There’s a major disruption looming in how the site-of-care for infusions is managed which will have repercussions for plan competition, delivery system economics, PE hunting for healthcare opportunity and biopharma commercialization strategy.

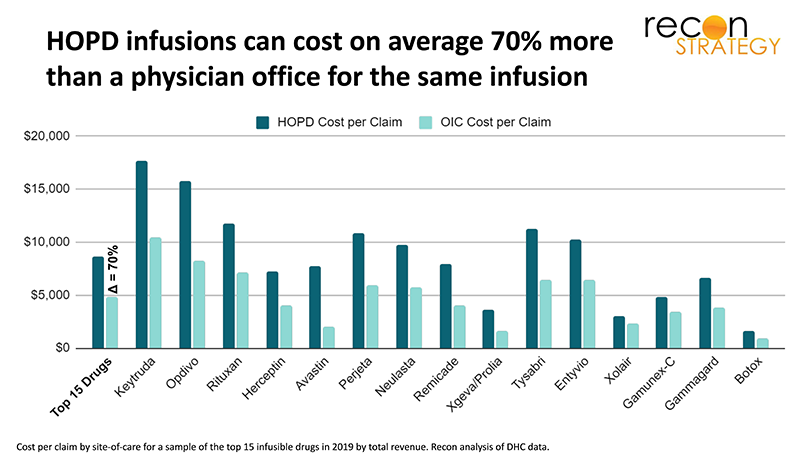

Plans have long been frustrated by the growth of infusion care in expensive hospital outpatient department (HOPD) settings. HOPD infusion services can cost health plans on average 70% more than a physician office for the same infusion. But because patients on infusion therapy are often very sick and the therapies hard to tolerate, plans have historically been reluctant to intervene on site of care.

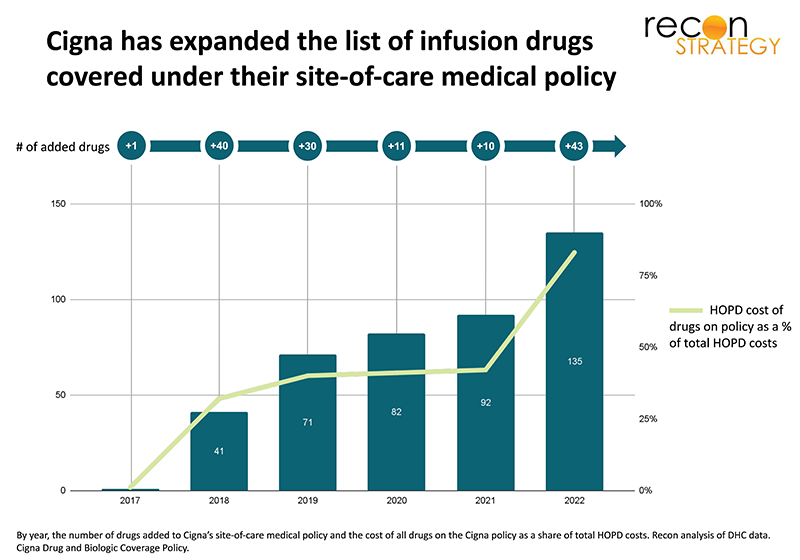

Over the last several years, however, the context for infusion management has changed. Specialty medications have become a more visible cost trend driver. Employers—having exhausted the possibilities of employee cost sharing—are embracing stronger care interventions, and recent M&A driven consolidation of medical and pharmacy benefits management have combined the intervention levers and accountability in one set of hands. This view of the list of infusion drugs (including many oncology drugs) for which Cigna has set site of care medical necessity criteria exemplifies the breadth and pace of change in health plan approaches:

As competitive pressures push more plans to replicate Cigna’s approach (as many nationals are already doing), there will be a major disruption in the HOPD infusion services business.

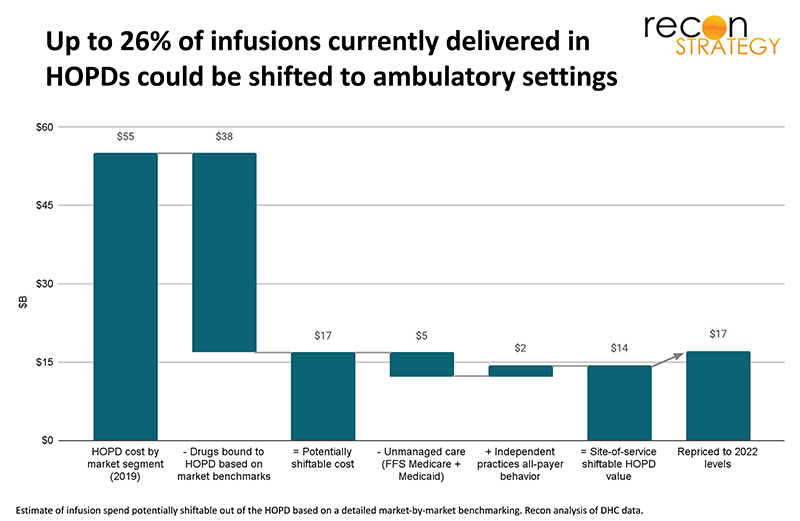

The ultimate floor for HOPD share of infusions is not a simple function of plan policies. Practical factors will degrade the yield—lingering sensitivities regarding oncology, differential impact of patient demographics and social determinants of health barriers, and profitability of infusing drugs in an ambulatory setting. Based on a detailed market-by-market benchmarking of actual infusion practice to incorporate these constraints, we estimate that up to 26% of infusion care currently delivered in the hospital outpatient department could be shifted to ambulatory settings, a total of $17B in 2022 infusion spend.

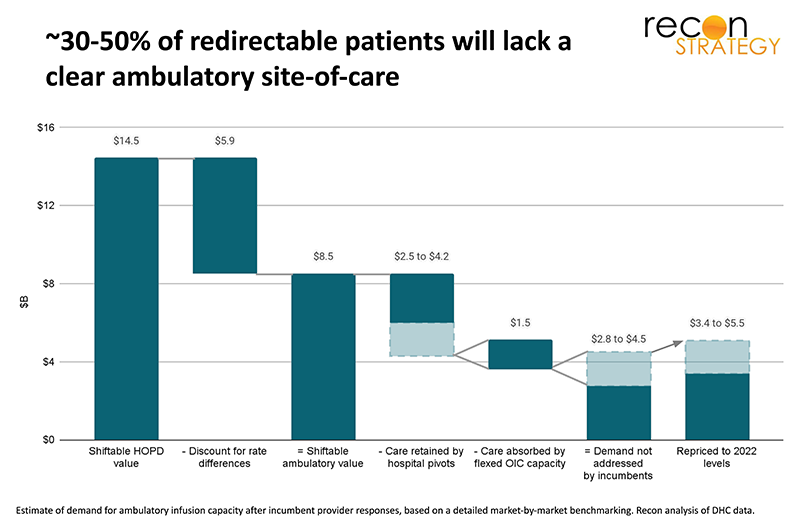

Where will this infusion demand go? Based on a series of market interviews, we believe about 30% to 50% of this redirection will be retained by integrated delivery systems which have largely aligned prescribing physicians, giving them an edge in holding onto the infusions. Notably, we do not expect all of these systems to keep the infusion in their HOPDs but in many cases to “pivot” by building ambulatory infusion sites integrated into their system (we talked to several systems which have such efforts underway). We also expect more independent physicians to expand in-office infusion care, absorbing about 20% of the redirected care. For the remainder, underlying patient risk likely disqualifies most patients currently getting infusions at hospital outpatient departments for redirection to home therapy.

That leaves the remaining 30% to 50% of infusions redirected out of the hospital (an estimated total of $3.4 to $5.5B in 2022 infusion spend once repriced to ambulatory rates) but without a clear ambulatory site-of-care as of today.

Meeting this demand is an opportunity for new entrants—whether private equity backed pure-plays or incumbents with existing distributed clinical networks that can add a new line of business.

For a more detailed review of our results, read our new white paper:

The coming infusion site-of-care shock: strategies, outcomes and opportunities

Jacob Wiesenthal

Associate Consultant

Tory Wolff

Managing Partner