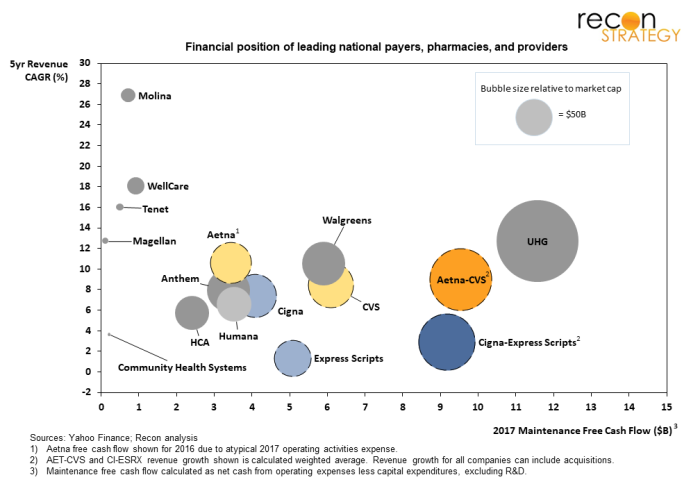

With the closing of the CVS/AET and CI/ESRX combinations, healthcare services are now led by a triumvirate of vertically-oriented goliaths. And we can anticipate that there will be more care delivery acquisitions and investments to fill out the new vertical platforms—just as the leader UnitedHealth Group (UNH) continues to invest in its care delivery arm (with the pending acquisition of DaVita’s physician group) a decade after it first went into the clinic business.

The extent to which the two new combinations have allowed legacy constituents CVS, AET, CI and ESRX to break away from the pack (and compete with UNH) in terms of financial resources can be seen in the chart below. The capital, scale, data assets and, perhaps most of all, the ability to pursue disruptive strategies of these three organizations make them intimidating to the vast array of smaller care delivery, care management and financing players (both for-profit and non-profit).

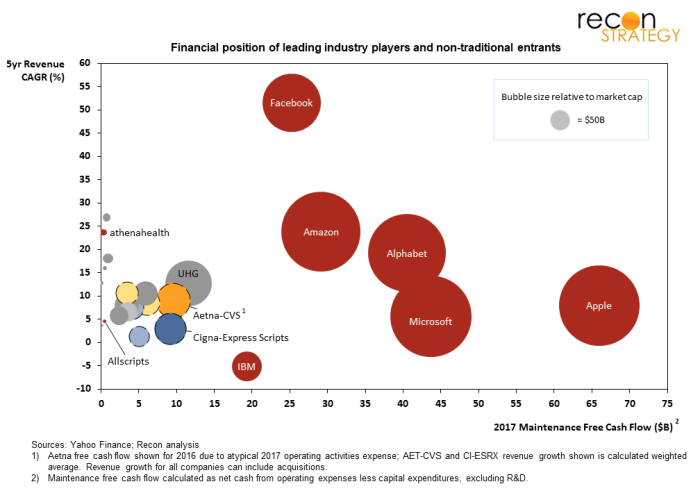

The smaller healthcare services players should keep in mind, however, that UNH, CVS/AET and CI/ESRX are, in many ways, prepping defensive positions. Their executive teams have been observing the healthcare experimenting by tech giants—including Alphabet, Amazon, Apple, Facebook, and Microsoft—over the past 3-4 years and the accompanying excited speculation that they will “fix” healthcare. And no wonder: the growing impatience with healthcare’s poor value proposition has created the invitation and heavy IT/digitization investments (e.g. EMRs) over the past decade have given these tech players a key to healthcare’s backdoor. The resources of these tech companies dwarf the “Big 3” in healthcare services. Imagine the executives in Minneapolis, Woonsocket, or Bloomfield looking over their shoulders and seeing this picture:

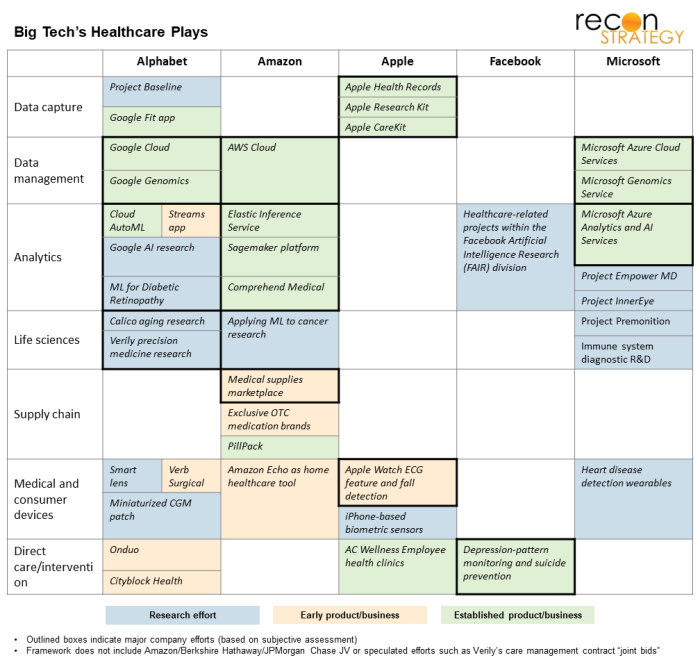

The tech giants’ initial forays into healthcare—whether by directly developing products and services or by strategic participation in ventures—range from logical extensions of their existing businesses in data services all the way to care provision and life sciences. The table below identifies major publicly disclosed efforts:

Of course, layered across all of these is the potential for artificial intelligence, an area in which tech incumbents have major capabilities and deep benches of talent. Efforts around AI include platforms that legacy healthcare companies can leverage to create their own AI-driven applications (e.g. Microsoft Azure, AWS, and Google Cloud) and standalone healthcare solutions. Within the latter category are the Apple Watch ECG feature and Microsoft’s Project EmpowerMD, an effort with UPMC to create an intelligent scribe learning system.

What does this mean for mid-tier healthcare services?

In the looming competitive struggle between healthcare’s vertical goliaths and the tech giants, what plays are available to the many mid-sized healthcare services organizations?

One response might be to try to compete on their own by investing in their own capability build-outs and scaling moves. Providence St. Joseph’s hiring of big tech execs and tech start-up acquisitions (most recently in blockchain for revenue cycle management) suggest a plan to stand on their own. In our view, such a path will take time, more resources than mid-tier players will have, and risks getting buried by day-to-day strategic and operational challenges of shifting to a value-based world.

Alternatively, mid-sized healthcare services players could make common cause with the tech giants. WBA’s recent deal with MSFT may be the first major example of such a deeply committed partnership: according to press reports, WBA will migrate the majority of its IT infrastructure onto Microsoft Azure, focus on consumer experience through digital capabilities, create a connected “ecosystem” of payer, provider, and pharma partners, develop chronic disease management applications, etc.

The mutual benefit offered by such deals is clear. Mid-size healthcare services players can leverage the scale and strength of their partners’ platforms to better compete against the vertical healthcare goliaths. They also secure big friends with interest in their survival and success. Tech giants, on the other hand, secure partners who can fill in the gaps in their healthcare expertise, potential reference clients and channels.

Given their compelling logic, we can expect more such deals.

Sophie Ranen

Associate Consultant

Tory Wolff

Managing Partner