Ezekiel Emanuel wrote an op-ed in the New York Times last month, which highlighted the low number of new antibiotics that have been brought to market in the past two decades. Antibiotics are a unique market compared to therapeutics for other diseases. Infectious disease clinicians prefer to use innovative new products as a last line of defense against highly resistant infections, relying on tried-and-true antibiotics as their primary options. Paradoxically, the “reward” for being a highly innovative, effective new antibiotic is to be sparsely used. Emanuel points out this conundrum while also highlighting the concurrent resistance to high prices, leading to an overall challenge in profitability for developing new antibiotics. As a solution he suggests prizes, upwards of $2 billion, to supplement expected revenues to create sufficient incentive for biopharmaceutical companies to focus their R&D expenditures on new antibiotics. Emanuel chooses the $2 billion figure based on the fact that average drug development costs exceed $1 billion, and he suggests a 100% ROI as sufficient incentive. This raises a more general question: does our health care system provide sufficient incentive generally for biopharmaceutical innovation? This post aims to explore this question by looking at profitability in biopharmaceuticals, biopharma’s returns compared to those of other industries and the recent history of R&D expenditures.

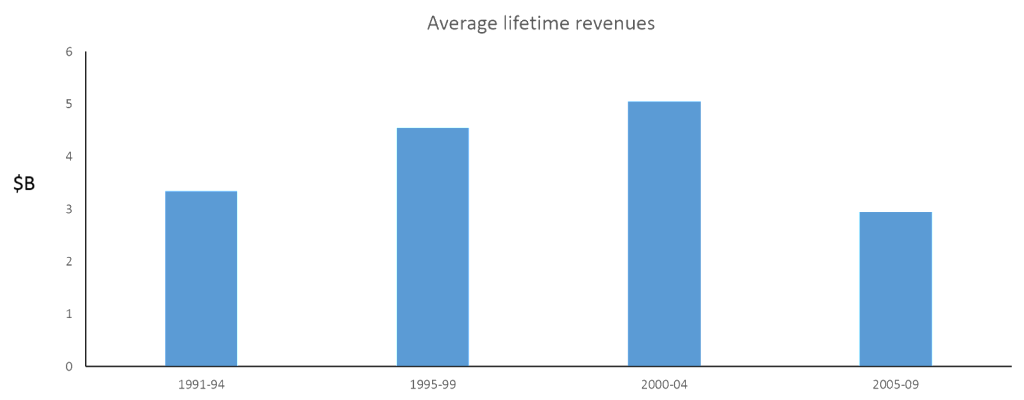

Health Affairs focused on biomedical innovation in its February 2015 issue. One article by Ernst Berndt et al, analyzed profitability for new prescription drugs over a 20 year period. His approach was to assess average revenues and costs for new prescription drugs, splitting the products into four time cohorts over the period of 1991 and 2009. Revenues grew initially, but declined by 43% between the final two time cohorts:

Bernt does not fully delineate the drivers of decline in the 2005-2009 cohort, and its worth noting that these lifetime revenue figures include estimates for future revenues, which could potentially understate future sales. He did offer some explanation. One of the modeled drivers is the expected impact from biosimilars, as the early biologics have been able to accrue monopoly profits beyond their exclusivity window with no competitors on market. Anecdotal evidence also supports the notion that the late 90’s and early 2000’s were they heyday for the industry: statins, SSRIs, TNF inhibitors were amongst the new classes of therapies that reached mega-blockbuster status. Fewer more recent drugs are expected to reach those heights.

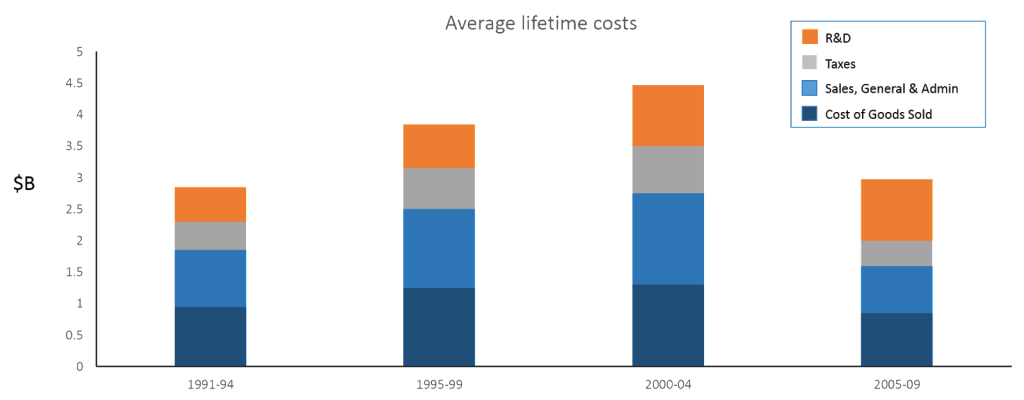

Bernt brought a different perspective on the cost side of the equation, which typically focuses on the average R&D cost to bring a new drug to market. He looked at lifetime total commercialization cost: R&D, sales COGS and taxes. General trends included growth in R&D expenditures over time, but initial growth and then reduction in costs for the others.

Taken together, the revenue and cost findings lead to a surprising conclusion: while profitability for new prescription drugs reached a peak in the late 90’s, the most recent therapies in the study are not expected to be profitable on average. It is possible that future expected revenues may decline less than projected by Bernt’s model, but the directionality of the trend is likely to problematic for the industry nonetheless.

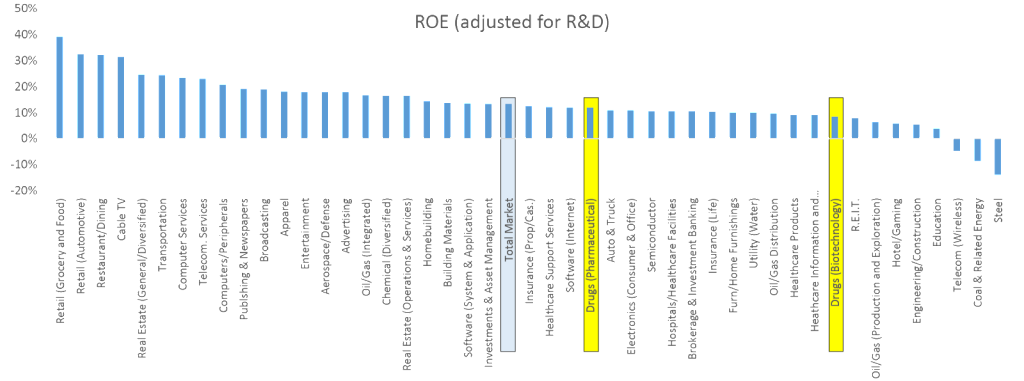

Research by NYU Finance Professor Aswath Damodaran provides a different approach to exploring the attractiveness of biopharma. Professor Damodaran maintains a database return on equity (ROE) rates across industry sectors, following more than public 4,000 companies in total. Using the data from his most recent dataset in January 2015, the biotech and pharmaceutical sectors look to have below average returns compared to the industry average.

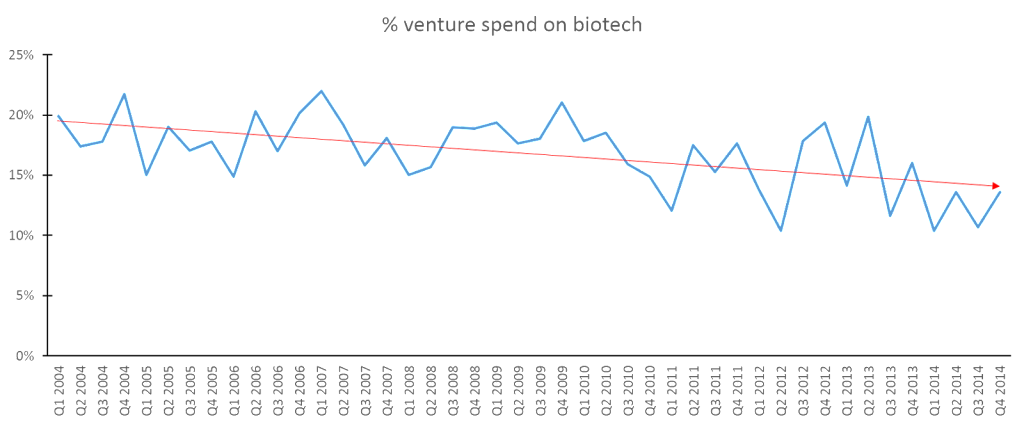

Given these findings, one would expect to find declining investment in biopharma compared to other industries. While the data is not strong, there are early signs that biopharma innovation may be beginning to stagnate. To assess new investments in biotech start-ups, we looked at data from the PWC Moneytree Report, which tracks venture capital on a quarterly basis across industries. In terms of absolute investment, both biotech and venture generally have increased recently. However, the relative interest in biotech has waned, as the proportion of venture investment targeted at biotech has slowly declined over the past decade. With the current cycle of overall start-up investments at a high, this phenomenon has not prevented funding of new biotechs, but it bears watching if fewer dollars are allocated to venture capital in the future and its resulting impact on this industry.

The much larger proportion of R&D investment is made by large biopharma companies, which is tracked by PhRMA on an annual basis. Over the past seven years, R&D expenditures has remained relatively constant, following a prior decade of robust growth. This pattern makes sense given Bernt’s findings: greater investment in the years following high profitability, little growth in the following years as profitability began to decline.

Looking at both the investment from large and small companies together, the data doesn’t demonstrate a precipitous drop in investment, but does provide early signs of stagnation and reallocation of capital towards other industries.

At the same time, payers across the globe are placing increasing pressure on pricing of new therapies. In his commentary in the same Health Affairs issue, University of California Berkeley professor James Robinson highlights that we are entering an emerging era where new therapies are reimbursed based on how much true innovation they deliver. The days where incremental improvements lead to billion-dollar revenue streams are increasingly in the past. Payers have begun to force steep discounts to provide access to these minimally differentiated products from their first-generation competitors. Importantly, he cautions that this system of paying for real innovation can only work if our health care system truly pays for innovation. The outrage that followed Gilead Sciences’ pricing of Sovaldi, should heed caution towards value-centric innovation. A ground-breaking therapy for Hepatitis C, Sovaldi has been found to be extraordinarily more effective than the existing standard-of-care, while also being highly cost-effective. While the course of therapy may be perceived as nominally steep, the value is fairly clear. These cost-effectiveness analyses don’t even consider the subsequent discounting that has ensued after Abbvie’s Viekra Pak entered as competition, which Gilead mentioned was an average 46% gross-to-net discount on its last quarterly earnings call.

The global evolution towards value-centric innovation is positive for stakeholders across the health-care industry: biopharma companies have clarity on the relative value of addressing high unmet need versus incremental improvements and can allocate resources accordingly; payers and governments have greater assurance that their budget is meaningfully improving patients’ lives; physicians and patients will have better tools to combat disease. Yet Robinson’s concerns about paying for actual innovation are an important factor. As Robinson writes, “if policy makers want breakthrough innovation, they will need to accept premium pricing.” Given the risk and development timelines, biopharmaceuticals should have a sufficiently attractive ROI or it may lead to relative underinvestment over time. In an industry where there are distinct winners and losers, the industry’s overall attractiveness can be obscured by the large profits of the few big winners. The aforementioned data on industry profitability, cross-industry returns and recent historical investment in biopharma R&D suggest that Robinson’s concerns are real. Just as Emanuel is concerned with sufficient incentives in the antibiotics space, we would benefit from ensuring that continued innovation is attractive for the biopharma industry as a whole.