There isn’t a bricks-and-mortar primary care acquisition out there that is beyond Amazon’s financial reach. While the announcement regarding One Medical has provoked fresh rounds of speculation about what Amazon might do broadly in primary care (e.g., push Pillpack),[1] our interest here is in why Amazon seems to think One Medical specifically is the right move right now. Below are some quick thoughts:

Compatible business models

One Medical’s legacy commercial business and Amazon (Prime) both operate a fixed annual membership fee plus charge-per-transaction business model. The membership fee provides customers with premium service, an annuity to the business and a consolidation of relevant transactions.

There are some differences of course: Amazon’s vast product and service scope makes the spend consolidation opportunity enabled by Prime especially attractive. There is only so much primary care activity most commercial patients need, however, so for One Medical, the opportunity is more around consolidating a slice of patients willing to pay a premium for access to healthcare and figuring out how to leverage them (e.g. through “rate borrowing” via strategic partnerships with branded delivery systems – see below).

Even so, however, the core business model compatibility makes exploration of potential synergies easier (e.g. bundled Prime/One Medical membership fees).

Direct-to-employer momentum

Amazon’s current virtual care offering has not gotten much traction outside its own employees and subsidiaries (e.g. Whole Foods).[2] It is early days but benefits consultants and CHROs can be cautious with vendors who lack a substantial track record.

One Medical, on the other hand, has a large base of employer clients (including some very big brands like Google).[3] The company has been attracting a lot of patients covered by enterprise relationships (35% CAGR in the most recent full year) and reached material scale (~425K patients among enterprise clients as of end of 2021).

Amazon could leverage One Medical’s inventory of direct-to-employer and benefit consultant relationships to sell additional health services (Amazon Care if the brand is retained, Pillpack etc) to both current One Medical clients and new customers.

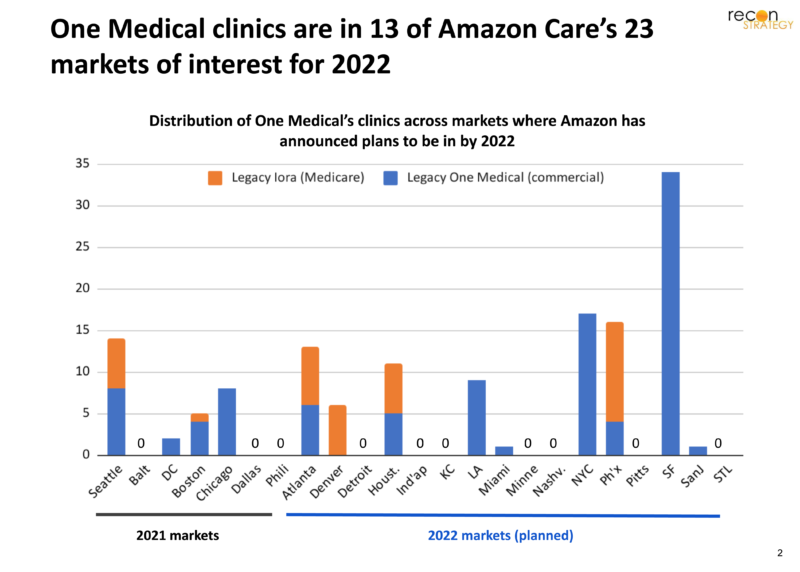

Quick path to hybridization of Amazon Care

To date, Amazon Care has largely been pitching employers a virtual-first care model (with optional @home enhancement via visiting nurses) across 23 geographies by 2022.[4] With people reverting back to clinics for ambulatory care, however, hybrid care (virtual and/or in-person depending on patient preference)[5] is becoming table stakes and the “as-is” Amazon Care model out of date.

One Medical has 137 of its clinics[6] located in 13 of Amazon Care’s markets of interest (which collectively represent 72% of the population in Amazon’s 23 stated markets of interest).[7] These offices can be quickly integrated into Amazon Care to provide a hybrid option. See below:

Partnership template for downstream care

In most of its markets, One Medical has built strategic partnerships with big systems. These models typically involve:

- One Medical joining a clinically integrated network with the system

- PMPM payments from the system partner to One Medical for the attributed patients

- Ceding of all billing revenue for the care delivery by One Medical to the system partner on the system’s contracts

Preferential referrals for specialty care within the clinically integrated network are also likely an important part of the model. The partners are impressive, often the leading academic system in their markets.[8] And the business model appears to be working, with revenues growing at 100%+ CAGR between 2018 and 2021, more than double One Medical’s overall revenues (43% CAGR since 2018).[9]

Amazon Care could be integrated into these partnerships as well in multiple ways – for specialty consults, as preferred downstream care partners or even into the One Medical clinically integrated network model (these systems may have more success negotiating virtual care rates than Amazon Care would as a stand-alone).

There may also be a business model opportunity here. These partnerships may also facilitate plan contracting. Reportedly, Amazon has been having trouble contracting with health plans because it has preferred a population/performance-based reimbursement model[10] while plans apparently sought more traditional claims-based models (suggesting some skepticism about Amazon’s ability to deliver on that performance and a desire to retain an apples-to-apples basis of comparison vs. other providers). One Medical’s strategic partnerships might allow Amazon to sidestep plan preferences, get its preferred population-based pricing model while “offloading” contracting with plans with more traditional structures onto its strategic partners.

Platform to test potential bricks-and-mortar bundles

One Medical’s clinic network is tightly co-located with the Whole Foods store fleet. The analysis below looks at the distance from One Medical commercial clinics (= legacy One Medical, not including legacy Iora clinics) to the nearest Whole Foods store:

Given that Whole Foods employees have access to Amazon Care as a benefit, there may be some immediate patient acquisition synergies for One Medical. These will be marginal, however. Retail front-line workers are not the typical patient for which One Medical was designed. Further, the overlap goes only one way: while the entire One Medical commercial clinic network is within 10 miles of a Whole Foods store, only 42% of Whole Foods stores are less than 10 miles from a One Medical commercial clinic.[11]

More generally, however, the tight geographic overlap between One Medical and Whole Foods does suggest that both brands are typically targeting the same consumer demographics (high disposable income) with the same shopping patterns (a premium/destination consumer experience). Having One Medical inhouse creates a ready-made platform for experimentation on value propositions and business models which can then be rolled out in the rest of Whole Foods geographies (e.g. Prime bundles).

Why did CVS walk away?

News reports have suggested that CVS put One Medical in play. Yet they walked away. Analysts have reasoned that CVS wants primary care to be accretive quickly while One Medical still needs a couple years to get to profitability. But CVS would have known One Medical’s profit trajectory before initiating the conversations. The discussions must have broken down for other reasons.

Two thoughts here:

CVS does not need some of the One Medical assets we think Amazon would find valuable (specifically: relationships with employers and benefits consultants, a distributed “real world” clinic option to support a hybridized care and existing payer contracts). So it would make sense that Amazon would be willing to pay more than CVS.

CVS should have been willing to pay a premium for a care model actually delivering on value-based care, while Amazon – more interested in transactions juiced with a layer of Prime-like premium fees for premium service – would not. We have had our suspicions that One Medical lacks an ability to bend the cost curve based on the uncompelling evidence publicly available.[12] CVS walking away after looking under the hood suggests those suspicions are warranted.

Thomas Uhler

Consultant

Tory Wolff

Managing Partner

[1] See our own “big think” view of what Amazon might do in healthcare (albeit back in the days of Haven) here.

[2] Publicized names include Hilton with ~60K employees in the US and several smaller companies (e.g., TrueBlue with ~6K employees, Silicon Lab with 2K employees, and Precor with ~1K).

[3] Reportedly 8.5K employers though this includes a long tail of very small companies since this would imply that the average account has only ~100-150 employees eligible for the service.

[4] We are relying on a broker presentation which Business Insider reported on in February, 2022 but which may date from 2021. Markets of interest are ones where, according to the presentation, Amazon Care already had services in 2021, planned them for 2021 or planned them for 2022, a total of 23 markets.

[5] And, increasingly, provider care protocols as they redesign care models.

[6] Figure should be regarded as approximate and based on public data on the clinic network. It may not reflect recent openings or closures nor One Medical’s closed onsite clinics. This figure does include both legacy One Medical clinics (98 clinics + 1 announced expansion into Miami) focused on the commercial market and legacy Iora markets (38 clinics) which were focused on Medicare Advantage patients. However, only one market – Denver – is covered by only legacy Iora offices. Collectively these 137 clinics represent a substantial majority of One Medical’s total of 188 clinics (per public reporting).

[7] Using the associated MSA for each market as a basis for population sizing.

[8] For example, Emory in Atlanta, Partners in Boston, University of Miami in Miami, Mount Sinai in New York, Duke in Raleigh, UCSD in San Diego and UCSF in San Francisco.

[9] Note: these CAGRs only allow for a partial year of the Iora Medicare revenues which, being largely about capitation, are considerable. However, our point is to evaluate the role of system partnerships in driving the legacy One Medical model rather than looking at acquisition-based growth.

[10] As noted below, we believe Amazon brings a more classic retail transactional mindset to healthcare so would be skeptical that their proposed population-based business models were actually linked with value.

[11] Whole Foods reportedly has 105K employees. Assuming 25% of these are in back office and logistics (likely concentrated in Austin where One Medical has no clinics) and that employees would be willing to travel up to 10 miles to go to a clinic, there would be 30-35K employees eligible. Using One Medical’s average activation rate (the share of eligible employees and dependents who use their services) of 40%, we would have 12-15K patients for One Medical. For comparison, One Medical is already treating >700K commercial patients. Further, these Whole Foods employees would likely partially overlap with patients Amazon Care is already treating and may not represent true new patients.

[12] Iora has its issues vs. its direct competitors in Medicare (see our “tear down” of Iora vs. Oak Street here). One Medical has published a study in JAMA Open of its performance with one employer. The study has some curious analytical choices and our guess is that the lower hospital admissions, ED visits and pharmacy costs for One Medical patients vs. a propensity matched cohort may reflect just a separation of engaged vs. unengaged patients rather than a change in clinical outcomes and costs.