Merck’s recently announced acquisition of Verona is the latest in a long line of “revenue” acquisitions. With a $10B price tag for its COPD asset Ohtuvayre, the company is hoping to make a meaningful dent in the looming revenue gap from Keytruda’s loss of exclusivity. But even these late-stage “revenue acquisitions” come with meaningful risk.

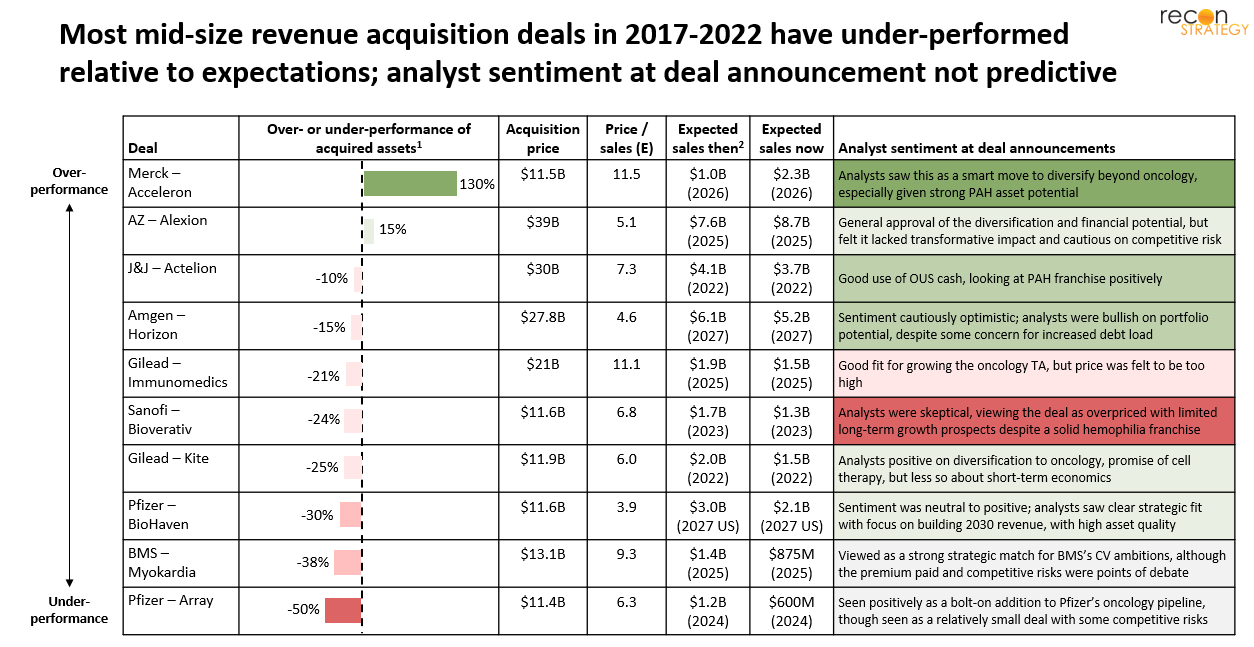

How have prior mid-size ($10-50B) biopharma revenue acquisitions fared? We reviewed 10 such transactions announced between 2017 and 2022. For each, we compared 5-year revenue projections at the time of announcement with today’s actual results (or the latest available forecasts for deals announced after 2019). We also examined analyst commentary from the time of each announcement, summarizing sentiment across at least 4-6 sources per deal.

Figure 1: All mid-size ($10-50B) biopharma M&A transactions between 2017-2022 involving marketed or post-Phase 3 assets [1]

We found that forecasts are often optimistic, with many transactions missing their projected sales trajectories. Only 2 of the 10 transactions are expected to exceed their original revenue forecasts (Merck/Acceleron and AstraZeneca/Alexion). Analyst sentiment at announcement showed little correlation with ultimate performance, with most deals, across over- and under-performers, receiving positive reviews. Mid-size acquisitions also tended to fade from analyst coverage after announcement and closing, surfacing again only in cases of major underperformance (e.g., impairment charges), which generated minor news flow.

Taken together, the findings indicate that although revenue acquisitions carry less scientific risk than early-stage bets, they still demand discerning judgement to assess, and ultimately capture, long-term value. Strategic benefits outside of direct revenue (e.g., enabling new discovery programs) are possible, but appear marginal in most of these cases.

Merck’s success with the Acceleron acquisition stands out as a rare clear overperformer in this category. Time will tell whether Verona can follow in its footsteps.

[1] Notes: % difference between expected target sales at the time of announcement and actual sales or projection as of Jul 202, 5-year forecast of expected target sales at the time of announcement, Sources: Evaluate Pharma, contemporaneous analyst reports