PDF: Trends and strategy in oncology development

Summary

We review a sample of oncology programs from the past decade and arrive at the following key findings:

- The use of expansion cohorts in first-in-human (FIH) studies has grown significantly in the last decade, with an accompanying decrease in separate phase 2 studies

- Commercial-stage sponsors and early-stage companies backed by established VCs are much more aggressive in discontinuing programs quickly compared to other early-stage companies

- For drugs that achieve approval, the time from FIH to approval is much shorter for big pharma programs than for early-stage companies that are not backed by established VCs.

Oncology clinical development is changing

Nowadays, FIH trials in oncology frequently become umbrella studies — in addition to the initial dose-finding component, sponsors add expansion cohorts targeting specific types of tumors as new data become available. In the most spectacular example of this new paradigm, a single NCT number for an FIH trial can, over time, enroll >1000 patients in many expansion cohorts, and lead to an accelerated approval by the FDA. Though not fully Bayesian in form, the intent of these seamless trials is Bayesian in spirit: the study design is dynamically adjusted as information is collected.

This evolution has been noted and discussed in occasional articles and white papers, but has not been formally quantified.[1] Nor have we encountered an analysis of how such structural changes have affected decision making. After all, in drug development, progressing an asset from one phase to another is an extremely momentous decision. Simply adding an expansion cohort to an existing study — less so.

While an exhaustive view of development strategies for oncology is an endeavor beyond the scope of this brief analysis, we have sampled trends with three snapshots:

- 75 oncology assets with FIH trials initiated in the US in 2012

- 76 oncology assets with FIH trials initiated in the US in Q3 & Q4 of 2017

- 26 oncology assets receiving accelerated approval from FDA in 2019, 2020, and 2021

We reviewed the early development strategies for each of the sample groups listed above. For assets with FIH studies in 2012 and 2017, we looked at outcomes (as of April 2023). For approved assets, we looked at the timeline to approval. We found clear differences in strategy between sponsors that are commercial-stage biopharma companies, and those that are early-stage biotech firms. Further, among early-stage companies, those with backing from established VCs have a markedly different approach, likely with significant impact on ROI.

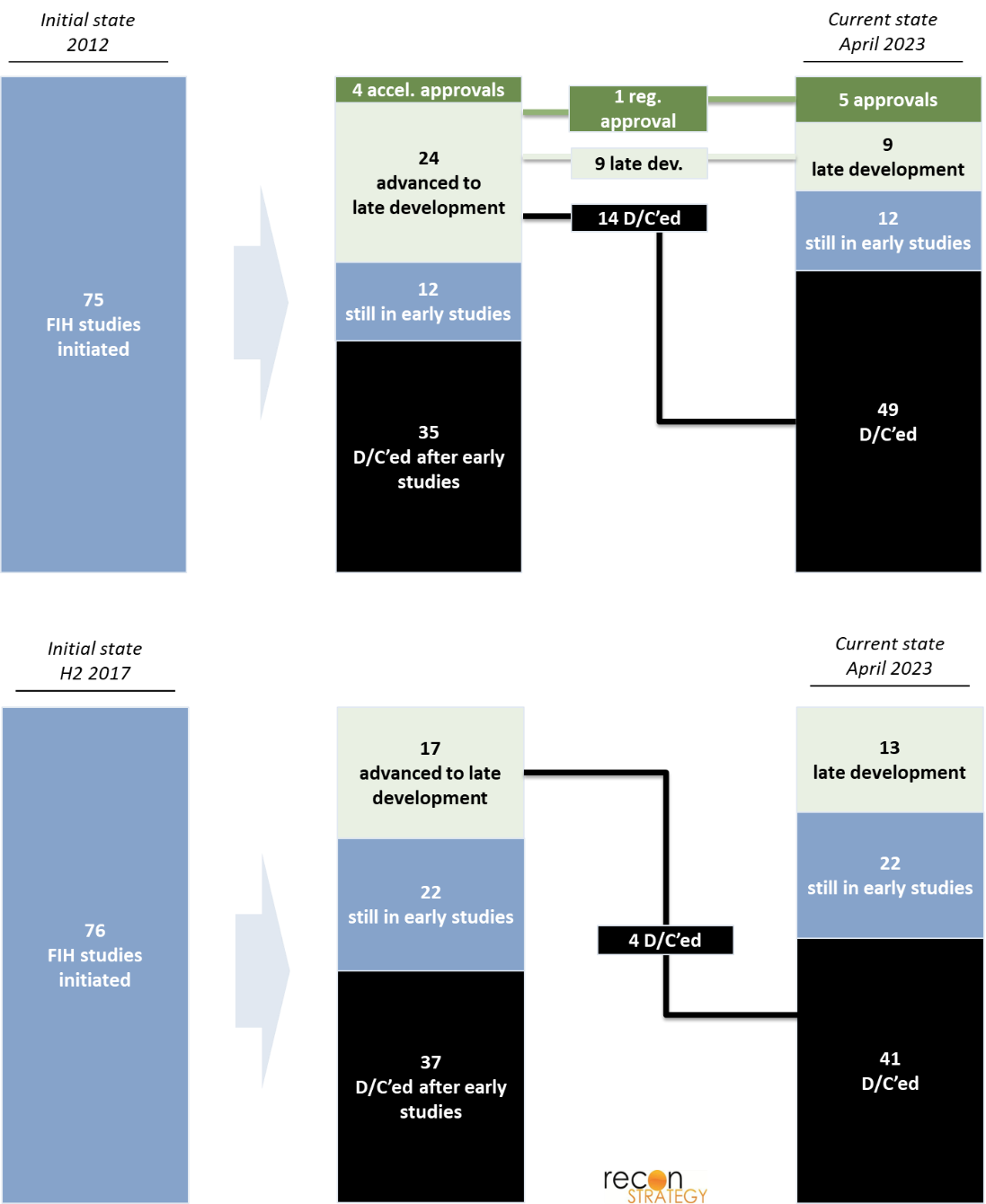

A prospective view: oncology programs entering US-based trials in 2012 vs 2017

In 2012, 75 oncology programs initiated FIH trials in the US. In contrast, between July and December of 2017 alone, 76 programs initiated FIH trials, reflecting the surge in oncology investment and related drug development during the interval. We mapped the outcome of each of these programs as of April 2023 (Exhibit 1). Though many programs are still ongoing, a majority has reached a final state of approval or discontinuation, even for programs that only entered the clinic in the second half of 2017.

Exhibit 1

For each program, we reviewed a broad range of parameters:

- Initial enrollment (specific tissue type, broad solid tumor, hematological malignancy, specific mutation)

- # of enrolled patients

- # of expansion cohorts used

- Type of sponsor (commercial-stage vs. early-stage)

- For early-stage, type of VC backing the company (established vs. other)

- Drug status (d/c after FIH, d/c after pivotal trial, early-stage development, late-stage development, regular approval, accelerated approval)

In the following sections, we highlight a few salient findings from our analysis.

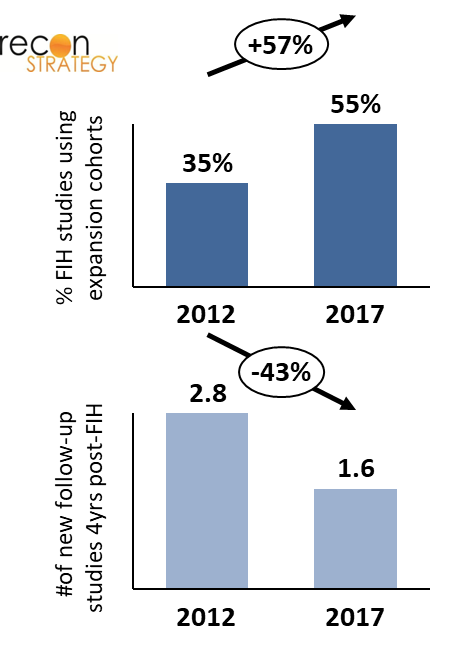

Sponsors increasingly use expansion cohorts in FIH studies in place of launching new trials

Expansion cohorts are increasingly used as an alternative to follow-up trials, as it allows programs to continuously enroll patients with diverse pathologies into one singular FIH trial. There is a clear efficiency benefit to this approach: it expedites development of oncology drugs and biologics by seamlessly proceeding from initial determination of a tolerated dose to assessments that are more typical of phase 2 trials, without the full administrative overhead of standing up a new study. On the other hand, there are risks associated with this methodology. For instance, it exposes more subjects across simultaneously accruing cohorts to potentially toxic doses of an investigational drug. Additionally, misinterpretation of preliminary trial signals based on responses in a subgroup may create faulty assumptions that lead downstream clinical development astray. To mitigate those risks, the FDA has required scientific rationale for inclusion of each population within a cohort, a statistical analysis plan to justify sample size, and updated safety information as available.[2] Still, the use of expansion cohorts has continued to grow over time.

As seen in Exhibit 2, there is a striking increase in use of expansion cohorts within a FIH study between 2012 and 2017: about a third of programs that initiated a FIH trial in 2012 used expansion cohorts, whereas more than half of new programs with FIH in 2017 did. This change has been accompanied by a reduction of the average number of follow-up trials (with distinct NCT #s) initiated over 4 years subsequent to FIH dosing, which almost halved between 2012 and 2017. As the increasing use of expansion cohorts allows for more extensive evaluation of a drug’s efficacy and safety in multiple indications, there is less need for initiating new trials.

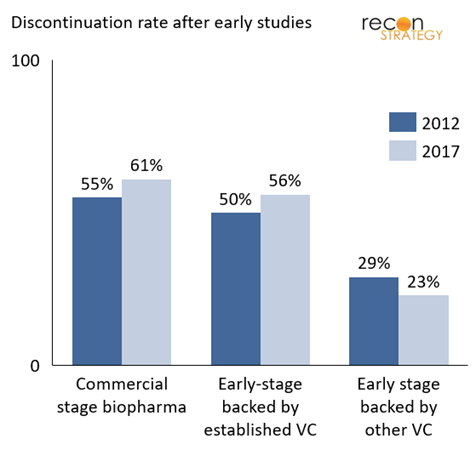

Commercial pharma and biotech backed by established VCs discontinue programs sooner

Exhibit 3 shows the percentage of programs discontinued after the FIH study, categorized by sponsor characteristics. Notably, commercial companies (top 50 pharma companies worldwide by revenue) tend to discontinue a higher proportion of drugs right after FIH studies. Companies backed by established VCs employ a similar strategy.[3] In contrast, early-stage pharmaceutical companies that are not backed by established VCs (identified as backed by other VCs) – are almost 50% less likely to discontinue a drug after its FIH trial. This difference in strategy became even more pronounced from 2012 to 2017, though on analysis, this observation does not rise to statistical significance.

The difference in strategy is likely a reflection of varied sponsor perspectives and incentives. Commercial-stage pharmaceutical companies take a portfolio view and have learned the lesson of the early 2000s that “failing fast” is a key ingredient of a productive R&D engine. To some extent, this is replicated by established biotech VCs who have a broad portfolio of companies and assets. Through their board seats, they can impose a high level of discipline on go/no-go decisions. Early-stage companies and other VC backers without seasoned oversights are more likely to experience concentrated risk, making it more painful to terminate a program. This has obvious consequences for their R&D ROI.

A retrospective view: oncology programs that achieved first approval in 2019 – 2021

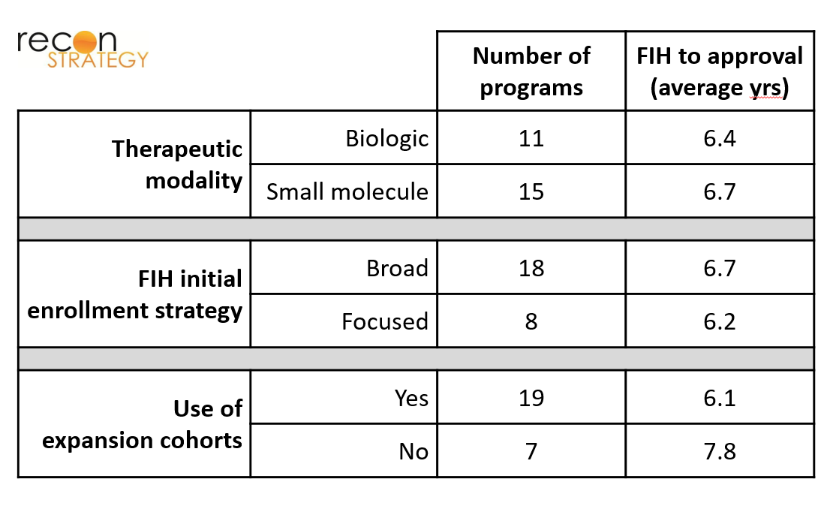

To further explore how the factors mentioned above affect the time and ability of programs to achieve FDA approval, we conducted a retrospective analysis of first approvals of oncology drugs. Specifically, we looked at FIH trials of drugs that received accelerated approval as first approval in the years 2019, 2020, and 2021, with time from FIH to first approval as a primary metric for performance.

We found that the type of indication pursued, type of molecule pursued, and use of expansion cohort did not appear to correlate with time-to-market of an approvable drug. As shown in Exhibit 4, drugs whose FIH trials focused on specific cancer subtypes (patients with specific tissue types / mutations) took the same amount of time to achieve approval as drugs whose FIH trials used a broader initial enrollment strategy (hematological malignancies or all solid tumors). There was also no significant difference in time-to-approval between biologics and small molecules. Although programs that did not make use of expansion cohorts took longer to gain approval, this finding is of marginal statistical significance given the limited sample size (p=0.14 for a 2-tailed t-test), and also potentially a non-causal consequence of the increased use of expansion cohorts over this time period. As one would expect, the average number of patients recruited for FIH trials that used expansion cohorts was significantly higher than in FIH trials that did not use expansion cohorts (290 vs 115 on average).

As for our prospective analysis of programs launched in 2012 and 2017, we compared performance by biopharma company type. As shown in Exhibit 5, drugs from commercial-stage companies reach approval faster than early-stage companies. Within early-stage companies, those backed by established VCs are faster. These differences in time to market will have profound impact on economic performance through three mechanisms: (i) shifting forward in time the revenue stream, (ii) extending the time on market before loss of exclusivity, and (3) in a competitive market, gaining share before others.

Final thoughts: big biopharmas may not be the best innovators, but they are the best at execution

Among some in the life sciences sector, large pharma companies are often regarded as slow, lumbering giants while new biotechs are thought to be quick and nimble. While this may be a perception sometime supported by experience, it is clear that large pharma companies bring a different level of operational efficiency. This comes in the form of staunchly pruning programs deemed to have a low probability of success, as well as accelerated prosecution of clinical development (likely in part due to better resourcing). Early-stage companies backed by experienced VCs come close to replicating that performance, but companies that do not have that backing do markedly worse. There is likely a selection bias whereby less compelling products attract less established funding sources, but the low rate of attrition of these inferior programs is even more of a testament to the lack of rigor in decision making.

Appendix: a subjective list of “established” VCs

Life sciences focused VCs: 5am Ventures, Alta Partners, Arch Venture Partners, Atlas Venture, Bain Capital Life Sciences, Casdin Capital, Deerfield, Flagship, Forbion, Frazier, MPM, New Leaf Venture Partners, OrbiMed, Polaris Partners, RA Capital, Rock Springs Capital, SV Health Investors, Third Rock, Venrock, Versant Ventures

Generalist VCs: Alexandria Venture Investments, Canaan Partners, Fidelity, F-Prime Capital, Kleiner Perkins, New Enterprise Associates

Acknowledgement

We thank Thomas Uhler for his contributions at the initial stage of this project.

References

[1] Theoret, et al. “Expansion Cohorts in First-in-Human Solid Tumor Oncology Trials”. Clinical Cancer Research (2015) 21 (20): 4545–4551.

[2] FDA. “Expansion Cohorts: Use in First-in-Human Clinical Trials to Expedite Development of Oncology Drugs and Biologics certain

[3] See Appendix for list of “established” VCs