The battle to own healthcare’s consumer relationship is being nowhere fought more intensely than in the mobile arena. Tea leaves suggest that Aetna has pulled back from trying to own this relationship in favor of a more collaborative “ecosystem” strategy, but United appears determined to lead. The thinking is speculative but I let me point out the emerging evidence and offer some guesses on what will come next.

Strategy environment for consumer mobile health

At the risk of oversimplification, let me offer six hypotheses regarding the strategic context for consumer mobile health:

(1) The space is very much in flux: there are a wide and expanding variety of value propositions, technologies and products with no view on what the final “stacks” (structure of service and product layers often collaboratively manufactured by different players which together deliver on a value proposition) and ecosystem will be. The consumer relationship today remains largely fragmented.

(3) However, right now, no one player (e.g. the manufacturer of the smartest sensor, the manufacturer of the most user-friendly display device, or company managing rewards and incentives for behavior change) is clearly positioned to win that integrator relationship. Many players see pathways to winning and will, therefore, jockey for that position. Players compete not just within their own “stack” but also using their “stack” as a platform for owning the relationship.

(4) Because mobile health is an evolving ecosystem, there is a lot of potential complementarity across players. This complementarity can be used strategically:

- selective interoperability (picking a few complementary players to interoperate with) to ride each other’s adoption coattails

- agnostic interoperability (being interoperable with all of a particular category of complements) to avoid favoring any one player and keep a portion of the market fragmented, and

- strategic decoupling (removing or avoiding interoperability with a player) to prevent or slow the growth of a potential competitor.

(5) When clinical stakes are high, providers will want to control the infrastructure (to ensure accuracy, reliability in the face of implied liability). It is, therefore, largely the healthy segment of consumers where a mobile health vendor can exploit a strong relationship. Implication: the clinical value at stake for holding the consumer relationship for mobile technology will be relatively small (a wellness payoff among the healthy).

(6) While the clinical payoff may be limited, the consumer mobile health relationship is attractive: incumbency here will ease follow-on sales of next generation products and services, aids cross-selling, and opens the opportunity to charge “taxes” for interoperability. It will be good to be king.

Just because the clinical cost payoff may not be large (per point #5 above), health plans should be very interested for two reasons:

- Owning this relationship creates affinity, stickiness and marketing opportunities for health insurance products (per point 6), something that will only become more important as health insurance becomes more retail.

- As the scope of value add for health plans shrinks (due, for example, to the transfer of risk to others in the value chain), the remaining opportunities for plans to differentiate acquire outsized importance. Even if the wellness payoff is small, plans need to hold on to the responsibility and the margin for delivering on that payoff

Even if the consumer mobile health space is nascent, its evolution is of deep strategic importance for the health plan industry. Let’s take a look at some recent moves by two big health plans and speculate a bit about the implications:

Aetna

CarePass was Aetna’s consolidation play with consumers, designed to collect, integrate, analyze and store self-generated health data with curated apps and appeal beyond Aetna’s current membership. This ambition, I have argued, set Aetna on a collision course with Samsung (which had similar grand designs for its S-Health and installed base of phones), perhaps pushing Samsung into the arms of Cigna for an open-ended strategic development partnership last year.

A few months ago, however, Aetna has shut down CarePass (we are indebted to the team at mobihealthnews for reporting). At the time, the rationale for an irrevocable, noisy exit from a key but immature market was not obvious (see here for 10 often mutually contradictory hypotheses from early September). But a few weeks ago, Samsung announced Aetna as one of its new roster of development partners. It seems clear that shutting down Carepass cleared Aetna’s strategic slate to collaborate with Samsung.

If Aetna has ceded the “software stack” (see exhibit) to others, it is a strategic retreat to a well prepared position: Aetna can focus on “close-to-home” plan-related opportunities for mobile (benefits, programs, incentives, provider interactions, etc.) while collaborating with – and thus benefiting from the adoption of – one-time former competitors’ technology (such as Samsung). The “plan/benefits stack” for mobile may be too narrow a platform to build a broad consumer mobile health relationship, but strategic retreats always involve trading off opportunity to reduce risk.

Unitedhealth

United has a long and active history in consumer mobile health (e.g.,consistent participation in the annual Consumer Electronic Show, various engagement apps such as OptumizeMe and Health4Me, and widely publicized alliance with Fitbit). Earlier this year, Optum bought a majority stake in Audax, an early stage company which integrates health plan data, care management interactions, biometric data, etc. to help consumers manage health – in other words, a potential platform for the primary mobile consumer health relationship.

This past August, United (along with Humana) was reportedly in talks with Apple regarding Healthkit. It could be this signaled United’s openness to sharing the “software stack”– United has the scale and the organizational flexibility to pursue multiple, potentially conflicting strategies at the same time. However, the only publicized outcome of those meetings was Humana’s broader collaboration with Apple. As far as United goes, there is silence.

My interpretations is that, despite what they learned from Apple, United still wants to control the ecosystem and own the consumer mobile relationship. Keep in mind that, via Optum, success could be meaningful also for United’s businesses serving other health plans, providers and other players in the market.

One tea leaf to consider: What has happened since Apple’s meeting with United in August is the FitBit and Apple decoupling. It may be that Apple took the initiative to create room for its Apple Watch. But Fitbit may have made the decision itself since it has no plans to integrate with Healthkit. While Fitbit certainly has some emerging muscle, it is a risky move to cross swords with Apple in such an early stage in the market’s development. Perhaps – just speculating, of course – Fitbit sees that United (its long-time strategic partner) shares a reluctance to see Apple win the consumer relationship space via its Healthkit middle layer play and therefore won’t push for its adoption. Having a major payer as an ally might help explain Fitbit’s boldness.

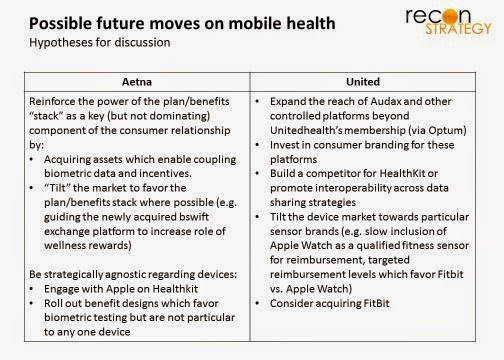

What’s next?

Even if these interpretations are correct, the battle is far from concluded. But there are a few things we expect to see from United and Aetna in the coming months: