Even as our priority today is dealing with the Covid crisis, healthcare organizations would do well to start thinking about the longer-term implications for their strategies. In some instances the marketplace will revert to the prior dynamic, but in many others the changes wrought during this crisis are likely to persist in a way that will call for new strategy or will produce unpredictable outcomes that will require scenario planning.

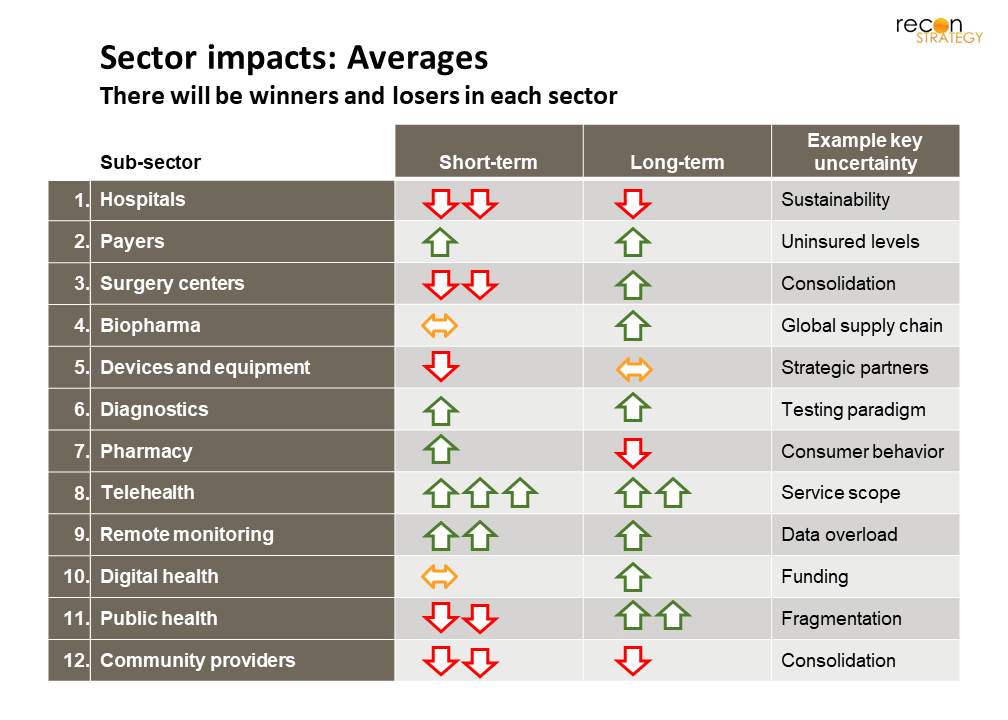

Sectors will be impacted in very different ways and there will be winners and losers in each. In this short post we draw attention to our quick takes on implications for players in each of the sectors over the next 2-3 years. We will update this as we learn more.

- Hospitals: The postponement of elective procedures will wreak havoc on hospital income statements and cash flow positions especially when you consider these in light of high costs as they deal with ramping up staffing and infrastructure to deal with Covid and their typically razor-thin margins. In the short term, survival of many will depend on how much they are paid by commercial and government payers for Covid care or what they get from a bailout. In the long term, even assuming policy makers, payers (particularly CMS), and the public are much more willing to invest in supporting hospitals after their heroic response to the crisis, there’s a lot of uncertainty on how that would translate in the real world with our mix of for profit, non-profit, and public facilities. There may be some future upside from their ability to acquire struggling independents but that may not be enough. No wonder then that the stock market has pummeled HCA and Tenet. Example strategy question: What are the possible scenarios and the implications of each on capital decisions (including shutting down services where needed), M&A and alliances, and upstream or downstream vertical integration.

- Payers: The part of the health sector that everyone loves to hate has responded with alacrity to the Covid situation (or at least many carriers have) using levers such as removing copays and deductibles, allowing early Rx refills, and lifting prior-auth requirements. They’ve also been promoting the use of telehealth, nurse care lines, and digital health solutions. They should also be thinking about the strategic importance of keeping providers sustainable. While some have suggested they pass on some of the premium dollar to make providers whole (assuming there is actually a surplus given that they have to pay for Covid care, mixed reads on this one) which raíses interesting legal and ethical questions around who health insurance premiums belong to once they are paid. We think this is an interesting idea that could be easier to do if you treat payments as advances against future services rather than just “the right thing to do”. Looking post Covid the big unknown is how many people will lose employer coverage and move to Medicaid, or the exchange, or drop out of coverage and whether employers on the cusp will shift back from self- to fully- insured. Example strategy question: What’s the future role of payers as the trusted partner for consumers and in sustaining sufficient provider capacity and competition?

- Surgery centers: Ambulatory Surgery Centers (ASCs) are severely affected during the crisis with shutdowns and postponements of elective procedures. Some have taken to furloughing workers and halting payments to physician owners. In some states they are being brought in either to take on procedures that would otherwise have been done in hospitals or to add bed capacity for Covid patients. After this crisis passes, there will be an opportunity for ASCs to thrive as patients will prefer staying away from hospitals for an increasing range of procedures and ASCs will have proved that they are safe locations for a broader range of procedures than currently allowed. Also with the recognition that they provide important surge capacity we could see some relaxation of regulatory barriers to expansion (e.g. lowering the bar on issuing a Certificate-of-Need). Some ambulatory services that are relatively rare in the U.S. such as birthing centers may also gain some footing, though we think the barriers to something like that are enormous. Example strategy question: What is the optimal path and logic to scale based on the drivers of value created by a corporate center both within and across specialties and how does that vary by location?

- Biopharma: Well-funded early stage biotech companies likely will have many of the same competitive dynamics though will be a renewed interest in finding ways to make certain areas more viable commercially such as infectious disease drugs, vaccines, and repurposing of existing drugs. It will be interesting to see what the impact will be on the FDA and their approach to prioritizing review or otherwise incentivizing these areas. Manufacturing and global supply chain resilience, already a complex question due to cross-border considerations such as tariffs, taxes, and pricing, become harder to optimize. If drugs and vaccines ultimately are what solve this problem for the world that would be a huge win for an industry that’s been heavily criticized for their pricing. You could also see regulators and payers making drug repurposing easier and more attractive. But in a 2-year timeframe there are challenges that mute these positives. There will be layoffs on the commercial side and some high-flying early stage companies will run out of cash. Many trials have paused or are slow to enroll. As timelines are hit, value is being lost (no COVID-related IP extensions coming their way!). Companies will be faced with imperfect data from Phase 1 and 2 trials to make their big investment decisions, and Phase 3 imperfections will have to be negotiated with regulators. A silver lining is that we’ll see many more processes digitized across the R&D to commercial value-chain such as virtual / remote clinical trials and more e-detailing. Example strategy question for early stage biotech: What are the critical choices that we made previously such as focus areas, targets, assets etc. need to change because our assumptions on the regulatory and market environment are no longer what they were?

- Devices and equipment: Reduction in elective procedures is a shock to the sector (witness Boston Scientific cutting pay, though an obvious exception is manufacturers of equipment used in Covid care e.g. ResMed) though much of the demand should bounce back relatively quickly and there may even be some pent up demand (that knee still has to be replaced). Longer term expect to see this sector return faster than other sectors to its prior competitive dynamic. On the startup side we don’t see as much of an impact as in biotech as a lot of the engineering work has been able to continue. What remains to be seen is whether or not there’s some reduction of support particularly from strategic partners. Example strategy question for an early stage device company: What are the risks to our funding and other support from our large device company partners and what do we need to do to mitigate them?

- Diagnostics: Short term impact varies even across larger players with some benefiting (Abbott, for instance, though was this a missed opportunity on the service side for Quest?). Longer term expect an evolution toward a combination of broader -omic and biome testing and a real-time system that is less tied to traditional care delivery. This could include more home testing and increasing consumerism (which ties in to home monitoring and telehealth). Example strategy question: What is the future paradigm of diagnostic testing and what should we be doing to shape it to our advantage?

- Pharmacy: Pharmacies have remained central to American’s day-to-day lives despite a long push by payers to get people to shift to mail order delivery for prescriptions. Like other sectors they’ve performed heroically during this time ramping up rapidly. Longer term though, just like with people trying out telehealth, this may be a moment where more people try mail delivery and then stick with it. The short term surge buying of vitamins and cold medicines will not last long. That said, CVS (with Caremark and Aetna) is better positioned to retain advantage long term. Example strategy question: If there is a step shift towards mail order, what will that mean for retail pharmacies especially in light of a continuing pressure on dispensing charges?

- Telehealth: The most obvious beneficiary with exploding interest during the crisis as even providers who previously may have been wary of using it have had little choice but to try it out and having used it are realizing it’s not so bad after all. Look for growth in telehealth not just in urgent care and mental health but more broadly in primary care, maternity and many office-based specialties. Example strategy question: Should we be a platform for providers and health systems or should we be the provider ourselves?

- Remote monitoring: A counterpart and extender of telehealth (some include it in the same category) is also an undeniable gainer though we expect some consolidation as weaker players run out of cash and winning technologies are acquired. Enabled by technology and consumer-friendly solutions, we will see accelerated adoption where it already exists and the introduction of new measures. Related to this will be the need to integrate and use the data from all these devices in a way that does not overwhelm the patient and the care-delivery system. Example strategy question: Should we take a shot at being the leading player (though risk losing it all if our advantage is not sustainable) or should we join hands (partner, sell to a strategic, etc.) to increase the chance of success (for a share of the spoils)?

- Digital health: (aside from remote monitoring and telehealth which some include in this broad bucket) Covid response leading to a few big winners but also serious winnowing of the competitive landscape. Adoption of AI will only increase in areas such as pathology and radiology as well as for differential diagnoses (look at Buoy Health’s emergence during this crisis). We expect well-equipped analytics companies and digital workflow companies to find tremendous opportunities serving all of the stakeholders. Example strategy question: What are the emerging hospital use-cases for digital products and services and what’s the best way to position your product to be the category killer in its space?

- Public health: The debate on the trade-off between our ability to harness the enormous value of large datasets and our desire to protect our privacy has come to the fore. We expect that there will be a somewhat greater willingness to allow more disease surveillance in some ways that will be more visible to the public, and others that will be less visible. There is the potential for this to enable life sciences research and improve early warning systems and population health management. While in the short term public health that’s not Covid related will suffer, in the long term expect there to be much more appetite from the public and governments to fund public health. Example strategy question: What assets, capabilities, partnerships, and more will organizations need to deliver public health value from integrating data across multiple sources?

- Community providers: Independent physicians and other providers who are not engaged in Covid care are in limbo. Many offices are closed or functioning at a low capacity with many lacking sufficient telehealth capabilities. Some larger groups that participate in physician owned ACOs could see impact extend well beyond this year as the consequences of missed preventive care during this period will play out in the months ahead. These and other factors could push groups, especially the remaining smaller offices into the arms of health systems or larger entities such as Optum Care. Example strategy question for a multi-specialty group: What are the optimal strategic options under different scenarios playing out and what are the conditions under which we should be ready to pull the trigger?