Summary

After challenging conditions in 2022, deal-driven biotech spending appears to have picked up in 2023. To quantify this trend we have systematically reviewed deals announced during this period and examined differences based on therapeutic areas and stage of development. We find that (1) deal counts shrank in oncology compensated by growth in other TAs; (2) the decrease in number of oncology deals was largely driven by less appetite for earlier phase assets, whereas compensated growth in other TAs came from the same earlier stages of development, (3) across the board, the average deal value went up principally driven by late phase assets. In sum, there is increasing willingness to pay for de-risked assets, along with shifts in TA focus for earlier stage programs.

A rebound in biotech deal making?

The general consensus on biotechnology industry funding after last month’s JPM conference was best characterized as cautious optimism. After record highs during 2021, the sector cooled considerably in 2022, but there were anecdotal signs of some recovery in 2023, notably large M&A deals including Pfizer-Seagen, Abbvie-Immunogen, and Abbvie-Cerevel. We were interested in looking beyond those handful of large deals, investigating if there were changes in overall deal activity in company M&A and product licensing between 2022 and 2023.

Beyond the 2022-2023 time frame, we limited our analysis to deals meeting the following criteria:

- The funding recipient (acquiree or licenser) is a US company (but the buyer could be based anywhere)

- The upfront cash value is at least $50M

- The risk-adjusted total deal value is at least $200M

- We excluded alternative listing mechanisms such as SPAC acquisitions and reverse mergers. We also excluded pure royalty financing deals.

In regard to the total deal value mentioned in criteria 3, we risk adjusted any contingent element (CVR, milestone-driven biobucks) based on the phase of the lead asset at the time of the deal, reflecting the historic probability of success of assets at that stage (Wong et al. 2019)

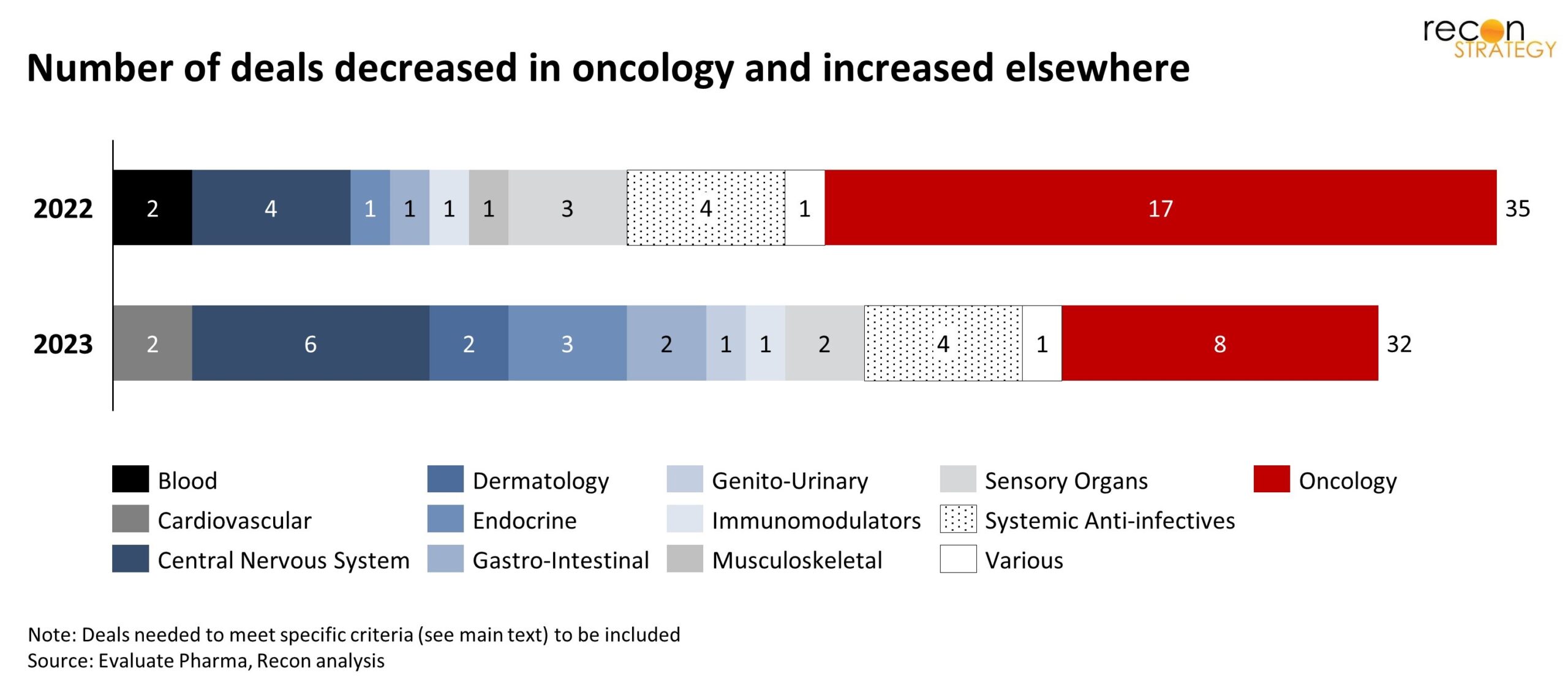

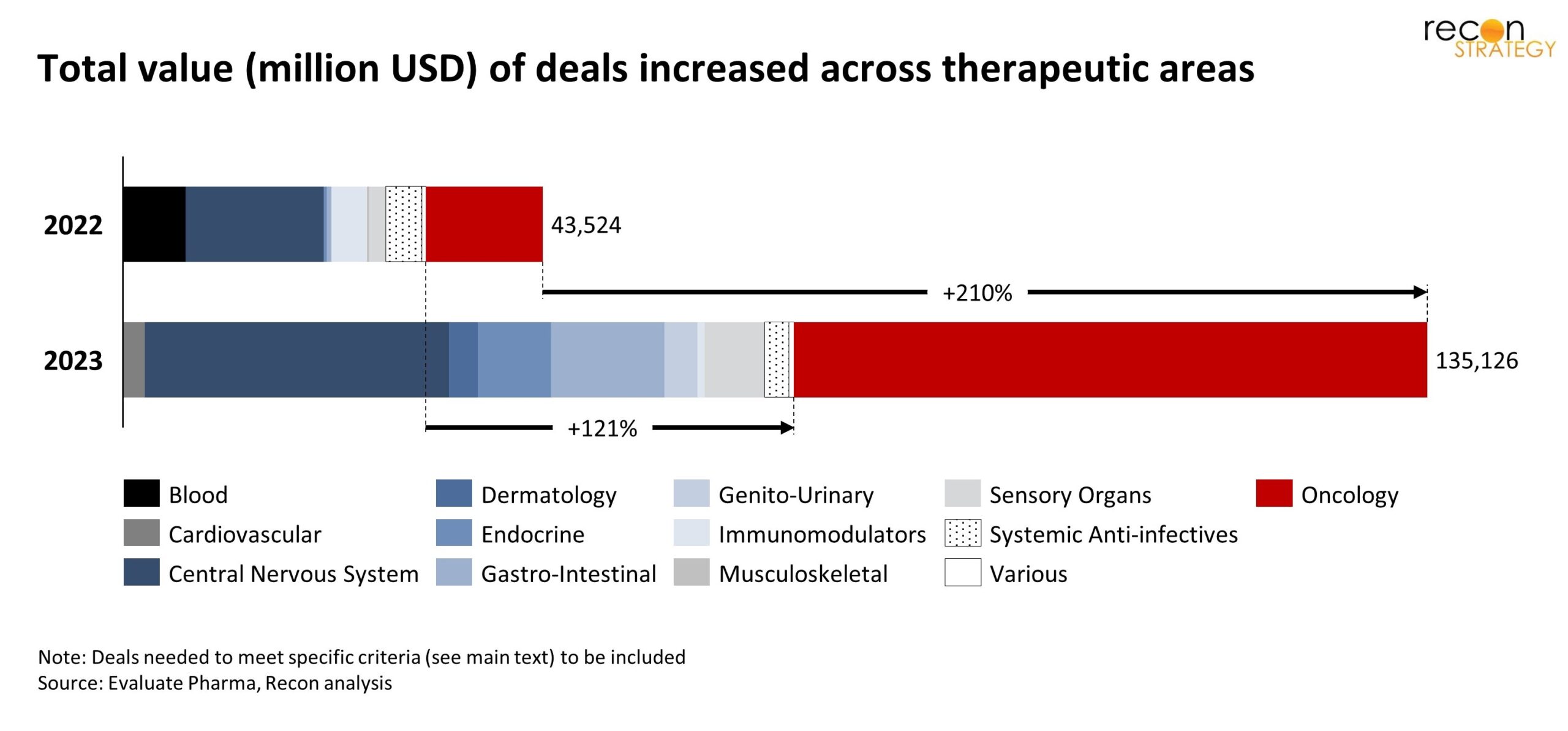

There were 35 deals in 2022 and 32 deals in 2023 meeting these criteria for a total value of $44B in 2022 and $135B in 2023 (Exhibits 1 and 3).

Deal counts trends diverged between oncology and all other TAs

Deal count was essentially flat between 2022 and 2023, but declined significantly in oncology with compensatory increases across the combination of non-oncology therapeutic areas (Exhibit 1).

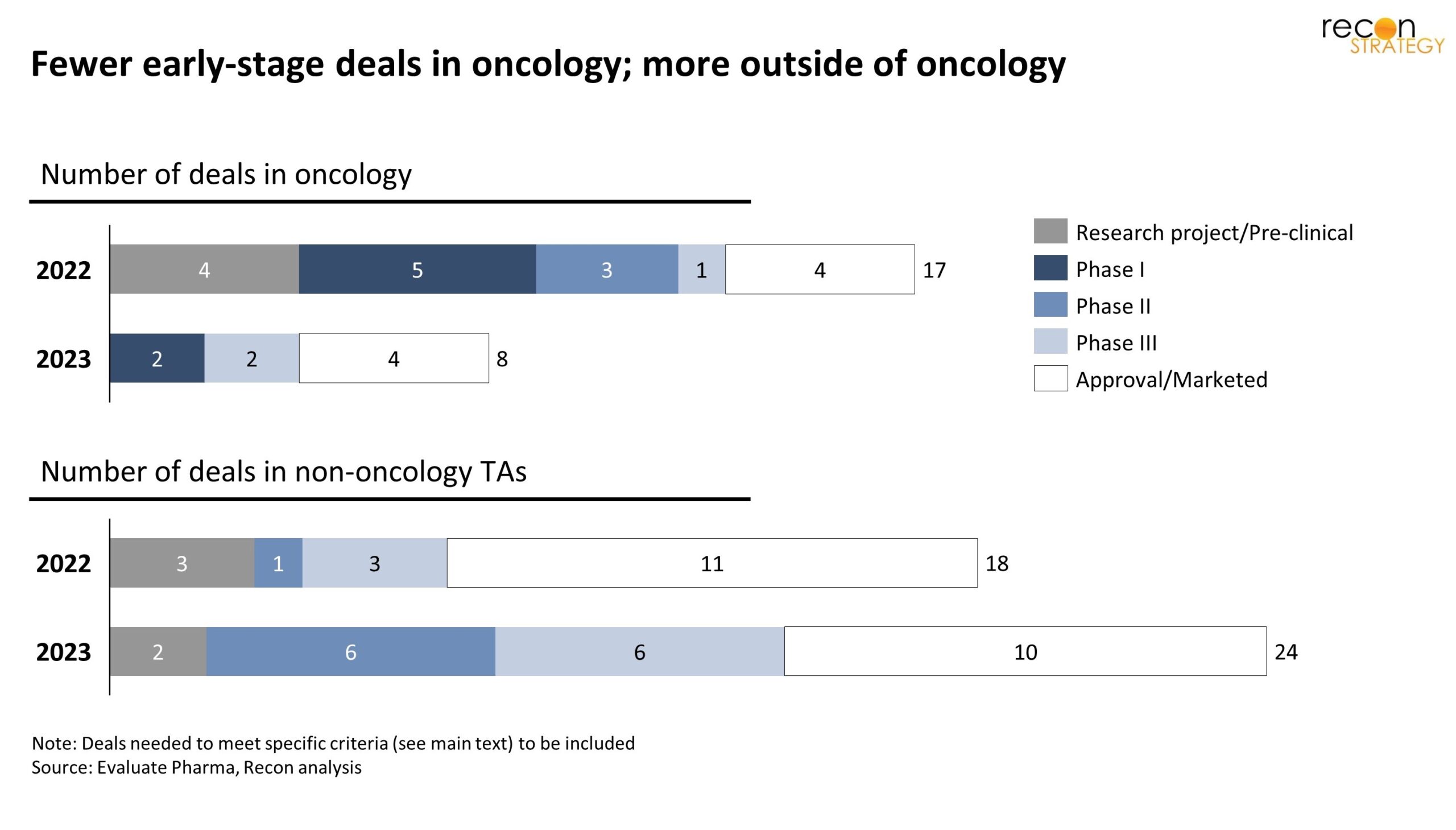

Interestingly, the decrease in oncology deals announced in 2023 can be specifically attributed to a decrease in the number of early-stage deals (Exhibit 2). In contrast, the increase in the total number of deals outside oncology is largely attributable to early-stage assets or pipelines.

In contrast to the deal count, there was significant growth in the average value of deals

Though the deal count was flat, total (risk-adjusted) value was multiplied more than 3x (Exhibit 3), which of course means that the average value per deal was much higher too.

At first glance, this appears to indicate that the value of oncology deals far outgrew other TAs in 2023, but the aforementioned acquisitions of Seagen and Immunogen accounted for $43 billion and $10.1 billion, respectively. Without these two large deals, the total value of oncology would be nearly unchanged (3% increase), but since the number of oncology deals dropped significantly, even without Seagen and Immunogen, the value per deal was significantly higher (+353%) in 2023.

There was also significant growth in non-oncology deals, both in total value and in average value, persisting even when removing one outlier (Cerevel’s acquisition).

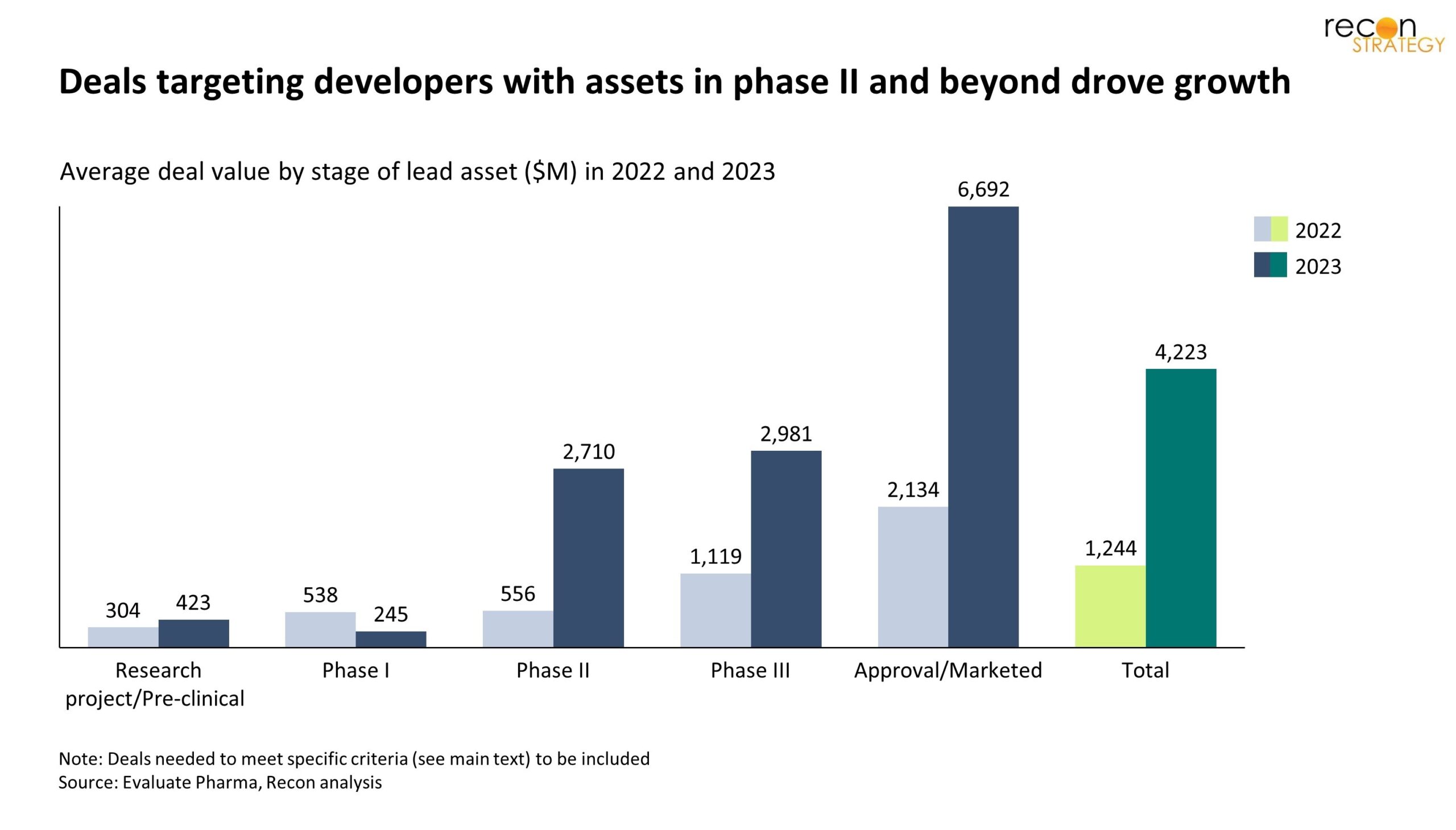

Analyzing the average deal value by stage of the key assets (Exhibit 4), investment in mid-to-late R&D and commercial stage companies drove most of the average deal value growth seen across the biotech sector. Note that the 2023 phase II average deal value was inflated by Cerevel’s $8.7 billion acquisition. Cerevel was an unusual case with a broad clinical pipeline, the M&A driver being emraclidine (phase II), but with four other assets across phases I-III. Excluding Cerevel, the average deal value for phase II assets in 2023 would still be $1.5 billion, marking a significant increase over 2022.

Final thoughts

Viewed through the lens of deal value rather than the number of deals announced, M&A and licensing trends appear to align with the cautiously optimistic sentiment about the biotechnology industry moving into 2024.

However, in oncology there was a notable shift away from early stage assets. In particular, after a period of enormous enthusiasm for immuno-oncology that fueled a wave of deals for ever earlier assets, 2023 suggested a shift towards fewer overall deals, but at the same time the willingness to pay for a de-risked asset(s) being much higher.

In other therapeutic areas, a slightly different story holds. Deals for early stage assets are growing, but at low average value (perhaps reflecting a bit of urgency from cash-constrained sellers). Mid-to-late stage deals increased in number and value, once again showing an increasing willingness to pay for de-risked goods.

Across the board, big pharma is shopping, but with an increased emphasis on filling out their later stage product line. Whether these trends are a one year phenomenon or beginning of a trend remains to be seen.