low occupancy (therefore less opportunity cost for keeping a low-risk medical admission in a bed) or both[10]. What could be going on with these other hospitals?

Rethinking the footprint, optimizing the infrastructure

High market share may open the door to an operating cost reduction opportunity. Hospital@home has lower costs per comparable admission because of shorter length of stay (LOS) and less care activity during the admission. Some studies suggest cost reductions in the 10-20% range. By diverting a material share of low-risk admissions back to the home, the hospital can improve the margin on these admissions. Of course, this would raise the fixed cost burden on the remaining in-hospital admissions. However, once the program gets to critical mass[11], the hospital could trim its bed capacity to match a reduced volume of generally higher risk patients, reducing the fixed cost burden and improving overall operating economics.

Consistent with this potential rationale, the hospital@home participants with high market share tend to have lower average acuity admissions, weaker payer mix and a lower share of surgical care, all of which would suggest a very large opportunity for hospital@home. In more dynamic markets where share can be gained or lost, a hospital might be tempted to hold onto its beds, blunting the potential cost efficiencies[12]. Where the hospital is secure in its market leadership, however, bed capacity rationalization (a second potential rationale for hospital@home) could be positioned as a transformation, not a retreat.

Fast followers for two different reasons

That still leaves us with 30 hospitals participating in hospital@home with both low occupancy and low STAC bed share (lower left-hand quadrant in the chart).

18 of these directly compete with hospitals which are participating in the hospital@home program[13]. These hospitals also have very attractive payer mixes (high share of commercial). Perhaps what we are seeing here is defensive competitive matching (a third rationale) to hold on to commercially insured patients attracted to innovative hospital brands. The business risk of cannibalizing a patient by sending them into hospital@home is better than losing that patient altogether.

Of the remaining 12, almost all are part of health systems containing larger hospitals with hospital@home programs. Their participation may be driven by a system-wide initiative rather than local market conditions — in other words, system consistency (a fourth and final rationale). Allocating some of the fixed costs for launching hospital@home over a larger number of hospitals can make the program more economical. Intriguingly, the hospitals in this group of system followers tend to have larger STAC bed shares than, for example, those falling in the “competitive matching” segment. They also have less attractive payer mixes. Ultimately, these hospitals may see an efficiency opportunity in rationalizing bed mixes for a smaller – but more complicated – flow of patients inside the four walls.

* * *

A few implications

There appear to be at least four plausible rationales for undertaking hospital@home which will support its long-term viability even in the face of cannibalization risk:

- On demand capacity expansion: opening beds for higher margin care

- Bed capacity rationalization: make costly in-hospital bed capacity redundant

- Competitive matching: maintaining innovative brand positioning

- System consistency: ensuring a consistent system face to the market.

In markets where hospitals are looking to use on-demand capacity expansion to enhance their share and case mix, there will likely be losers (the procedural care must come from somewhere) which will have repercussions on their economics. Payers supporting hospital@home with one hospital may find these systems coming back with requests for relief.

While on demand capacity expansion appears to be the most broadly applicable rationale now (based on the share of total beds among participating hospitals), competitive matching is perhaps the most interesting. New models of care are adopted more quickly and broadly when they ae linked with competition.

—

[1] See for a recent reconfirmation of this rule of thumb, Rosko et al. “Efficiency and profitability in US not-for-profit hospitals” International Journal of Health Economics and Management, 2020. This study looked at the margins of 1,317 acute care hospitals in 2015. Even when incorporating a wide range of economic drivers (including the usual suspects of academic status, payer mix, market concentration and an innovative measure of operating efficiency), occupancy remained a critical driver. Per Table 3 in that study, increasing bed occupancy by 10 percentage points would add 0.65% to the operating margin.

[2] Occupancy is not just about the full allocation of fixed costs inside the building. In our experience, the clinical team willing and able to operate in the home setting tend to be of a different phenotype than those who prefer to deliver care inside the hospital with all its resources. This implies that the care team for hospital at home is not fully fungible from those within the hospital.

[3] Some players such as Dispatch Health are experimenting with hospital@home without the hospital which will not face the cannibalization issue.

[4] Hospitals listed on the CMS website and hospitals in listed systems with identified hospital@home programs were analyzed if 2018 Bed Utilization Rate and Number of Staffed Beds data were available.

[5] Short-term acute care hospitals with available data from Definitive Healthcare – including 2018 Bed Utilization Rate and Number of Staffed Beds – were analyzed. Unweighted averages were calculated to view each case without bias towards larger hospitals.

[6] Market Concentration Index is derived by Herfindahl-Hirschman Index, a statistic that sums the squares of individual market participants’ market shares and provides an indication if market share if evenly distributed across participants or if there is a small number of very large players. In this situation, the share of Net Patient Revenue for each hospital in a market is squared and then summed, with a lower number indicating a more competitive market.

[7] 2018 Bed Occupancy Rate was analyzed to avoid any COVID-19 pandemic distortion.

[8] Of course, the hospital could also keep beds open for more medical admissions; however, these tend to be less profitable and, because they are less controllable, they are harder to grow strategically.

[9] (61% private/self, 31% Medicare, 8% Medicaid) than those not participating (57% private/self, 34% Medicare and 9% Medicaid

[10] The hospitals we hypothesize as potential “case mix enhancers” (low market share/high occupancy) tend be much larger than the other participants, so their market characteristics tend to dominate in any statistical average view across participating hospitals.

[11] Easier in markets where the hospital has high share because the messaging on clinical quality of hospital@home can be more consistent.

[12] For example, suppose 20% of admissions were diverted home and the care costing 10% less. That would add 2% to the hospital operating margin (assuming no change in negotiated rates). However, a 20% reduction in occupancy would also drive at least ~1.3% reduction in operating margin because of reallocation of fixed costs (see note 1 above. Actually, likely much more because the occupancy impact on margin estimated in this paper is measured on an average not marginal basis) for a net impact of ~0.7%. If the hospital could restructure its beds to match a 20% reduction in occupancy, however, then the full 2% would be available to enhance its bottom line.

[13] Defined as Hospital Service Area (which breaks the US market up into 3,436 different regions).