Over the last two decades, biotech companies have increasingly used therapeutic platform models that utilize a core technology potentially applicable to multiple targets or disease areas to develop a broader portfolio, theoretically with greater speed and cost efficiency than pursuing one-off assets.

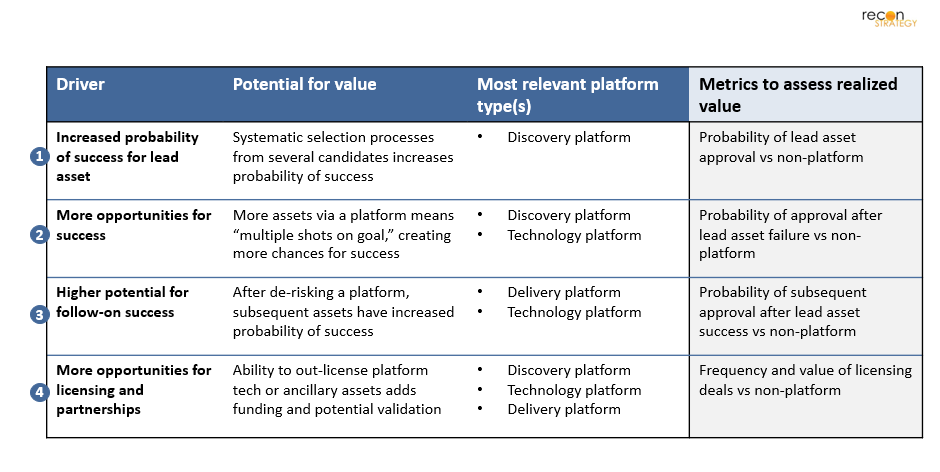

Despite extensive theorizing on the advantages of a platform model in biotech[1], few retrospective analyses have examined their realized value. In this analysis, we explore four hypothesized value drivers (Figure 1) of platform-based companies and evaluate the actual value achieved 10-15 years out from initial capital raise.

Figure 1: Key areas of potential additive value for platform-based companies during drug development, paired with metrics used to measure each area’s actual impact

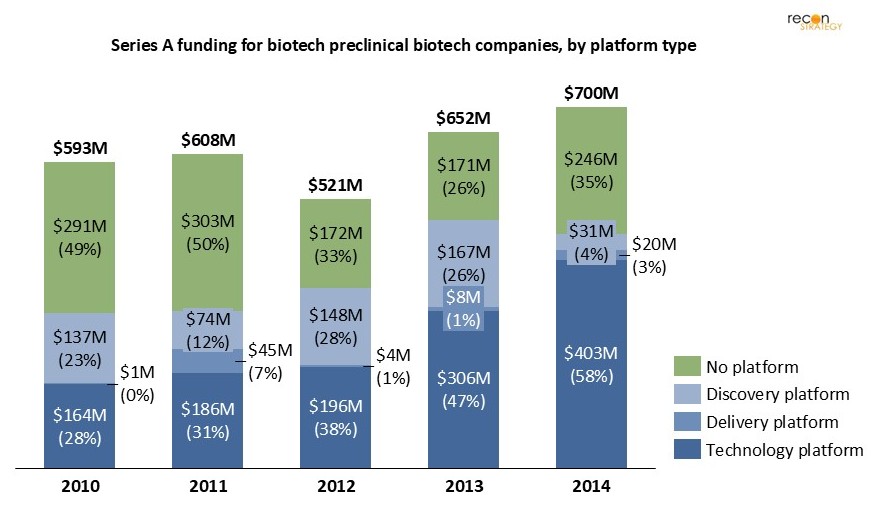

We analyzed five years of series A funding rounds (2010-2014), focusing specifically on companies that were in preclinical stage at the time of their raise. This ensured a level playing field when comparing success rates across platform and non-platform companies. Among Series A financing rounds generally, non-platform companies were more likely to be further along in development during their series A raise, which could artificially inflate their apparent success rate if not adjusted.

We classified companies as platform-based if, at the time of their Series A, they publicly described a core technology designed to generate multiple future assets. This classification was based on contemporaneous press releases and archived company website content. Platform types were further categorized into three groups: technology, based on a novel biologic or chemical modality; discovery, leveraging design or computational approaches to identify and/or optimize assets; and delivery, focused on innovations in drug administration.

Company cohort overview

Figure 2: Series A funding for pre-clinical biotech companies (2010-2014), grouped by whether a platform was announced at the time of the raise and by specific platform type[2]

For each year between 2010 and 2014, more than 50% of series A funding for preclinical-stage companies went to those with a platform, an increasing trend over the period. The majority of this funding went to technology platforms, most commonly those built around antibody engineering, though more advanced modalities related to cell and gene therapies also appeared. Discovery platforms accounted for the next largest share, often centered around protein design engines or high-throughput molecular screening. Delivery platforms represented a smaller portion of the total share, most commonly utilizing technology that aimed to improve targeted administration such as inhalers or specialized injectors.

Probability of success for lead asset

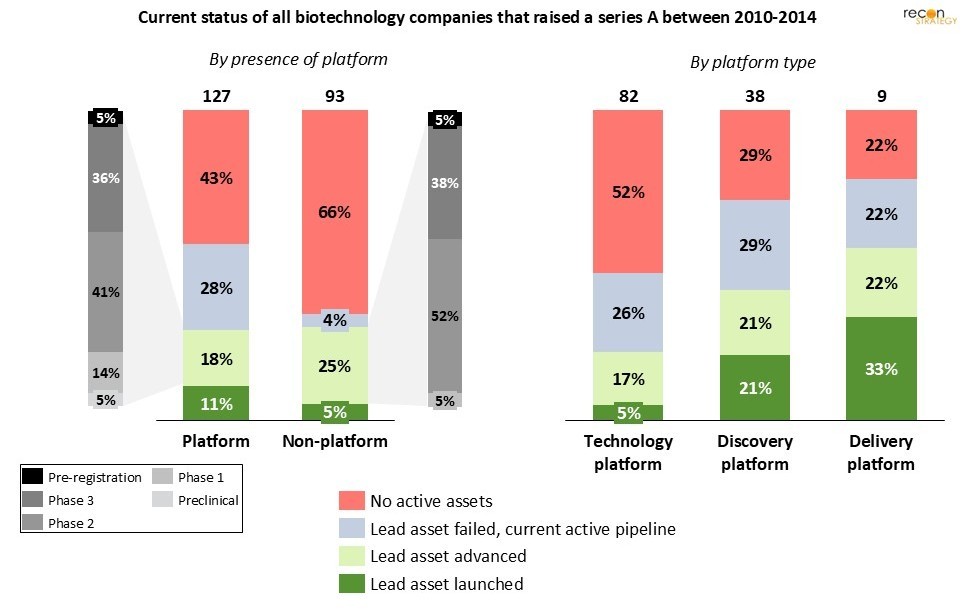

Our first analysis explores the first potential advantage of a platform model: increased probability of success for lead assets. To measure the realized value, we followed each preclinical-stage biotech that raised a Series A between 2011 and 2014 to see what became of the lead program and whether the company is still actively developing assets today.

Figure 3: Current development stage for biotechnology companies identified as having raised a series A between 2010-2014, grouped by whether a platform was announced at the time of the raise and by the specific platform type[3]

Platform and non-platform start-ups showed roughly the same rate of advancing their lead program (Figure 3), yet a larger share of platform companies made it all the way to launch. Digging deeper, technology-platforms, which are more likely to utilize new modalities or address novel targets, posted the lowest lead-asset success rate, suggesting additional scientific risk that comes with their increased use of untested modalities compared with non-platform peers. Discovery-platform companies landed in the middle: their success likelihood was higher than that of non-platform peers, suggesting that their systematic asset-selection processes do confer some benefit. Delivery-platform companies had the highest rate of lead asset success, potentially due to a typical approach of pairing established molecules with novel delivery tech.

Survival after a lead asset failure paints a sharper contrast. When a non-platform company’s lead program failed, most firms faded out entirely, with little or no follow-on R&D. In platform companies, by contrast, 30% saw their first asset fail yet continue preclinical or clinical development today.

Comparative opportunities for success

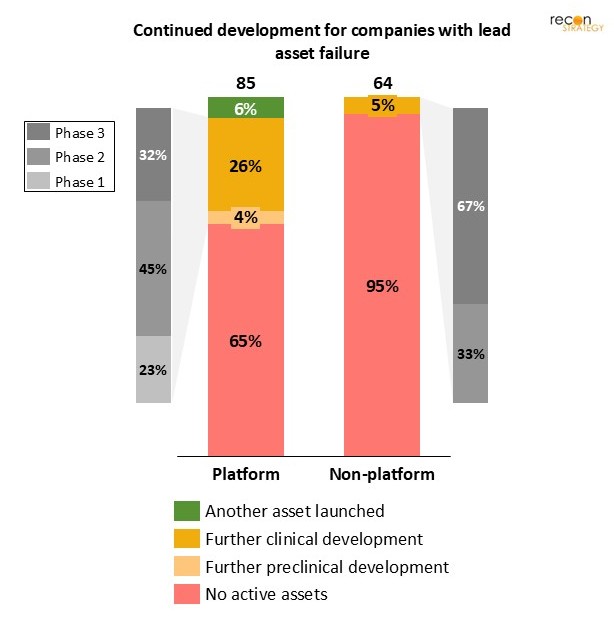

For companies where the lead asset at the time of their series A raise failed, we investigated each company’s subsequent development journey (Figure 4) to assess the second potential advantage of a platform model: more opportunities for success. Our analysis shows that platform companies have a much higher probability of surviving post lead asset failure – 65% of platform companies are now defunct compared to a staggering 95% of non-platform companies.

Figure 4: Current development stage for companies whose lead asset failed or ceased development[3]

Platform companies were not only more likely to survive post lead asset failure, but also more likely to see another asset launched. Among those experiencing lead asset failure, 6% went on to launch another asset with an additional 26% maintaining active clinical development. In stark contrast, non-platform companies saw no additional asset launches and only 5% maintain active programs in clinical development.

In many cases, platform companies were able to shift focus to a backup asset using the same core technology as the original lead, often after advancing multiple candidates in parallel. In the case of ADC Therapeutics, their lead asset camildanlumab tesirine, developed using their PBD-based ADC technology platform, was discontinued in Phase 3 after the FDA advised against submitting a BLA. However, the company continued to leverage its platform and ultimately secured FDA approval for loncastuximab tesirine (Zynlonta) in 2021. This illustrates how platform models can enable rapid follow-on development when a lead program fails due to asset-specific, rather than platform-specific, issues. These companies can quickly advance a waiting backup asset, potentially utilizing better-understood biology.

While the data does not show whether survival after lead asset failure increases value for investors, the launch and ongoing development rates (Figure 4) suggest it might. The rates are higher than those of lead assets for non-platform companies, even though the analysis captures a shorter window for advancement. Although this is not definitive proof that continued capital deployment in a platform translates into value for investors, this evidence suggests that these follow-on platform programs are not inherently destined to fail but instead may offer an additional shot at success.

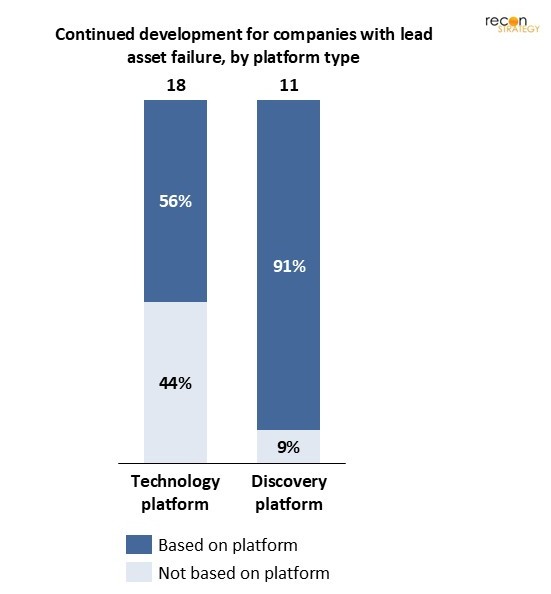

Figure 5: Use of original platform by companies with continued development after lead asset failure, by platform type

For platform companies that experienced a lead asset failure but have seen some continued development, we reviewed active programs to determine whether they remain based on the original platform. Companies’ subsequent development was designated “based on platform” if the platform was explicitly mentioned or clearly implied in the descriptions of the majority of their current pipeline programs. Our analysis shows that while platform companies are more likely to see subsequent success after a lead asset failure, their strategies underlying that success differ by platform type. Discovery-platform companies almost exclusively (91%) continue to develop additional assets using their original platform, indicating that in this case, lead asset failure is not necessarily indicative of the potential of a discovery platform.

In contrast to discovery-platform companies, technology-platform companies show a more varied response to lead asset failure. Continued development was fairly evenly split between original platform use and a pivot to something else. Among those companies that continued to use their original platform, ~50% pivoted use of the platform to a different therapeutic area. In the case of Juno Therapeutics, their lead asset at the time of series A using their CAR-T cell therapy platform made it to Phase 3 for relapsed or refractory B-cell ALL before being discontinued after several patient deaths. They continued using the platform in various hematological malignancies, resulting in the approval of lisocabtagene maraleucel (Breyanzi) for NHL, along with a broader clinical-stage hematology-oncology pipeline. Dimension Therapeutics, on the other hand, redirected their AAV liver-directed gene therapy platform away from hemophilia B, which was discontinued after a phase 2 failure, into rare metabolic diseases, where they are currently developing 2 phase 3 assets.

Among companies that did not continue development with their original platform after a lead asset failure, the majority (~70%) pivoted to another platform with varying degrees of similarity to the original platform. Kite Pharma’s lead asset at the time of series A was developed using their GM-CAIX therapeutic vaccine platform and was discontinued after phase 1. The company transitioned to their eACT cell therapy platform, which has led to the approval and marketing of axicabtagene ciloleucel (Yescarta) and brexucabtagene autoleucel (Tecartus).

Overall, these findings support the notion that platform models offer “multiple shots on goal” and greater flexibility post-failure. Compared to their non-platform counterparts, platform companies are more likely to survive and advance new programs after abandoning a lead asset. The relative resilience of platform companies is also not based on a single strategy, with companies pursuing a range of successful paths from continuing with the same platform technology while pivoting therapeutic area to pivoting entirely to another platform.

Probability of follow-on success

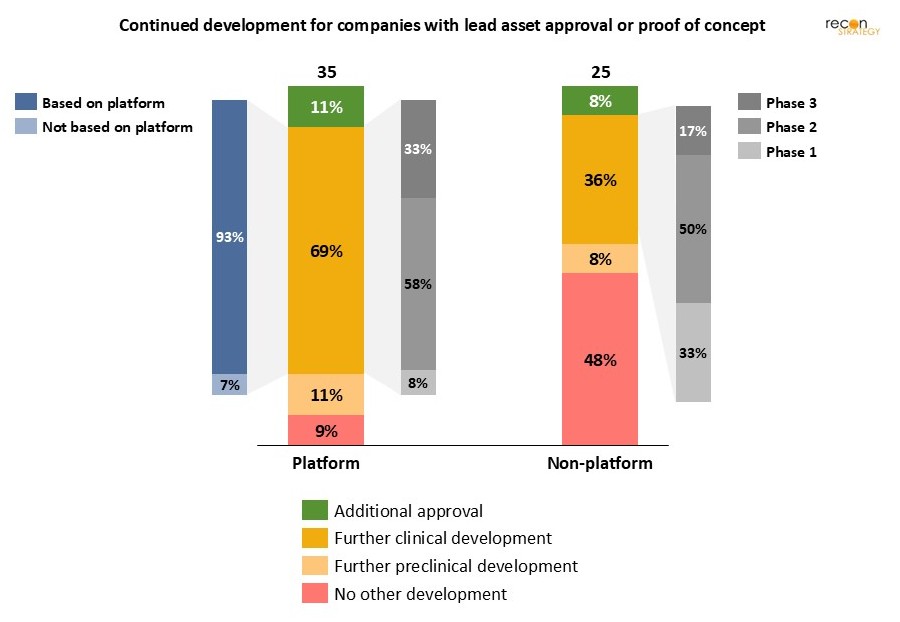

To test the third area of potential advantage of platform companies, higher reward post-validation, we focused on firms whose first drug had either reached proof-of-concept or made it to market. Among that subset, platform players were significantly more likely to have some level of continued development today. This trend may reflect the extra capital platform companies can secure before first approval, or the richer follow-on potential a de-risked platform offers compared with an asset-focused approach.

Figure 6: Current development stage for companies whose lead asset has launched or shown proof of concept, by presence of platform[3]

What we didn’t see was a surge in additional product launches after lead asset success. That’s surprising given that a proven platform should, in theory, make follow-on approvals faster and easier than entirely unique assets. This gap was most glaring for technology platforms: despite accounting for most of the Series A cash, not one has managed a second launch. However, this may be a result of a timeline effect, given 10-15 years out from a series A raise may not be long enough to bring multiple assets to market. Given that platform companies with lead asset approval have a higher rate of ongoing clinical development, we could see a corresponding higher rate of multiple approvals if looking 5-10 years in the future. There also may be an additional higher hurdle for truly novel modalities, which have a lower probability of success (as discussed above) and potentially longer timelines to approval to address novel regulatory and development procedures. Only one company in our cohort that was developing advanced therapies, CRISPR Therapeutics with its sickle cell gene-editing therapy Casgevy, had a lead asset approved.

In addition to a relatively similar rate of subsequent approvals, the average peak revenue projection to 2030 for all approved assets in this subset was very similar although the sample size is too small to draw significant conclusions. Each side had high performers (Apellis on the non-platform side, Loxo Oncology for platforms), and commercial disappointments (Rebiotix, Global Blood Therapeutics). This early data may suggest that, from a commercial standpoint, successful companies in both categories can look quite similar, even if platform companies may be advancing more programs behind the scenes. These commercial projections varied widely across platform types. Discovery platforms stood out with the highest average peak sales projections for approved assets, likely reflecting the greater ability of discovery platforms to generate and launch multiple high-value assets within the evaluation period.

Licensing and partnership opportunities

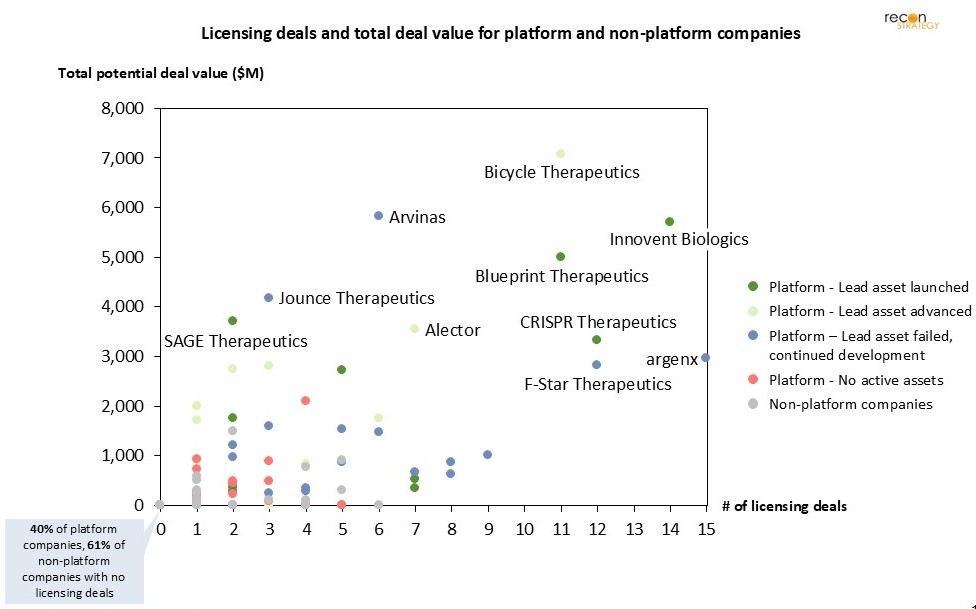

Finally, we examined all out-licensing activity for our company cohort. Resoundingly, the platform companies secured more deals and captured higher total potential deal value than their non-platform peers, a trend that was consistent across platform types. Notably, 60% of platform companies had at least one licensing agreement, compared to only 39% of non-platform companies. Perhaps more significantly, platform companies generated $748M in total potential deal value, more than five times the $136M average for non-platform companies.

Figure 7: Licensing activity of company cohort: each point shows a company’s out-licensing deal count versus its total potential deal value, including all upfront and milestone payments[4]

This licensing advantage likely stems from the core premise of platform models: the ability to generate multiple assets, either through a proprietary discovery engine or by applying a foundational technology across a broad range of targets and indications. That scalability creates more opportunities to out-license assets, either through agreements with large pharma for high-value indications that require commercial infrastructure, or through collaborative discovery partnerships with other biotechs.

This licensing advantage persists even in the case of lead asset failure. Argenx, for example, secured multiple deals based on its SIMPLE antibody platform, including a deal worth up to $1.8B for their anti-CD70 antibody with Janssen in 2019. Those partnerships provided a runway through multiple early lead asset failures, ultimately enabling the success of Vyvgart – now projected to exceed $5B in annual revenue by 2030, despite not being derived from the original platform.

Conclusions

Platform companies, especially those built around novel technologies, have drawn a growing share of venture capital in biotech, especially over the last five years.[5] Investors appear to buy into the idea that platforms, by enabling systematic drug discovery or unlocking new therapeutic modalities, can produce not just one product, but many.

Our analysis has shown that discovery platforms have historically offered the strongest return on that thesis. They showed the highest lead asset success rates, significantly more out-licensing activity than non-platforms, and accounted for nearly all multi-asset approvals within our cohort. Among companies with approved assets, discovery-platform companies also had the highest average projected peak sales. Despite these outcomes, discovery platforms made up a relatively small portion of overall series A financing in this period (18%), while technology platforms were much more significant (41%).

While technology platform investments may seem like classic high-risk, high-reward bets, they have not yet delivered on the upside of that narrative within this cohort. These companies faced lower lead asset success rates, and none in our cohort have achieved multiple launches. Even among those with an approved lead asset, average peak sales projections were lower than for non-platform companies.

Across platform types, two value areas stood out: greater survivability and more licensing opportunities. Platform companies were more likely to remain active and continue developing new programs even after early failures. This resilience may stem from larger pipelines, broader team expertise, more versatile technologies, or deeper access to capital and partnerships. In parallel, platform companies also secured significantly more out-licensing deals with higher total potential deal value, though the realization of this value through milestones remains unclear.

Looking ahead, further analysis could provide more evidence for the degree to which increased investment in platform companies translates into real value, beyond shorter-term development and commercial success. Key questions remain for this cohort, and new questions arise for more recent platform companies: does the higher rate of activity after lead asset failure, or even initial success, ultimately result in outsized commercial returns relative to investment? Do today’s AI-enabled discovery engines and emerging modalities deliver on the flexibility and scale akin to the platforms in our retrospective cohort? This continued analysis, along with corresponding thoughtful capital allocation from investors, will be critical in surfacing the platforms most capable of delivering meaningful long-term value.

[1] (1) ZS, “Why therapeutic platforms could provide a powerful innovation model”, 2023 (2) Jones CH, Beitelshees M, Hill A, Griffiths D, Murphy M, Kapadia K, Dolsten M, True JM. Framework to identify innovative sources of value creation from platform technologies. Proc Natl Acad Sci USA. 2025

[2] Crunchbase (accessed Jul 2025), platform status determined by contemporaneous press releases and website data at time of series A raise

[3] Crunchbase (accessed Jul 2025), platform status determined by contemporaneous press releases and website data at time of series A raise, current company status and stage determined by company website and PharmaProjects (accessed Jul 2025)

[4] Evaluate Pharma (accessed Jul 2025)

[5] (1) McKinsey, “What are the biotech investment themes that will shape the industry?”, Jun 2022 (2) McKinsey, “What early-stage investing reveals about biotech innovation”, Dec 2023