What is revenue cycle management?

Revenue cycle management (RCM) is the process of converting care delivery into cash. At its most comprehensive, services include:

- patient intake (scheduling/registration, coverage verification and financial counseling)

- claim submission (charge capture, coding, documentation, submission), and

- payment capture (payment processing, denials, customer service and collections).

Effective RCM is challenging because of:

- The variety of plans and benefits designs (what’s covered, patient co-pays, rates, etc.),

- Ambiguities of payer approval of specific clinical services (prior authorization, etc.),

- Requirements and opportunities in characterizing the care and patient risk (e.g., coding),

- Complexity of contracts (e.g., getting appropriate credit for value-based deals), and

- Evolving regulations (e.g., all the Covid emergency measures).

Given this complexity and importance of the ultimate deliverable (cash), providers spend a lot on RCM—between $50-100B overall.

RCM outsourcing small but growing

While only 20-30% of RCM is outsourced today,[1] that share is growing fast. Here’s why: as it is a back-office function, RCM is not usually seen by providers as a basis for strategic advantage. On the other hand, because expertise and technology are key to effective RCM, operational scale is critical. Therefore, consolidating RCM across multiple delivery systems onto a “utility” vendor operating on a white label basis can benefit each (by pooling scale) while harming none.

Logically enough, several of the largest delivery systems—Ascension, HCA, Tenet, and Bon Secours Mercy —have spun their internal RCM functions into subsidiary/co-owned companies (as R1, Parallon, Conifer, and Ensemble, respectively, making up 4 of the top 5 end-to-end RCM outsourcers) and sell services to other providers (with mixed success[2]). Most often, these deals look like classic business process outsourcing (BPO), with the client’s RCM staff rebadging on the contract’s Day One to become employees of the vendor.

These vendors largely have remained stand-alone “pure plays.” Dimensions of competition have focused on adding scale, automation/digitization, and improving patient experience with the administration aspects of care.[3]

Optum using an RCM BPO anchor to build more strategic relationships

Optum360 is the outlier among the Big Five given its very different corporate parentage and sibling relationships (as a company within OptumInsight and part of UNH overall).

Historically, Optum360 played the game in end-to-end RCM BPO the same as the pure plays[4] and done well with it.[5]

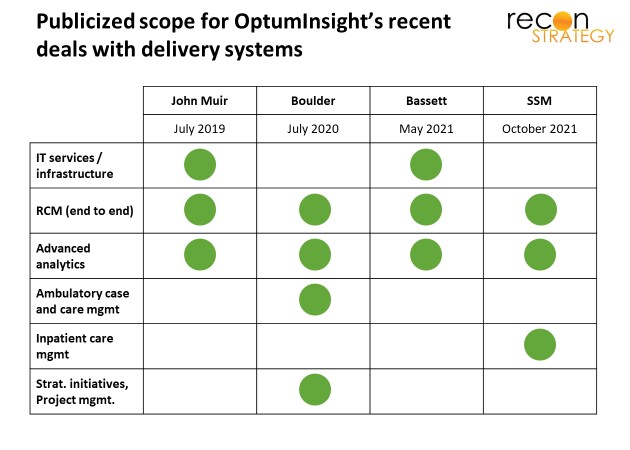

In four recent deals involving RCM, however, OptumInsight has bundled additional services into RCM BPO drawn from the rest of its product portfolio:

- IT management services outsourcing (across two deals),

- Advanced analytics (across all four deals),

- Ambulatory case and care management plus strategic project management (Boulder Community Health), and

- Inpatient care management (SSM Health).

The IT services product seems similar to RCM in that the delivery system is swapping out a well-defined subscale back-office function for a better scaled vendor. The advanced analytics and care management services are different:

The analytics are described as providing the point of care with targeted care recommendations, serving up disparate patient SDoH information, and driving more consistent clinical decision-making. SSM, in particular, is expecting the analytics to “reduce care variation” and support a “new inpatient delivery model” to reduce length of stay (LOS) (perhaps tying in the SDoH data to facilitate more nuanced discharge planning).

The care management is a rebadging of client staff: Boulder is transitioning its nurse care managers, nurses, and social workers overseeing populations in the ambulatory setting (as well as directly engaging with patients) over to Optum career tracks. SSM is planning on transitioning ~300 of its inpatient care managers to the Optum organization.

Essentially, these systems are handing over some of the keys to operating key aspects of care within the delivery system, making the relationship more strategic.

Logic for the bundle

There are a lot of potential synergies from combining RCM, analytics, and care management. A few quick scenarios:

- Analytics flags SDoH barriers for a patient, RCM identifies resources to address them (e.g., out of a value-based agreement), and care management put the solutions in place,

- RCM identifies the payment model and benefit design for an admitted patient (e.g., % of charges, DRG, capitation) early enough so that case management can design a care plan which optimizes fixed cost/variable cost trade-offs and patient cost share,

- Case managers keep RCM in the loop on patients with upcoming procedures so RCM can expedite payer authorization, reducing payment uncertainty at discharge,[6]

- Analytics predicts a patient’s post-acute trajectory at admission, giving discharge planners plenty of time to tweak discharge timing and line up resources.

In any of these scenarios, rewiring of the cross-functional workflow is required. Carving care management over to Optum (in the case of Boulder and SSM) implies a few things:

- The change management challenges behind this rewiring can be addressed more easily if the insights and the execution are organizationally integrated,

- The ultimate fruits of this rewiring outweigh any frictions of having care management and care delivery report up different chains of command, and

- Optum likely has performance components in these agreements (a natural corollary to owning the execution), strengthening the strategic aspects of the partnership.

Not every delivery system will find a broader bundle attractive (John Muir and Bassett, for example, evidently wanted to keep control of execution). But the appeal of Optum’s offer also won’t just be for marginal or struggling systems either: SSM is a very large, $8B multi-regional system with its own health plan and PBM, well-respected by bond holders. And while it is usually the #2 in each of its markets, its average LOS is significantly less than its surrounding competitors (with comparable case mix indices) and average bed occupancy is marginally higher. Of course, aggregate data may mask targeted opportunities for improvement which Optum can surface.[7] SSM’s lower share of surgical cases relative to competitors suggests some opportunity for admission mix improvement.[8] See exhibit.

Implications

By expanding the scope of services from back-office into clinical, OptumInsight is building strategic relationships with delivery systems “from the inside out.” This pairs well with the relationship UNH’s health plan can build “from the outside in.” In the case of John Muir, for example, where there are several product alignments.[9]

Other RCM BPO vendors face a real threat. Right now, they cannot match OptumInsight’s analytical/care management bundles. If OptumInsight’s offer gains traction (and the SSM win is certainly a big reason to think that it will), these players will need new capabilities to compete (most likely inorganically). But even if they can acquire comparable capabilities, Optum is already a step ahead with ready to go outsourced hospitalist services (Sound Physicians) and post-acute optimization (naviHealth) as logical extensions on its analytically driven inpatient care management.[10]

More generally, Optum is setting up a powerful flywheel. The more services these systems buy from Optum, the more Optum effectively becomes the “Intel inside” of delivery system performance, the better these systems perform and the better value they deliver United’s health plan. Many of these delivery systems said they chose Optum to avoid having to join up with other systems, as a way to “stay independent.” Ultimately, however, these systems will become—despite their legal independence and non-profit status—de facto extensions of Optum’s influence on US healthcare.

Tory Wolff

Managing Partner

[1] The long tail of small-scale vendors and clients (such as small physician practices) make estimating the market size and outsourcing share challenging, so estimates vary widely. Data noted is taken from Ensemble Health (their S-1) at the lower end and from R1 (from analyst reports commenting on the company) at the upper end. An industry rule of thumb is that average RCM costs are about ~5% of revenues and 5-10% of a typical delivery systems’ employee base (when RCM is insourced).

[2] Sometimes, financial investors (e.g., going public or taking on private equity) take a share of the subsidiary to provide focus on the external growth agenda. And sometimes they don’t, and the vendor stays introspective: for example, Conifer is jointly owned by Tenet (76%) and CommonSpirit (24%) and the vast majority of Conifer’s $1.3B in revenues (83%) still come from its parents. Parallon is also widely regarded as focusing on internal customers. Notably, Tenet is reportedly planning on spinning out Conifer into a public offer in 2022.

[3] Over last few years, R1, for example, has:

- Acquired Intermedix (with a large physician practice ambulatory footprint) in 2018 and Cerner’s struggling RCM operation in August 2020, adding customers to its platform,

- Acquired SCI Solutions in April 2020, which supports digital front door strategies such as self-serve scheduling and patient access, and VisitPay in May 2021, a digital consumer payments platform, and

- Invested in digital transformation (launching a dedicated office in November 2018) and machine learning to support automation (first machine learning model implemented in 3Q in 2020).

[4] Optum360 made its big play for growth in 2013 with an alliance with Dignity, taking over its operations in return for a minority share in Optum360. See Marrying into the right family: the bets underlying United’s revenue cycle management joint venture with Dignity Health. CommonSpirit (which succeeded Dignity in its ownership share) recently reduced its ownership stake in Optum360 from 23% (a position which arose out of the September 2013 alliance) to 4.15% in March 2021 by selling shares back to UNH.

[5] See Marrying into the right family pays off! Update on revenue cycle management joint venturing.

[6] A few years ago, RCM outsourcer Parallon found that 24% of their client’s write-offs were for inpatient clients which remained unauthorized at point of discharge. Declining LOS leaves less time for busy case managers to secure payer approvals. Parallon—stuck in the RCM work scope—could only propose throwing more denial resolution bodies retroactively at the problem for marginal improvement. See Parallon “Preventing Denials through Teamwork, Innovation and Technology,” Perspective Brief white paper available on their website and dated 2015.

[7] For example: SSM’s second largest hospital, St. Anthony in Oklahoma City has occupancy of 74% vs. 67% for the local market and surgical share of care delivery of 31% of discharges vs. 36% of discharges for its competitors. If more bed capacity could be opened, St. Anthony’s might be able to increase its share of profitable surgeries in this market. Notably, St. Anthony’s surgical case mix index was also lower than the market average (3.06 vs. 3.15).

[8] To the extent that the Optum deals free up bed capacity, perhaps some other Optum assets could help their clients sort out the most profitable surgeries to fill those beds such as some of the Advisory Board analytical tools.

[9] These include:

- UNH’s Signature Value product in California couples John Muir in the Bay Area with its OptumCare delivery network in Southern California

- UNH uses Canopy Health (a John Muir joint ventured delivery network) to cover John Muir employees

- UNH launched the California Doctors Plan in 2020 with Canopy promising premium savings of up to 25%.

[10] Granted, these would likely take some work to put into reality. All the assets in the four deals discussed here are part of OptumInsight while Sound and naviHealth are part of OptumHealth. Despite the common parent and a lot of marketing spin about the UnitedHealth “family,” individual parts of Optum are very competitive and collaborating across BU’s does not always come naturally.