PDF: Are some of Kaiser’s regional ambitions starting to pay off?

We have produced a new study evaluating developments in Kaiser’s regions (outside of California). The report provides an explanation for recent improvements in performance as well as leadership and governance changes. Further, we identify several implications for the future of Kaiser strategy.

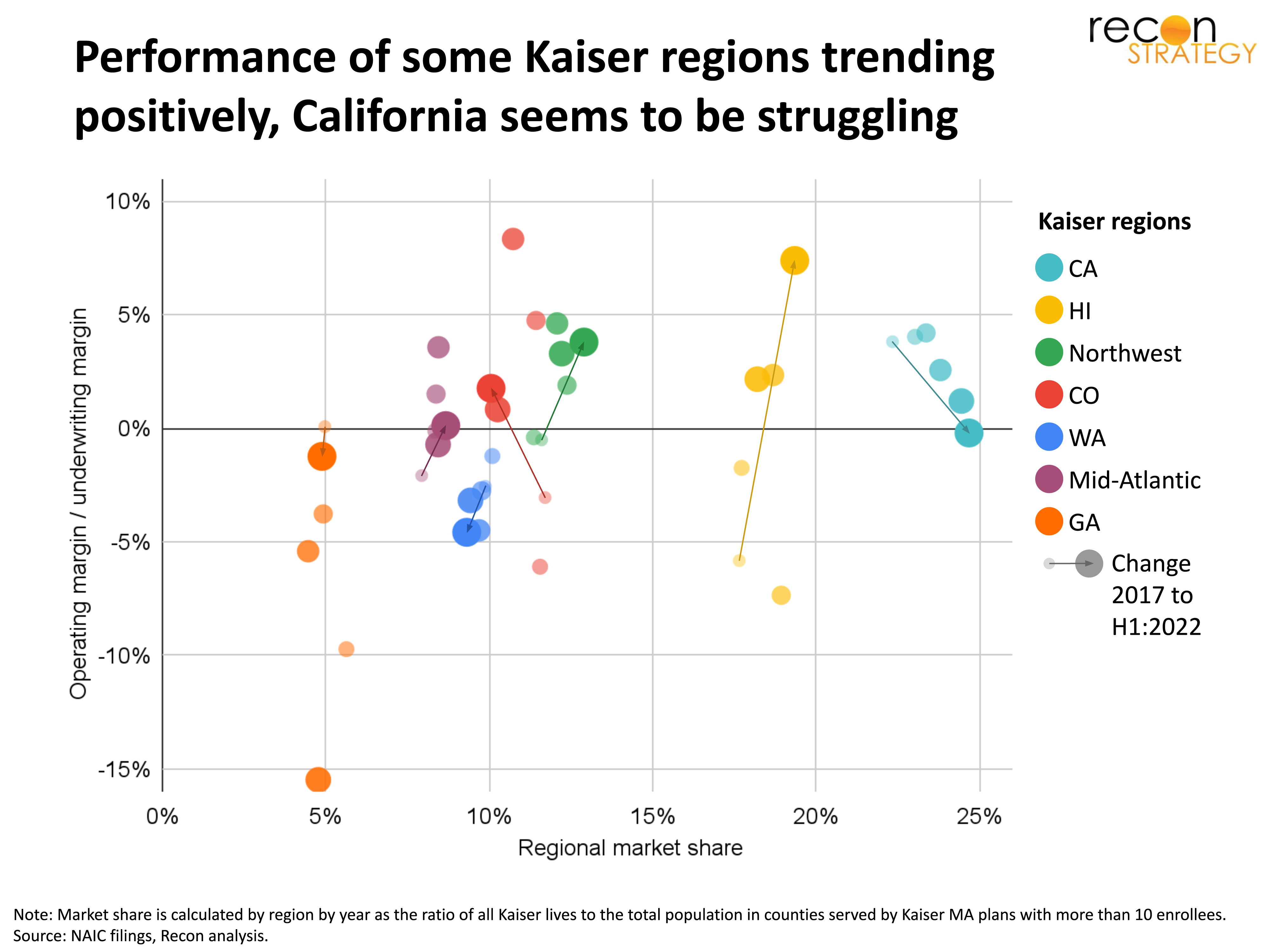

The Kaiser Permanente model has a heavy infrastructure, and so it requires a lot of local market share and operating scale to deliver a positive net underwriting margin (we roughly size how much using statistical analysis). Yet, even when market share and scale are at the lower end, several of Kaiser’s regions have seen a remarkable turnaround in underwriting performance since 2017.

The improvements are less about major changes in strategy and more about enhancing operations: repricing books-of-business while accepting attrition, improving care internalization and medical cost management, and sharply reducing bloated admin costs. Kaiser has been parachuting in “outsider” (non-Kaiser) leaders on a short-term basis to galvanize regional operations. Further, most of the regions outside of California operate a hybrid model in which hospital facility care is outsourced to strategic partners. It appears this strategy has benefited the regions as delays in repricing contracts with these strategic partners have temporarily buffered Kaiser from surging hospital costs. Because Kaiser has fully insourced hospital care in California, however, there is no comparable buffer from surging hospital costs. But, because competing health plans are buffered, Kaiser has not yet been able to raise premiums to match, contributing to the California downtrend.

The regional turnarounds have required a lot of changes in the care model, so the Permanente medical groups are a critical partner in execution. That’s likely why Kaiser has recently been restructuring the Permanente groups in Colorado and Washington (as part of a new KP Medical Foundation) which has given Kaiser a lot more control to drive these changes. This change may be part of a larger bifurcation in Kaiser strategy which recognizes the need for different models in markets where it has hospitals (California, Hawaii, Oregon/Northwest) and where it does not (Washington, Colorado, Georgia, Mid-Atlantic).

The recent turnarounds also confirm that, properly run, the Kaiser model does not need overwhelming share or its own hospitals to succeed, provided there is strong physician leadership and/or close alignment between the medical group and plan.

Please click the link below for the full report.

PDF: Are some of Kaiser’s regional ambitions starting to pay off?

Jacob Wiesenthal

Associate Consultant

Tory Wolff

Managing Partner