Summary

- Livongo is marrying a cellular-enabled glucometer and a data cloud with patient engagement services to help manage sugar levels

- Glucometer incumbents could match Livongo’s technology but will struggle to counter the business model innovation

- By expanding into services, however, Livongo is expanding its potential competitive set to include incumbent downstream care providers

- If Livongo’s model demonstrates compelling value, both device and services incumbents could find ways to stitch together competing solutions in collaborative ecosystems

- Closed loops are great ways to develop value propositions but can be rickety for trying to scale a solution in healthcare given the frictions which reimbursement introduces

* * *

Venture capital has bet over $80M on diabetes management start-up Livongo over the past two years with a $50M Series C closed this past April. The company is targeting a glucometer market dominated by four diagnostic/therapeutic heavy hitters (Johnson & Johnson, Abbott, Roche and Bayer/Ascensia) overseeing a sophisticated, well-reimbursed distribution chain. Even Sanofi (with their iBGStar glucometer) made little headway against the incumbent quartet. Two earlier glucometer start-ups (funded in 2010) have also seen limited progress. Why does venture capital think Livongo is going to succeed?

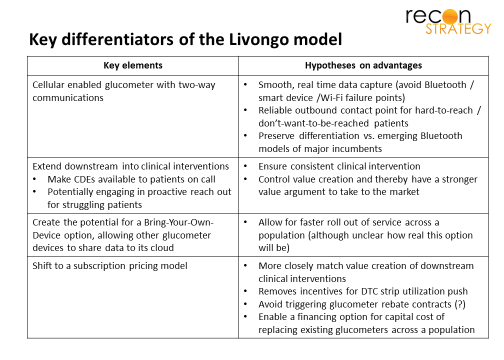

Livongo is exploiting the incumbent’s sleepy approach to wireless. The model eliminates barriers to consistent, timely and expert evaluation of glucose levels by creating a low latency closed loop. Its glucometer has built-in cellular connectivity to push readings out to cloud storage, algorithmic evaluation and further sharing. The cellular connectivity breaks the dependence on patient push and Wi-Fi availability to transmit to the cloud. In addition, Livongo has on-call certified diabetes educators (CDEs) to engage patients on their glucose levels by texting via the glucometer’s smart screen (or other channels if the patient offers them). The 2-way cellular connectivity ensures that CDEs can reliably reach patients via the glucometer smart screen. Initial outcomes results released this month suggest meaningful impact on HbA1c levels (down 0.7% on average).

![]()

What happened to the first wave of wireless start-ups?

Venture capital already backed two glucometer start-ups seeking to exploit wireless. Telcare makes a cellular-enabled glucometer uploading readings to a proprietary cloud (like Livongo). Glooko makes a cable to transmit data from a wide range of in-market glucometers to its cloud. Both companies provided basic trending analysis to patients (via a cloud-based e-logbook) as part of the package but stopped short of delivering live interventions themselves.

Their hope was that simple algorithm-driven feedback to the patient and easier data sharing with the provider (both enabled by the cloud) would create enough value to secure preferred position on the formularies for Telcare’s glucometer and reimbursement for Glooko’s dongle. While Telcare took the incumbents head on, Glooko assumed the incumbents would cede wireless connectivity to a “neutral” utility to avoid an arms race on wireless features. By 2014, neither Glooko nor Telcare had made much visible headway. Evidently, algorithm driven feedback did not create a strong enough value case to get preferred reimbursement. One can guess why: patients eager to adopt wireless were already actively engaged in their disease, reducing the potential to improve outcomes; unengaged patients, on the other hand, needed more than algorithm-based feedback to change behavior.

Provider interventions based on timely glucose data could make a big difference with these patients. However, providers do not decide which glucometer a patient gets, nor do patients (few “trade up” on glucometers). Instead, glucometer choice depends on which has first tier position in the formulary, thus varying by health plan and self-funded employer. Providers have to adopt clinical processes that work with any of them, so a patient providing a real-time electronic feed of glucose data will be treated largely the same as one with a desultorily maintained paper log. This is likely one reason why glucometer makers have been slow to push for wireless: because providers are unlikely to customize workflows around a single glucometer, there is little incentive to get too far ahead of competitors by investing in innovations that require clinicians to change their workflows. Nor did it help that few providers were taking risk at the time of Telcare and Glooko launches and therefore not compensated for the extra work that would have been involved in reviewing the low latency high frequency data.

Livongo’s approach incorporates downstream services

Livongo’s model has several differentiators (see exhibit below) centered on packaging downstream clinical interventions together with its glucometer.

By offering the closed loop, Livongo opens up value locked up by a reimbursement model that balkanizes glucometers across provider patient panels. The fixed costs of developing an intervention model using timely glucose data can be paid once and spread across all Livongo users rather than being duplicated across each provider system with the costs being spread out only over that fraction of the system’s patients who use Livongo glucometers.

Outcomes among provider patient panels are often skewed negatively by a subset of struggling; hard-to-reach/don’t want to be reached patients. For these patients, Livongo’s model seems particularly suited: the glucometer is going to be in a patient’s hands at ideal “teachable moments” (when they are testing) for the smart screen to offer outbound messaging from CDEs. Livongo could maintain a premium price point by focusing on these tougher cases (e.g., via a prior authorization process). Providers, increasingly at-risk for the outcomes on their panels and exasperated by unengaged patients would likely be happy to support a case for authorization (particularly because CDEs do not threaten to cannibalize their own professional fees).

Being a “last resort” glucometer for a subset of patients does not win you $80M in venture capital. Longer term, Livongo is likely planning to use beachheads among high risk, non-compliant patients to build a broader population health play. Such a move could create more value by carving out the service under a white label (and supplanting some care management programs which plans and risk-taking providers have in place) and handing off risk to Livongo. “After all,” the argument will go, “self-management habits are best set early in the course of the disease but we cannot identify non-compliant patients at the time of diagnosis. If Livongo’s model is effective with a subset of patients who have ‘tried-and-failed’ on traditional glucometers, imagine how effective it will be if we get all your patients from the start.” This could more effectively exploit the power of the outbound channel and any relationship the CDE’s develop while also allowing plans and providers to save costs by turning programs off. Livongo will (of course) want to swap out competing glucometers to ensure seamlessness, so the service would be more appealing to plans with highly sticky members (e.g. strong Medicare Advantage or commercial plans with high market share; note that the Humana – a Medicare Advantage specialist — and BCBSMA – a plan with a very high commercial market share — both invested in Livongo’s “C” round).

Competitive “judo” or just blazing a trail for others to follow?

If Livongo’s closed loop model becomes compelling to payers, the glucometer incumbents will struggle to parry on their own. Matching the connectivity technology will not be the problem (see exhibit), but integrating services would require a business model transformation. Vertical integrations are tough and the history of tech is filled with stories of manufacturers who have struggled for decades to expand into downstream services. Nice bit of competitive judo by Livongo!

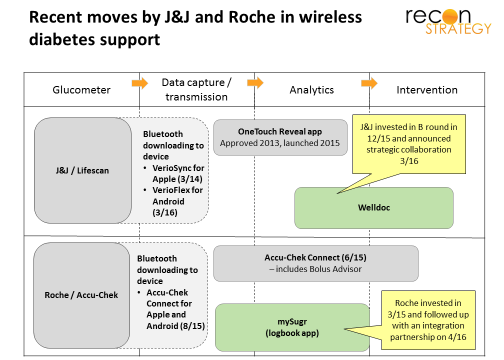

However, the glucometer incumbent would not need to do this on their own: they would just need to promote the growth of services players downstream from the hardware and data. Some diabetes intervention incumbents have already demonstrated interest in timely glucose data via one-off deals (Health Dialog struck a strategic alliance with Telcare at the end of 2013 and Joslin launched a partnership with Glooko on a “next generation diabetes management solution” in January 2014). Others ambitious, technology-oriented providers are expressing interest in getting into chronic care (such as Teladoc) and may be interested in wireless glucometry as a disruptive entry point. More interest could be stoked if data across a critical mass of glucometers could be made available — easily be done by a hub like Glooko, some interoperability collaboration or via a series of direct point-to-point interfaces with the handful of EHR vendors which matter.

Such a device/services ecosystem (similar to what we see for smart phones and mobile carriers) would have several advantages vs. Livongo’s closed loop:

- Function within the current reimbursement model (vs. having to adopt Livongo’s subscription pricing) thereby ensuring the support of channel incumbents

- Exploit the installed base of devices, scale, contracts and relationships of the incumbents on both sides of the device/services divide

- Potentially create better outcomes on services by incorporating more data streams (glucose remains one of many biometric/lifestyle measures relevant for managing diabetes and Livongo’s services will likely remain glucose-focused) and being better equipped to address comorbidities with which many high-risk diabetes are afflicted.

Sales cycles in healthcare are slow. Livongo’s business development operation is impressive (starting with forward-thinking large employers such as Iron Mountain, Lowes, and Office Depot; moving backward to channel partners with Mercer and Express Scripts; reeling in HUM and BCBSMA to close its C Round; interoperability with Cerner, etc.) but it still expects to have only 40K users by the end of 2016 per press reports. The incumbents will have a couple years before Livongo becomes a serious threat.

If the incumbents are able to put together such an ecosystem, Livongo could find itself facing the business end of some competitive judo: Its closed loop model would require it to pay for the R&D to stay competitive and the channels to reach buyers at every point in the loop. This competitive reality may force Livongo to open up its closed loop, make its vague “BYOD” promise a reality and transition its care management models to be device agnostic – in other words, eliminate its differentiation and leave its glucometer technology a stranded asset.

Aggressive business development is important, but Livongo would do well to lay the groundwork now for competitive advantage in an ecosystem end game (e.g. by locking in strategic alliances with major players further downstream). Otherwise, they may just end up blazing a trail that others actually exploit.