A number of observers have noted that the Apple’s partnership with Epic on HealthKit could reinforce the role of “closed IT system” strategies in general and Epic’s leading position among EMR vendors in particular. Others have noted that prominent PHR failures (Google, Revolution Health) should add some sobriety to the hype around HealthKit. While I don’t disagree with these concerns, I have three other thoughts on the announcement that Apple has built a framework for collecting and presenting health data from a wide variety of consumer devices and apps.

Providers making a play for the healthy?

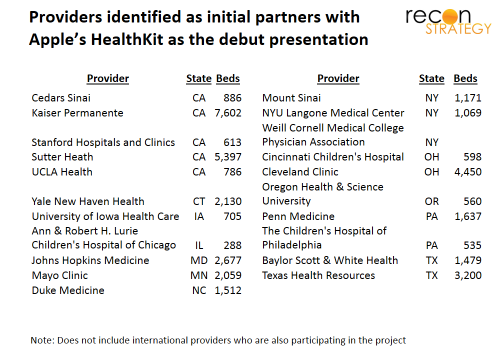

Apple’s focus on providers contrasts sharply with Samsung’s overtures to payers as partners in mobile health (note Samsung’s year-old strategic alliance with Cigna which is starting to bear fruit). Besides Mayo (which was intimately involved in the development of HealthKit and is staking out a position researching the value of mobile and apps), more than twenty provider systems have signed up as partners.

Yet there is no reimbursement model for physicians evaluating consumer-generated, wearable sensor-based biometric data. The clinical value of getting physician eyes on the data (in contrast, for example, to feeding the data back to the patient) is — with a few niche exceptions – undefined — the potential is there but years of research away. Finally, today, my guess is that the patients using wearable sensors today generally warrant less physician attention: they will skew younger, less risky and probably include a disproportionate share of the “compulsively healthy”.

Nor do I see how HealthKit will easily evolve beyond that healthy segment. HealthKit is designed to make data collection from a wide variety of consumer-selected devices easier. But what provider is going to rely on devices selected and maintained by the consumer for a high-stakes clinical decision for a high-risk patient? Who knows, after all, when the last time the consumer calibrated their device? I would expect physicians to require the use of devices they know and trust for the risky patients, devices for which no HealthKit is needed for integration into the provider workflow.

So why are the providers lining up with Apple?

It is not clear what having your logo show up on an Apple slide on HealthKit means–it might be quite a light commitment or part of a long-term clinical research agenda. If it is a meaningful partnership, could these providers be trying to attract these healthy consumers as patients via a wellness play? After all, consumers are being asked to make increasingly constrained choices about their providers (narrow networks, defined benefit, private exchanges, etc.). The healthy tend to have the least sticky relationship with providers, so are more willing to compromise on network for a lower premium. If HealthKit allows provider systems to build a relationship with these consumers (by, for example, having “conversations” regarding their peak heart beat rate during daily exercise – to start, it could be as simple as automated feedback in response to downloads or even just accepting the data into an EMR and recognizing it in the next standard office visit), the consumers will want those providers in-network. The fact that these patients belong in the fitness tracking portion of low-utilizers can even offer an arbitrage opportunity for risk-taking providers: risk adjustment algorithms can access no flag for the “obsessively healthy” and may well under-correct for the health status and behaviors.

It is no accident that the providers which have signed up (see Exhibit) are either deeply at risk (Kaiser) or tend to be top branded systems with expensive rates (Mayo, Johns Hopkins, Yale, Mount Sinai, Sutter for example). Also, if providers can figure out how to engage healthy consumers based on fitness, they will have a strong platform for pushing into wellness. And insurers could lose the wellness lever to differentiate themselves/add value and employers will have one more reason to work directly with providers on their insurance needs.

Closed systems can accelerate use case validation

Evaluation of consumer-generated biometric data is of uncertain clinical value and, I would guess, more about figuring out how to reinforce healthy behaviors than about identifying hidden ticking time bombs. Clearly there is a lot of research to be done. That is why, even if you are cautious about the broader impact of Epic’s “walled garden” strategy on innovation, there is a good reason to celebrate Epic’s involvement at this early stage of mobile health.

If we are going to prove out the value for clinical evaluation of patient-generated biometric data, we need to get it into clinicians’ hands and tie it with other clinical data. HealthKit will integrate and bring the consumer mobile device up to the front door of the EMR. But, after that, it is hard to predict where the data will need to go inside the provider system or with what other data, workflows it will need to be integrated. The cheaper we can move the data around to the right place inside the provider system, the broader the range of use cases which can be economically tested and the more robust the final set of use cases that get prioritized.

That’s where Epic’s superb “Epic-to-Epic” interoperability especially across the facilities/technical/physician divides can be a real advantage (“deepest data sharing of all EMR vendors” per KLAS). The providers who have signed up (with the notable exception of Mayo) are all on Epic. And Epic’s direct participation with Apple should make these interfaces even easier. Experimentation will be less costly. We can have more thorough investigation of a broader range of possible use cases.

While Epic and its customers may enjoy some first mover advantage, the many academic and publication-oriented providers are hardly going to keep the good use cases a secret. And reducing the uncertainty around the value at stake will make it easier for other EMR vendors and providers to invest in the requisite connections.

Getting to behavior change among consumers

Healthcare has never been very good at engaging consumers to be effective stewards of their health (either in the form of selecting healthy behaviors or in researching, identifying and using value-based healthcare providers). Convoluted economic incentives, deeply personal priorities and the sheer complexity of the data all stand in the way of this engagement. Even healthcare experts who recognize the need for greater paient-oriented transparency fail when they try put themselves in the mind of the consumer (see our view of Michael Porter and Tom Lee’s recommendations for metric “consumers care about” here). Apple’s brilliance at designing modalities and interfaces to dramatically change how consumers behave is well proven. Perhaps Apple’s commitment to healthcare may be just what is needed for getting real patient engagement in the longer haul.