MSFT’s pathbreaking alliances in healthcare services are impressive and well designed to grow adoption of their Azure cloud over the medium term. But if MSFT wants to be at the forefront of change and maintain a robust hold on healthcare cloud share in the long-term, their publicly disclosed partner set seems highly incomplete[1].

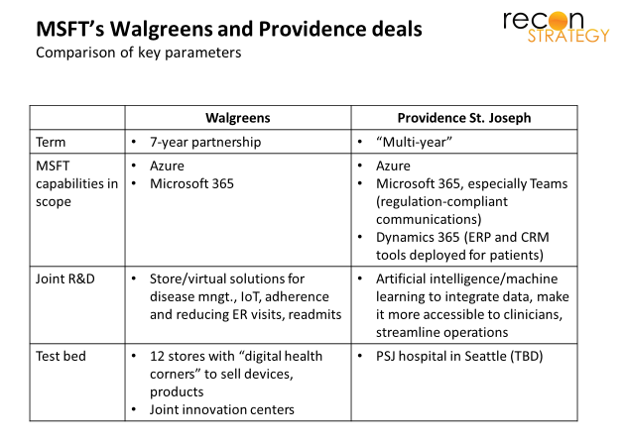

The two major alliances announced this year – Walgreens and Providence St. Joseph (PSJ) — are predictable outcomes of the emergence of the UNH, CVS/AET and CI/ESRX triumvirate. Healthcare’s anxious mid-tier services players need enablement partners with scale and capital while Big Tech wants footholds to drive lucrative industry transformation. (We made this prediction earlier this year here[2]). The two deals both emphasize cloud, productivity tools, and joint development (see table below).

A closer look at the PSJ deal

Per PSJ press release, the deal will accelerate the “…adoption of the cloud and enable data-driven clinical and operational decision-making by leveraging Azure and FHIR to integrate siloed data sources….” PSJ CEO Rod Hochman is looking for process improvements both from enablement (e.g., helping clinicians be more productive and supporting collaboration) and analysis (e.g., by “understanding why the cost and quality of similar procedures can vary across its 51 hospitals and hundreds of clinics”).

No surprise that creating value from EMRs is top of mind. The Cloud appears to be a low CapEx way of lifting insight from the data traps hardwired into legacy systems, and, thus, a perfect tool for the mid-tier to level the playing field vs. the capital-rich giants.

Supporting PSJ diversification and seeding a new distribution partner for MSFT?

PSJ likely also sees a big top-line synergy with their diversification strategy. It recently acquired Bluetree (an Epic consulting firm), Engage (reportedly one of the largest Meditech solutions with revenues of $44M, 165 customers and a hosting business), and Lumedic (a blockchain revenue cycle management start-up). It is looking to use these as a starter kit for a services business yielding $1B in revenues and 20% return by 2023.

How? The theory seems to be as follows: PSJ can insert its experience with Meditech, Epic and converting from one to the other (as it is now doing with its CA hospitals) into these subsidiary vendors. Engage can support providers on Meditech (for which talent is becoming scarce) via hosting. Then, when customers are ready, they can transition to Epic via Bluetree and Community Connect (a vehicle for independent systems to use Providence’s version of Epic). With the MSFT deal, PSJ will gain analogous experience with rolling out Azure on top of Epic which it can feed into the services business. Bluetree can go from an Epic optimizer to an Epic + Azure optimizer.

Network effect for anchor tenants on Azure

MSFT – which has about half of AWS’s share in cloud services – must be delighted to score a major Epic customer like PSJ[3] and lay the groundwork for a new channel partner. Beyond that, MSFT’s choice of alliance partners seems to be focused on adding organizations that are “must have” partners for large swathes of healthcare. Walgreens dispenses and counsels at least some patients of most providers in America. PSJ is the largest hospital system in the Pacific Northwest (and in many regions of that geography, the only provider of referral and facilities care[4]).

Having large-scale players operating on your cloud creates compelling value for others who want to collaborate on clinical and business processes while avoiding the complexities of a multi-cloud environment[5]. Access to large players also can attract developers to a platform. The lure of hospital-anchored delivery systems for a software company is understandable. IT budgets and headaches are enormous, the hospital industry is amid a difficult transformation, and most would agree that only the hospital systems with the best information will thrive.

But is the hospital the right setting to design the future of healthcare?

MSFT and PSJ plan to use one of PSJ’s Seattle hospitals as the initial test bed before a broader roll-out. It is no surprise, therefore, that the press has described the effort as creating the “hospital of the future.”

Yet, hospitals are playing a declining role in our increasingly value-based healthcare system. In time, much of today’s hospital care will shift to other settings (e.g. ASCs, hospital at home) or eliminated (e.g., avoidable admissions, new cures). “Hospitals of the future” will be fewer, smaller, more specialized.

Hospital-anchored systems are focused on surviving, not leading, that transformation. Capital-intensive facilities plus relatively fixed, talented, expensive staff require volume to sustain them. Unless your occupancy is high, the ROI on keeping patients out of your hospital is near zero[6]. Hospital leaders may evangelize about transformation and strike myriad deals with start-ups. And the cloud could – theoretically – ease the standing up of new capabilities, shorten the time between piloting and production and reduce the technologies stuck in pilot purgatory. “Easing” is not the same as easy, however. The complexity of hospital operations keeps operating models and cultures relatively inward looking. And the weight of all those cash-hungry fixed costs will slow down even the most forward-thinking leaders[7]. Culture, after all, eats strategy for breakfast[8].

The next generation of value-based care will most likely be led by organizations facing the entire bill for hospital care — not just the marginal costs. These “anti-systems” combine muscular primary care, ambitious care internalization, collaboration across clinically integrated networks (CINs – great opportunities for cloud) and appetite for risk. For these organizations, the cloud won’t be a short cut to get around rigid EHRs. They will be vital platforms for (1) managing new information flows (“always on” connected devices/IoT, etc.) that will, in time, dwarf those exclusive to hospital-based care and (2) tightly collaborating on care management across care settings and CIN partners. Supporting vendors and developers in analytics and life sciences will regard those organizations as “must have” customers and will focus their efforts accordingly.

AMZN seems to understand this. While AWS has a deal with Cerner (which will, presumably, help them reach hospitals on that EHR) and with academic systems such as Beth Israel Deaconess in Boston, they also report relationships with innovators like Iora, VillageMD, Aledade, OneMedical, Zocdoc, Livongo. And AWS advertises that it is the needs of their diverse customer portfolio which drive feature development (“90-95% of what we build is driven by what customers tell us matters” per Shez Partovi who leads AWS’s business development in healthcare).

To the extent MSFT is interested in being at the forefront of healthcare, it would do well to balance its strategic partnerships with big hospital-anchored players by adding some of these anti-systems and the diverse, multi-stakeholder CINs which they often orchestrate. Otherwise, MSFT risks setting up Azure as a platform focused on solving narrowly scoped issues for a shrinking portion of care delivery (integrating EHRs, optimizing costs for hospital procedures, readmissions) and being in second place with the needs of broader transformation.

[1] We assume here that the publicly disclosed deals are representative given every cloud vendor’s interest in building a picture of healthcare momentum for their offering.

[2] At the time, we also thought PSJ’s raiding of MSFT and AMZN talent and acquisitions indicating that PSJ abjured help from Big Tech and planned to “go it alone.” This assessment has proven wrong. Perhaps Big Tech was, in fact, seeding talent into PSJ in order to accelerate their acceptance of an alliance strategy.

[3] MSFT already made some inroads to Epic in 2017 with a deal to have Epic’s AI “Cognitive Computing Platform” on Azure. These deals potentially setting up a split across the two major EHR vendors, given AWS’s 2018 deal with Cerner.

[4] Notably, MSFT is also a strategic partner with UPMC – the leading (some might say dominant) facilities provider in most of Pennsylvania — in a $2B project to build three new specialty hospitals in Pittsburgh. This effort has not visibly been identified as involving Azure or other MSFT tools but UPMC has positioned MSFT’s involvement as ensuring that the designs will be technologically sophisticated.

[5] It is probably just a coincidence that Walgreens and PSJ already partner together in a small way that could be facilitated by a shared cloud platform (Providence operates the retail clinics housed within Walgreens stores in Pacific Northwest markets). But the PSJ CEO brought up their Walgreens partnership in the context of the MSFT deal, suggesting that, even when tiny, the network affect caught his attention.

[6] The incremental operating costs of these initiatives will often more or less cancel out the avoided marginal costs of care delivery at least to the point where the actual returns are vanishingly small relative to the overall bottom line.

[7] Having a health plan arm (as PSJ does as does MSFT’s other notable hospital system partner, UPMC) does not change the economics much for a delivery system: Given the high contribution margin on volume, you are more than willing to discount care (especially in a controlled way to an affiliated plan) in return for more members in your plan loyally using your delivery system.

[8] The same logic applies to the Walgreens partnership. Walgreens has been handing over its clinics to local incumbent delivery systems (thus dealing themselves out of risk). They have little interest in making waves for local big providers. Ultimately, a pharmacy’s mission is dispensing medications and their interest in digital will be governed by its contribution to that end.