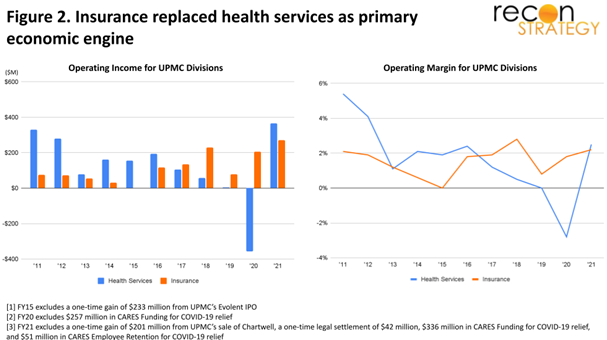

UPMC’s decoupling from Highmark exposed a critical vulnerability: economic dependence on its Allegheny County hospitals. In FY11-12,[1] these hospitals provided 70% of UPMC’s overall operating margin, an average of ~$270M annually.[2] A few years later, these operating margins had been cut in half and, by FY19, these same hospitals could contribute just $9M to the enterprise.[3]

How did this happen?

The Highmark dispute created severe economic headwinds for its western Pennsylvania (what we call “Core”)[4] hospitals:

- Decay in payer mix. As Highmark patients went elsewhere, the overall commercial share of UPMC care delivery went from 37% in FY11 to 27% in FY19.[5] Volume from UPMC insurance grew (from 14% of care delivery revenues in FY11 to a peak of 22% in FY17) but not enough to backfill for Highmark. That volume was also a mix of commercial and more heavily discounted government programs. Unsurprisingly, the average discount off of gross charges went from 73% in FY11 to almost 80% by FY19.

- Shift in service mix stranding capacity. Volume in UPMC’s Core hospitals shifted away from I/P (discharges fell 11%) towards O/P (visits grew 27%) between FY11-19. While O/P care can be highly profitable, the large reduction in admissions would have left a lot of expensive facilities, equipment, and people underutilized.[6]

- Overhead costs growing faster than revenues. In part because UPMC retained much of its underutilized bed capacity, overhead costs went from 17% to 24% of revenues over the same timeframe, cutting seven percentage points from potential profit.

To find a way out of this box, UPMC would need to create reliable new profit engines.

Remarkably, UPMC was able to construct two such engines in just a few years after the Highmark decoupling thanks to the flexibility of a vertical model (combining payer and provider) and aggressive geographic expansion.

Insurance profits backfill for care delivery

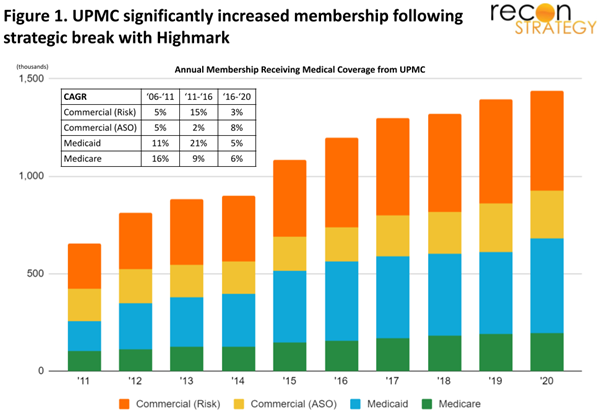

The first new engine was an expanded insurance division.

Historically, UPMC’s insurance division has provided, at best, a supplement to UPMC’s overall profit, contributing an average $74M per year between FY11-12 or about 20% of overall operating income.

Starting in FY12, however, UPMC significantly increased its insurance membership (from 8% CAGR in the five years prior to FY11 to an average of 13% per year in the five years following FY11). This growth was led in particular by a doubling in membership in its commercial risk line of business in the five years after the Highmark decoupling.[7]

UPMC recognized the opportunity to exploit the uncertainty of access to its highly branded clinical assets: once the dispute broke open, Highmark could no longer ensure that its members could receive the highest ranked care delivery in western Pennsylvania. UPMC insurance, on the other hand, could offer that certainty.[8]

Membership growth was more modest after FY16 (averaging ~6% CAGR), but, by then, UPMC insurance had already grown to more than one million members. Premium revenues would approach those of care delivery but with a steadier margin (particularly after FY15-16).

As a result, the relative profit contribution of UPMC’s care delivery versus its insurance division flipped: while care delivery contributed the majority (81%) of overall UPMC profit between FY11-15 (an average of $200M per year), insurance contributed the majority (61%) between FY16-19 (an average of $140M per year).

Profits in new eastern hospitals replace declining hospitals profits in the West

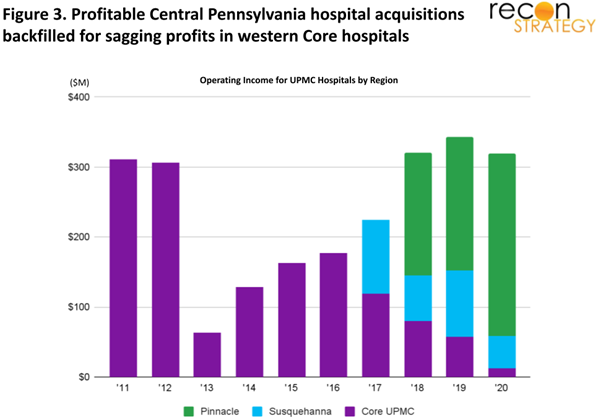

UPMC created a second new profit engine through the acquisition of hospital systems in northern and central Pennsylvania in FY17-18.

These systems—Susquehanna in northern Pennsylvania and Pinnacle in the Capital district[9]—enjoyed significantly higher average margins versus the legacy Core even before the Highmark decoupling.[10] In FY10, Susquehanna and Pinnacle hospitals yielded an average combined margin of 13% versus the 5% margin in core UPMC hospitals. Pinnacle and Susquehanna then improved their margins in the five years before their acquisitions to an average 16%, while margins in Core UPMC had slipped to 3%.[11] In particular, Pinnacle had 80% less total revenues than Core UPMC hospitals between FY13-17 yet saw an average of 20% more income each year.

Because these systems were largely untouched by the Highmark dispute, they were able to maintain their high margins after their acquisition by UPMC. Despite smaller revenue bases, their operating profits were sufficient to backfill for the declining profits from the Core hospitals[12] and bring annual hospital profitability back up to the $300M levels.[13]

Impact

While profits from its Allegheny County hospitals dissipated, UPMC was able to grow its insurance business to backfill for care delivery and acquire new systems that could backfill for declining legacy Core hospitals. These new profit engines not only sustained the enterprise, but they also enabled UPMC to continue investing in new and improved facilities, tightening physician affiliations, and expanding clinic networks across both its legacy western and newly acquired eastern Pennsylvania markets (for more detail on these investments, see our research report link below). Early data from FY21 suggests that this is already starting to pay off, as overall care delivery profits have returned to FY11 levels (even after adjusting for one-time Covid payouts).

With the announcement of the ten-year network deal with Highmark in June 2019, the headwinds for the western Pennsylvania care delivery operations should be largely alleviated. There was a quick increase of Highmark’s share of UPMC’s FY20 care delivery volume. Longer term, it is likely that the overall commercial share of UPMC’s payer mix will increase in its Core hospitals and assist a return to higher bed occupancy levels.

Thus, UPMC has not only weathered the economic headwinds of the Highmark decoupling; it can now expect its Core hospitals to become profitable once again. UPMC enters the 2020s not with one profit engine, but with three—its western Pennsylvania hospitals, its eastern Pennsylvania hospitals, and its scaled insurance business.

The UPMC case demonstrates the strategic robustness enabled by combining a vertical business model with a willingness to expand geographically. Other delivery systems—particularly those with nascent insurance operations—are no doubt taking note.

To read more about the evolution of UPMC’s economics from 2016 to 2021, view the full report:

Evolution of UPMC Economics 2016 – 2021

[1] This analysis uses fiscal years ending June 30th. UPMC originally reported its data in fiscal years, although it has since changed to calendar year reporting. We used quarterly data to reconstruct fiscal years and enable a consistent time series.

[2] From FY11-12, UPMC’s Allegheny hospitals contributed a total of $545M out of $610M in aggregate care delivery income and $757M in total UPMC enterprise income.

[3] Volume and financial data for UPMC’s Pennsylvania hospitals are sourced from the Pennsylvania Healthcare Cost Containment Council (PHC4) and CMS’s Medicare Cost Report (Hospital 2552-2010 form). Aggregate-level volume and financial data for the UPMC system is derived from revenue bond offering disclosures on MSRB’s Electronic Municipal Market Access (EMMA). Hospital-level financials are reconciled with the aggregate-level data in order to pull apart the various economic components of UPMC’s overall performance.

[4] We define UPMC’s “Core” hospitals as all western Pennsylvania hospitals they owned before FY16—primarily consisting of its flagships in Allegheny County, but also its smaller hospitals in neighboring Bedford, Mercer, and Venango Counties, as well as its nearby acquisition hospitals in Blair and Erie Counties.

[5] Measured as the share of gross charges which we assume will have similar price weights across coverage types.

[6] UPMC did not fully restructure its capacity accordingly, reducing staff beds in the Core by 3.5% between FY15-20—much less than the corresponding decline in admissions over the same timeframe. As a result, occupancy went from 70% in FY11 to 67% in FY15 and 63% in FY20.

[7] Commercial risk membership went from 231K in FY11 to 459K in FY16—an increase from the average ~5% membership CAGR in the five years prior to the break with Highmark to an average 15% per year in the five years afterward.

[8] UPMC was also able to roughly double the growth rates of its Medicaid membership. This line of business grew an average of 11% CAGR in the five years prior to FY11 but reached 21% in the five years after the FY11 break with Highmark.

[9] In both cases, the original non-profit delivery systems acquired additional hospitals from nearby for-profit players (Lock Haven and Sunbury hospitals from Quorum for Susquehanna and Carlisle, Lancaster Regional, Heart of Lancaster (Lititz), and Memorial hospitals from CHS for Pinnacle) before being integrated into UPMC.

[10] We refer to Susquehanna and Pinnacle hospitals as the combination of both their legacy hospitals and those that they acquired from Quorum and Community, respectively. Pinnacle also includes one non-Community acquisition hospital (Hanover) that was brought on shortly after the deal with Community.

[11] Between FY12-16, Susquehanna hospitals earned $201M in operating income and had $2,133M in total operating revenues. Between FY13-17, Pinnacle hospitals earned $1,220M in operating income and had $6,841M in total operating revenues. Between FY12-17, Core UPMC hospitals earned $952M in operating income and had $33,778M in total operating revenues.

[12] Hospital-level financial data is not yet publicly available for FY21. As such, we are unable to disaggregate health services income between hospitals and non-hospital care delivery for this year.

[13] Note that restoring hospital operating profit was insufficient to avoid a significant decline in overall care delivery profitability between FY16-20 (see Figure 2). The difference between overall care delivery and Pennsylvania hospital operations should primarily be clinics and physician costs (though it will also include a few small hospitals outside of Pennsylvania). UPMC undertook major investments in growing affiliations and care delivery points which likely contributed to operating cost. Had the new acquisitions not contributed to hospital profits to net out versus these losses, however, overall care delivery would have operated at a substantial loss throughout FY17-19 instead of being somewhat profitable.