Introduction

It has become a truism in the pharmaceutical industry that new product performance is more often divergent from pre-launch forecasts than on target. In fact, less than 24% of major products (>$250M annual US sales expected or achieved by year 5 post-launch) launched in the 2014 – 2019 timeframe was within 30% of pre-launch forecasted revenue, while 27% exceeded those forecasts by 2x or more, and 24% were less than half of expectations.[1] This uncertainty drives significant misallocation of resources.

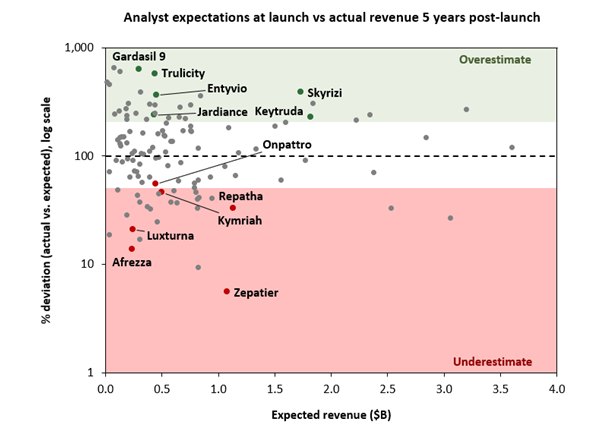

Understanding the drivers of this uncertainty—and what is controllable through effective product strategy—is critical to building world-class strategy functions. We recently took a retrospective view of major FDA-approved drugs (assets projected to achieve $250 M+ peak revenue) launched between 2014 and 2019 in the U.S.; 130 assets were ranked by comparing actual revenues at Year 5 post-launch against analyst revenue predictions at launch. To understand why drugs over- or underperform relative to pre-launch analyst predictions, we evaluated each product against five key themes: payer dynamics, provider practices, patient behaviors, scientific advancements, and supply chain logistics. These themes are intended to encompass the full spectrum of challenges drugs face from approval to commercialization, influencing their revenue trajectory and market performance.

Figure 1. Summary of analyst expectations at launch vs actual revenue, 2014-2019, $250M+ projected peak revenue

While our analysis focuses on outliers that significantly over- or underperform compared to their forecasted revenues, these takeaways should apply more broadly. By examining these extremes, we aim to illustrate key factors influencing drug performance, providing insights that can help refine predictions for all drugs, whether they are outliers or fall within more typical performance ranges. As the market landscape shifts—driven by evolving rebate dynamics, the growing role of patients in determining their own care, the increasing influence of biosimilars, and the rise of curative gene therapies—forecasts must be adapted to align with real-world outcomes. This paper highlights the critical factors within these five categories that contribute to a drug’s success or failure in meeting expectations and concludes with a set of reminder questions that drug strategists should ensure are well covered.

Payer

In our sample set, failure to address payer concerns adequately was a key driver of underperformance. These concerns are especially important when the price is high enough, or the population large enough, to materially impact the economics of the relevant risk pool.

For example, PCSK9 inhibitors like Praluent (Regeneron/Sanofi) and Repatha (Amgen) launched with strong clinical efficacy but faced significant payer resistance due to their initial $14,000+ per year price tag, which significantly exceeded the predicted $5,000-$10,000 per patient price point.[2] Adding to the alarm, analysts projected upwards of 2–10 million eligible patients, creating a potential $20B+ spending burden if PCSK9 inhibitors were used widely. This concern was further amplified by the removal of strict LDL-C targets in 2013 and ambiguous definitions of statin intolerance.[3],[4],[5],[6] Praluent’s FDA approval did little to quell these concerns when it was approved adjunct to diet and maximally tolerated statin therapy in patients with heterozygous familial hypercholesterolemia or patients with clinical atherosclerotic cardiovascular disease.[7] Subsequently, real-world access was constrained by restrictive coverage policies, with 30% of discontinuations attributed to payer refusal,[8] marking one of the first major cases where insurers effectively dictated market outcomes. Ultimately, Repatha achieved $376M in sales in the US by 2019 compared to the predicted $1.1B. Praluent achieved $125M in sales in the US by 2019 compared to the predicted $842M.

On the flip side, ensuring that pricing and rebate schemes are aligned with payer incentives can help with faster uptake and growth. When Skyrizi launched in 2019, Citi analysts projected peak sales of $3.7B,[9] citing limited time to establish itself before biosimilar competition. Yet by 2023, Skyrizi held 21% market share and generated nearly $10B in US sales.[10] While Skyrizi did bring excellent clinical results to the table, outperforming competitors like Stelara in Crohn’s disease trials,[11],[12] AbbVie’s success was driven in part by leveraging Humira’s existing rebate structure to secure formulary placement for Skyrizi – rebates amounting to an estimated $7 billion to US commercial plans, with PBMs receiving $1.5 billion.[13],[14] More specifically, others have reported that AbbVie tied the profitable rebates of several of its largest drugs together in an all-or-nothing arrangement.[15],[16],[17] Under this deal, if a PBM chose to recommend a biosimilar over Humira, it would risk losing rebates for other AbbVie products—such as Rinvoq and Skyrizi. As a result, PBMs would be heavily incentivized to favor AbbVie’s portfolio (including Humira) over competing biosimilars. AbbVie’s strategies to retain market share versus biosimilars proved remarkably effective: when biosimilars launched in 2023, they captured just 2% US market share, compared to 35% in Europe where such rebate structures did not exist.[18]

Provider

Several of the products with major gaps against expectations had unusual requirements or benefits for providers. Understanding the intricacies of provider dynamics is essential for navigating market performance.

On the plus side, targeted marketing to specialists and disease-specific patient support where appropriate can improve uptake. One example is Entyvio, which gained unexpected success in part by marketing specifically to specialists and offering robust patient support programs that reduced the burden on providers after prescribing the drug to their patients.

Positioned as second-line to TNF inhibitors like Humira, Entyvio’s approval was initially met with uncertainty. Early forecasts projected peak sales under $1B, with biosimilars expected to erode market share by 2019.[19],[20] But just a year post-launch, some analysts tripled their estimates after seeing Entyvio’s early traction.[21] This is partly because Takeda rolled out a commercial strategy focused on physician relationships and patient support (see Figure 2 example provider support materials below). Unlike broader autoimmune biologics’ campaigns (e.g., Humira or Remicade), Entyvio was marketed exclusively to gastroenterologists. As a result, in 2016, among biologics used to treat the same conditions like Stelara, Remicade, Simponi, and Humira, Entyvio accounted for proportionally far more prescriptions among GI providers compared to all specialties (5x as many prescriptions from GI compared to all other specialties combined). This demonstrated that gastroenterologists were notably more comfortable prescribing Entyvio than non-GI doctors when it came to these competitor drugs.[22] Takeda’s EntyvioConnect program enrolled over 6,500 patients within the first year, covering about 70% of the patient base.[23] Beyond the successful physician targeting, an evolving treatment paradigm also worked in Entyvio’s favor. As understanding of TNF inhibitor failures became more sophisticated through therapeutic drug monitoring, Entyvio’s market opportunity as a second-line therapy to TNF inhibitors expanded beyond initial expectations.[24],[25],[26],[27],[28] By 2020, the FDA removed language about TNF blocker failure from its label.[29] Entyvio sales reached $4B in 2024, double what analysts predicted in 2015, proving that even in a crowded market, strategic physician engagement and evolving treatment practices can redefine a drug’s potential.

Figure 2. Takeda’s Entyvio provider support materials. Takeda went to great lengths to facilitate Entyvio’s ease of use for providers going as far as explaining how providers can fill out a prescription, different models for administration and subsequent reimbursement, how to complete a claims form, and how to properly code the applicable treatment procedures.

In contrast, products which require complex investments or changes in process / behaviors on the part of providers have faced meaningful headwinds. One well-known example, Kymriah, the first CAR-T therapy approved for leukemia and later for lymphomas, underperformed analyst expectations not due to lack of efficacy, but because its complex manufacturing and administration process required a major shift in provider practice.[30] CAR-T treatments require patient cell collection, weeks-long lab processing, and specialized reinfusion, which created logistical hurdles for hospitals and delayed adoption. A survey of providers found that over 60% encountered at least two logistical obstacles at every stage of CAR-T administration. While manufacturing timelines have improved from an initial 52-day turnaround to closer to 2-4 weeks,[31] its $475,000 price—lower than some analyst projections of up to $750,000[32]—along with competition from faster and cheaper alternatives like Yescarta[33] (and challenging ramp in manufacturing capacity) limited Kymriah’s commercial success. Five years after its launch in 2017, Kymriah achieved $230M in sales, falling far below the $497M pre-launch predicted year-five sales.

Patient

The ability to better understand and anticipate patient demand dynamics has become increasingly critical, with more tools becoming available to uncover these insights. In our sample set, we saw three themes.

First, how patients balance the benefits and burdens of therapies is fluid. Innovation can rapidly change the cost-benefit calculation for patients, making it essential to track these shifts in real time to stay ahead of evolving demand dynamics.

While GLP-1s have garnered significant commercial success in recent years, initial forecasts for the GLP-1 class were modest: Credit Suisse predicted a $10-12B market by 2020, and others echoed similar projections.[34],[35],[36] When Trulicity launched in 2014, injectables were regarded as second-tier options behind oral therapies like SGLT2s and DPP4s for type 2 diabetes.[37] By 2016, the prevailing belief was that only oral GLP-1s had true blockbuster potential.[38] Because providers had already been thoroughly surveyed, the surge in demand stemmed primarily from unexpected patient behavior. Patients clearly cared less about convenience than providers or analysts predicted leading to a drug like Trulicity’s blockbuster success.

Similar misunderstandings of patient-driven demand dynamics led to opposite commercial outcomes in the inhaled insulin market. Industry initially attributed Exubera’s commercial failure in the 2006-2008 timeframe due to its bulky administration device and inconvenient dosing regimen.[39] However, the subsequent failure of Afrezza, another inhaled insulin launched in 2015, highlighted a deeper miscalculation: needle-free insulin delivery simply wasn’t broadly valuable to most diabetic patients or their providers. Afrezza’s FDA-mandated lung function tests before and during treatment, along with lingering concerns over inhaled insulin safety,[40] created barriers to adoption, while advances in microneedles and insulin pens had already made injections less burdensome.[41] Additionally, Afrezza’s high cost, rigid dosing, and inability to fully replace needles for patients requiring basal insulin limited its real-world utility,[42],[43] leading to poor patient retention and an eventual collapse of Sanofi’s $2 billion partnership despite initial optimism. Before its 2014 launch, Afrezza was predicted to do $234M in US sales by 2018, but only achieved $32M.

Second, the ability and willingness of patients to pay out-of-pocket for certain therapies may be shifting. The success of GLP-1s and Gardasil 9 showed that patients were willing to pay out of pocket for benefits like weight loss or superior protection, which exceeded initial expectations.

Analysts initially underestimated Gardasil 9’s potential in China, assuming that high out-of-pocket costs—ranging from $254 to $576 for the full series—would curb demand.[44],[45] HPV vaccines were not included in the national immunization schedule, meaning only select regions offered free bivalent options to adolescent girls.[46] Most expected those patients would opt for government-subsidized alternatives rather than paying a premium for Gardasil 9. Yet, the vaccine defied expectations, generating $3.1 billion in sales to Zhifei Bio in 2022 alone.[47],[48] Gardasil 9’s success was fueled by China’s growing upper-middle-class population, who viewed the 9-valent vaccine as a superior option and were willing to pay for better protection, to the extent that China accounted for 60% of international sales.[49],[50] In cities like Shenzhen, for instance, public institutions allocated vaccine slots via a monthly lottery—where less than 4% became eligible—which led many women to seek higher-priced private clinics or even travel abroad for immunization.[51] Unlike in Western markets, where payer negotiations dictate access, Merck benefited from strong consumer-driven demand in China.

A similar story is playing out with the second generation of GLP-1 agonists. What analysts critically missed was the profound impact of weight loss on patient demand and willingness to pay out-of-pocket. Even modest weight loss (-6% to -8% with early GLP-1s) led to widespread adoption, and double-digit weight loss from second-generation GLP-1s drove sales for the overall category to $37.4 billion in 2023.[52],[53] A survey found that almost 20% of people on GLP-1s pay for the full costs themselves, driving a significant portion of the category’s performance, and suggesting that drug developers should consider patients’ willingness to pay out of pocket in addition to payer dynamics.[54],[55]

Finally, tracking market size for rapidly shifting diseases burdens or rare diseases remains challenging. Accurate market sizing is crucial for setting realistic forecasts, particularly in areas with limited existing data, such as rare diseases. Additionally, staying informed about competitor dynamics and patient uptake can help adjust expectations as the market evolves.

Luxturna, the only approved therapy for Leber congenital amaurosis (LCA), initially faced high market expectations, with peak sales projections ranging from $350M to $750M.[56] However, due to inaccurate market sizing and overestimated patient populations,[57],[58] actual sales only reached around $250M by 2023, with most eligible patients treated. The discrepancy highlights how over-extrapolated patient estimates from small studies led to inflated market forecasts, overestimating the market potential of Luxturna in the ultra-rare disease space.

Zepatier, Merck’s hepatitis C (HepC) drug, failed to meet market expectations largely due to misjudgments about the competitive landscape and patient population. While Merck priced Zepatier lower than competitors like Gilead’s Harvoni, it underestimated the speed at which Gilead’s treatments had already captured the HepC backlog, with Harvoni and Sovaldi rapidly treating a large portion of patients in 2014-2015 (Figure 3). Additionally, newer drugs emerged that treated more strains with shorter durations,[59] further reducing Zepatier’s appeal in an already saturated market, compounded by Gilead’s strong brand loyalty and successful payer negotiations.

Figure 3. Hepatitis C therapy predicted vs realized sales between 2013 and 2022. The red line is the total market sales. The blue line represents Zepatier. Note that Harvoni and Sovaldi sales are represented as one line since they were both early market entrants. Daklinza, Viekira Pak, and Vosevi were combined as small later entrants. Viekira Pak excluded from predicted sales because of lack of predictions in Evaluate Pharma database prior to US launch.

Science

While the factors above play important roles in the relative commercial success of products, drug success is still of course primarily driven by science, which can be high-risk. Several examples of under-performance in our sample were due to post-launch safety signals that were hard to predict. However, in our sample a few knowable factors about the science emerged which should be considered in developing product strategies.

First, innovations built on robust foundational science targeting mechanisms relevant across multiple indications have historically been some of the largest over-performers. For example, when Keytruda launched, analysts knew it was built on robust foundational science targeting the PD-1 pathway—already showing promise in melanoma, renal cancer, and lung cancer—but few anticipated how far this science could be leveraged. Early projections dramatically underestimated its potential: in 2014 pre-launch, analysts predicted 2020 US sales of $2.7 billion, and even by August 2017, forecasts had only risen to $4.9 billion. In reality, Keytruda’s US sales reached $8.4 billion in 2020, demonstrating how analysts consistently underestimated its expanding applications.[60]

The turning point came with Keytruda’s carefully designed KEYNOTE-024 trial in first-line non small cell lung cancer, focusing on patients with high PD-L1 expression and demonstrating a significantly longer progression-free and overall survival.[61] This success, followed by broader NSCLC approval regardless of PD-L1 status in 2017, laid the groundwork for Keytruda’s dominance. Merck’s sophisticated approach to biomarker-driven trial design propelled Keytruda to 40 FDA-approved indications by 2024. Keytruda’s unrivaled success underscores how coupling strong foundational science with a shrewd market expansion strategy can transform a promising therapy into a market leader.

However, while biomarker-driven strategies can unlock substantial value, functional outcomes rather than biomarkers alone often provide the most reliable prediction of a therapy’s ultimate market performance.

Jardiance is an example where exceptional outcomes data developed post-launch led to unforeseen market dominance. At launch, analysts saw it as just another SGLT2 inhibitor for diabetes, as no data had been released to suggest cardiovascular benefits. However, when Jardiance’s EMPA-REG OUTCOME trial readout in 2015 demonstrated a 38% reduction in cardiovascular death risk in diabetic patients with heart disease, analysts nearly quintupled sales projections.[62],[63] The strength of the cardiovascular data led to a swift label expansion in 2016, making Jardiance the first diabetes medication approved to reduce cardiovascular disease (Figure 4).[64]

Figure 4. Jardiance worldwide predicted and realized sales between 2014 and 2020. There was a clear and unpredicted inflection in realized sales between 2015 and 2016, after the cardio-protective data was released, which is largely due to label expansion.

On the other hand, Onpattro (Alnylam), an RNAi therapy designed to silence the mutated TTR gene in hATTR amyloidosis, underperformed analyst expectations largely due to scientific and clinical hurdles. Despite its strong biochemical impact on biomarkers like serum TTR levels, it failed to demonstrate a clinically meaningful improvement in key clinical measures like the six-minute walk test for transthyretin amyloid cardiomyopathy, leading to an FDA rejection of label expansion.[65] Additionally, competition from Pfizer’s Vyndamax, a more convenient and cheaper oral option, along with the launch of Amvuttra—a subcutaneous alternative with similar efficacy—further fragmented the market, limiting Onpattro’s adoption despite its theorized mechanistic advantages.[66],[67] Notably, Vyndamax was first approved in the cardiomyopathy indication and Amvuttra was eventually approved in cardiomyopathy in 2025. Five years after its 2019 launch, Onpattro achieved $247M in US sales compared to the pre-launch prediction of $447M at year-five.

Supply chain

No framework for pharmaceutical success can be complete without addressing the supply chain. Designing supply chains for new therapies with substantial demand uncertainty requires working through multiple potential scenarios to meet the required cost, quality, and reliability.

The challenges of supply chain in limiting growth for autologous CAR-T therapies have been well-documented elsewhere, leading to both cost of therapy constraints and scalability issues. The investments required in product-specific capabilities for these therapies required a balanced view across growth aspirations against capital and cost. More generally, understanding and planning for product-specific investments needed to scale is crucial to managing growth.

Additionally, while outside of our core sample set, there have been numerous examples over the years of companies that have been able to take advantage of competitors’ supply chain missteps to gain share. A recent example is Elahere, which was able to respond to the paclitaxel/carboplatin shortage in 2023 and gain meaningful share.[68],[69]

Summary

This retrospective analysis of product over- and under-performance suggests several themes that should be addressed by product strategists, quantified by product forecasters, and evaluated by company executives, portfolio managers and investors. A coordinated approach that ensures a deep understanding of each category–payer, provider, patient, science, and supply chain–is necessary for accurate forecasting and commercial success. By collecting and analyzing robust, real-time data across all five areas, companies can spot early warnings and quickly refine their strategies. Novel tools, including predictive analytics, machine learning models, and emerging “big data” sets (e.g., claims data or digital health records), offer a clearer view of the market’s moving parts. Regularly revisiting forecasts in light of real-world signals—such as new competitor launches, evolving practice guidelines, or emerging side effect profiles—can prevent overconfidence or inertia.

Table 1: Framework and Key Questions for Product Strategy

| Key Element / Value Inflection Lever | Associated Questions | |

| Payer | Cost-Benefit Threshold | Does the therapy meet cost-benefit thresholds, both in absolute terms and in comparison with alternatives? |

| Net Cost Savings | Does the therapy save payer costs on net? If so, are those savings likely in-year, during the payer’s typical patient relationship, or over the full lifetime of the patient? | |

| Budget Impact | Does the aggregate net-add in likely payments (price × # of patients) exceed the inflation target for the risk pool? | |

| Pricing Strategy | Is the pricing approach (list price and rebates) driving advantage for the category? | |

| Patient | Out-of-Pocket Willingness | (How) has patient willingness to pay out-of-pocket been assessed? |

| Patient Behavior | What degree of change in behavior is required from patients? | |

| Market Size Dynamics | Will therapies change the market size (e.g., curative vs. maintenance)? How is the potential catch-up cohort being tracked? | |

| Provider | Provider Burden | What new burdens does the therapy place on providers? How are those burdens mitigated? |

| Burden Reduction | What existing burdens does the therapy help providers reduce? | |

| Science | Mechanistic Foundation | Does the therapy target a foundational mechanism that is likely to be relevant across multiple indications? |

| Robust Outcomes Timing | At what point in development will robust outcomes data be available? For us and for competitors? | |

| Supply Chain | Production Requirements | Does the product require product-specific investments and capabilities? |

| Scalability & Flexibility | What volume scenarios are planned for? What will it take (cost, capital, time) to shift to supply for a different scenario? |

[1] Evaluate Pharma, accessed March 2025

[2] Joseph Walker, “Amgen to Slash Price of Cholesterol Drug Repatha by 60%,” MarketWatch, October 24, 2019, https://www.marketwatch.com/story/amgen-to-slash-price-of-cholesterol-drug-repatha-by-60-2019-10-24.

[3] “Regeneron and Sanofi Announce FDA Approval of Praluent® (Alirocumab) Injection, the First PCSK9 Inhibitor in the U.S., for the Treatment of High LDL Cholesterol in Adult Patients | Regeneron Pharmaceuticals Inc.,” Regeneron, July 24, 2015, https://investor.regeneron.com/news-releases/news-release-details/regeneron-and-sanofi-announce-fda-approval-praluentr-alirocumab/.

[4] Kevin McCaffrey, “Praluent’s FDA Review Looms, but Questions Persist,” MM+M – Medical Marketing and Media, July 22, 2015, https://www.mmm-online.com/home/channel/pharmaceutical/praluents-fda-review-looms-but-questions-persist/.

[5] Ted Okerson et al., “Effect of 2013 ACC/AHA Blood Cholesterol Guidelines on Statin Treatment Patterns and Low‐Density Lipoprotein Cholesterol in Atherosclerotic Cardiovascular Disease Patients,” Journal of the American Heart Association 6, no. 3 (March 17, 2017): e004909, https://doi.org/10.1161/JAHA.116.004909.

[6] Geoffrey Meacham, Carter Gould, Michael Ulz, Barclays, Jan 2015.

[7] “Regeneron and Sanofi Announce FDA Approval of Praluent® (Alirocumab) Injection, the First PCSK9 Inhibitor in the U.S., for the Treatment of High LDL Cholesterol in Adult Patients | Regeneron Pharmaceuticals Inc.”

[8] “Dr Jay Edelberg on Safety, Efficacy of Praluent and Remaining Payment Challenges,” November 16, 2017, https://www.ajmc.com/view/dr-jay-edelberg-on-safety-efficacy-of-praluent-and-remaining-payment-challenges.

[9] Andrew Baum, Citi Research, 15 Feb 2019.

[10] Christopher J. Raymond, Allison M. Bratzel, Nicole A. Gabreski, Piper Sandler, 20 July 2023.

[11] “AbbVie’s SKYRIZI® (Risankizumab) Versus STELARA® (Ustekinumab) Head-to-Head Study in Crohn’s Disease Meets All Primary and Secondary Endpoints,” PR Newswire, October 15, 2023, https://www.prnewswire.com/news-releases/abbvies-skyrizi-risankizumab-versus-stelara-ustekinumab-head-to-head-study-in-crohns-disease-meets-all-primary-and-secondary-endpoints-301956749.html.

[12] “Skyrizi vs Humira Psoriasis Efficacy,” Skyrizi HCP, accessed March 7, 2025, https://www.skyrizihcp.com/dermatology/psoriasis-efficacy/skyrizi-vs-humira.

[13] Andrew Baum, Citi Research, 26 Sep 2019.

[14] Dickson SR, Gabriel N, Hernandez I. Contextualizing the Price of Biosimilar Adalimumab Based on Historical Rebates for the Original Formulation of Branded Adalimumab. JAMA Netw Open. 2023;6(7):e2323398. Published 2023 Jul 3. doi:10.1001/jamanetworkopen.2023.23398

[15] Arthur Allen, “Save Billions or Stick With Humira? Drug Brokers Steer Americans to the Costly Choice,” KFF Health News (blog), September 19, 2023, https://kffhealthnews.org/news/article/humira-abbvie-biosimilar-biologic-savings-pbm-rebates/.

[16] I. P. D. Analytics, “IBD Market Snapshot: Payers May Shift Preferred Products To Accommodate New Drugs,” IPD Analytics, November 16, 2022, https://www.ipdanalytics.com/post/ibd-market-snapshot-payers-may-shift-preferred-products-to-accommodate-new-drugs.

[17] Eric Sagonowsky, “AbbVie’s Discounting Humira to Aid Skyrizi’s Launch—and a Price War Could Follow: Analyst | Fierce Pharma,” May 20, 2019, https://www.fiercepharma.com/pharma/abbvie-discounting-humira-modestly-to-support-skyrizi-rollout-analyst.

[18] Coghlan J, He H, Schwendeman AS. Overview of Humira® Biosimilars: Current European Landscape and Future Implications. J Pharm Sci. 2021;110(4):1572-1582. doi:10.1016/j.xphs.2021.02.003

[19] Atsushi Seki, Barclays, 14 April 2014.

[20] Hiroshi Tanaka, Mizuho Securities, 4 June 2014.

[21] Atsushi Seki, Barclays, 10 April 2015

[22] DefinitiveHealthcare Drug Analytics, accessed March 2025.

[23] Atsushi Seki, Barclays, March 2015

[24] Thalayasingam, Nishanthi, and John D. Isaacs. “Anti-TNF Therapy.” Best Practice & Research Clinical Rheumatology, vol. 25, no. 4, Aug. 2011, pp. 549–67.

[25] Ben-Horin, S., and Y. Chowers. “Review Article: Loss of Response to Anti-TNF Treatments in Crohn’s Disease: Review: Loss of Response to Anti-TNF in Crohn’s Disease.” Alimentary Pharmacology & Therapeutics, vol. 33, no. 9, May 2011, pp. 987–95.

[26] Ben-Horin, Shomron, et al. “Optimizing Anti-TNF Treatments in Inflammatory Bowel Disease.” Autoimmunity Reviews, vol. 13, no. 1, Jan. 2014, pp. 24–30.

[27] State, Monica, and Lucian Negreanu. “Defining the Failure of Medical Therapy for Inflammatory Bowel Disease in the Era of Advanced Therapies: A Systematic Review.” Biomedicines, vol. 11, no. 2, Feb. 2023, p. 544.

[28] Marsal, Jan, et al. “Management of Non-Response and Loss of Response to Anti-Tumor Necrosis Factor Therapy in Inflammatory Bowel Disease.” Frontiers in Medicine, vol. 9, June 2022. Frontiers

[29] “ENTYVIO FDA Label” (FDA, 2014).

[30] John Carroll, “Novartis Wins a Key OK for Kymriah, but Continuing Manufacturing Woes Hobble Rollout — Rival Gilead CAR-T Breaks into Europe,” Endpoints News, August 27, 2018, https://endpts.com/novartis-wins-a-key-ok-for-kymriah-but-continuing-manufacturing-woes-afflict-their-rollout-rival-gilead-breaks-into-europe/.

[31] Ned Paglarulo, “Novartis Still Hasn’t Solved Its CAR-T Manufacturing Issues,” BioPharma Dive, December 11, 2019, https://www.biopharmadive.com/news/novartis-kymriah-car-t-manufacturing-difficulties-cell-viability/568830/.

[32] Elvidge, “Despite CV Benefit, Amgen Still Facing Challenges over Repatha Cost.”

[33] Kevin Dunleavy, “ASCO: Positive Trial Shows Novartis’ Kymriah Poised to Play Catch-up in CAR-T Rivalry with Gilead’s Yescarta | Fierce Pharma,” June 3, 2021, https://www.fiercepharma.com/pharma/positive-trial-shows-novertis-kymriah-poised-to-play-catchup-car-t-rivalry-gilead-s-yescarta.

[34] Brian Lian, Truist Securities, 15 Feb 2013

[35] Catherine J. Arnold, Ari Jahja, Ronak H. Shah, Credit Suisse, 2 July 2012

[36] Jeffrey Holford, Jeffries, October 28, 2015

[37] Jeffrey Holford, Jeffries, October 28, 2015

[38] Tim Race, Sarah Thomas, Richard Parkes, Gregg Gilbert, Grunnar Romer; Deutsche Bank, 12 Sep 2016

[39] Jacob Oleck, Shahista Kassam, and Jennifer D. Goldman, “Commentary: Why Was Inhaled Insulin a Failure in the Market?,” Diabetes Spectrum : A Publication of the American Diabetes Association 29, no. 3 (August 2016): 180–84, https://doi.org/10.2337/diaspect.29.3.180.

[40] “Afrezza Label” (FDA, 2014).

[41] Harvinder S. Gill et al., “Effect of Microneedle Design on Pain in Human Subjects,” The Clinical Journal of Pain 24, no. 7 (September 2008): 585–94, https://doi.org/10.1097/AJP.0b013e31816778f9.

[42] Oleck, Kassam, and Goldman, “Commentary.”

[43] “MannKind Corporation Announces FDA Approval of AFREZZA(R); A Novel, Rapid-Acting Inhaled Insulin for the Treatment of Diabetes | MannKind Corporation,” MannKind, June 27, 2014, https://investors.mannkindcorp.com/news-releases/news-release-details/mannkind-corporation-announces-fda-approval-afrezzar-novel-rapid.

[44] You-Lin Qiao, Maria Gonzalez-Mendez, and Yan-Qin Yu, “Current Status of HPV Vaccine in China,” accessed March 7, 2025, https://www.hpvworld.com/articles/current-status-of-hpv-vaccine-in-china/.

[45] Wang H, Jiang Y, Wang Q, Lai Y, Holloway A. The status and challenges of HPV

vaccine programme in China: an exploration of the related policy obstacles. BMJ Glob Health. 2023.

[46] Zhao, XL., Tackling barriers to scale up human papillomavirus vaccination in China: progress and the way forward. Infect Dis Poverty 12, 86 (2023).

[47] Wolfe Research, 15 March 2023.

[48] Shenzhen Stock Exchange, Announcement on Renewal of Supply, Distribution, and

Co-promotion Agreement with Merck & Co., 30 Jan 2023

[49] Wolfe Research, 15 March 2023.

[50] Kevin Dunleavy, “As Gardasil Sales Fall in China, Merck Has Few Answers Why,” July 30, 2024, https://www.fiercepharma.com/pharma/merck-mystified-sudden-step-down-gardasil-sales-china.

[51] Luo Meihan, “China Expands HPV Vaccines Age, but Supply Concerns Remain,” #SixthTone, September 1, 2022, https://www.sixthtone.com/news/1011131.

[52] Ryan, Donna, and Andres Acosta. “GLP ‐1 Receptor Agonists: Nonglycemic Clinical Effects in Weight Loss and Beyond.” Obesity, vol. 23, no. 6, June 2015, pp. 1119–29. DOI.org (Crossref), https://doi.org/10.1002/oby.21107.

[53] Tim Race, Sarah Thomas, Richard Parkes, Gregg Gilbert, Grunnar Romer; Deutsche Bank, 12 Sep 2016

[54] Alex Montero et al., “KFF Health Tracking Poll May 2024: The Public’s Use and Views of GLP-1 Drugs,” KFF (blog), May 10, 2024, https://www.kff.org/health-costs/poll-finding/kff-health-tracking-poll-may-2024-the-publics-use-and-views-of-glp-1-drugs/.

[55] Interestingly, GLP-1’s success was captured by only 2 of the 3 insulin giants. Sanofi’s GLP-1 offering, Adlyxin/Lyxumia, delivered minimal weight loss benefits and lacked significant cardiovascular advantages. Their combination product, Soliqua (a GLP-1 and insulin combo), also struggled to gain traction due to dosing complexity and gastrointestinal side effects. Meanwhile, Novo Nordisk and Eli Lilly fully capitalized on the category’s growth, recognizing early that weight loss would heavily influence patient preference.

[56] Kathleen Gordon et al., “Gene Therapies in Ophthalmic Disease,” Nature Reviews Drug Discovery 18, no. 6 (January 23, 2019): 415–16, https://doi.org/10.1038/d41573-018-00016-1.

[57] Recon trategy, “Commercial performance of AAV gene therapies.”

[58] Hiroyuki Morimura et al., “Mutations in the RPE65 Gene in Patients with Autosomal Recessive Retinitis Pigmentosa or Leber Congenital Amaurosis,” Proceedings of the National Academy of Sciences 95, no. 6 (March 17, 1998): 3088–93, https://doi.org/10.1073/pnas.95.6.3088.

[59] Robert Lowes, “FDA OKs 8-Week Mavyret for Hepatitis C,” MedScape, August 3, 2017, https://www.medscape.com/viewarticle/883778.

[60] EvaluatePharma, Accessed March 2025

[61] Reck, Martin, et al. “Pembrolizumab versus Chemotherapy for PD-L1–Positive Non–Small-Cell Lung Cancer.” New England Journal of Medicine, vol. 375, no. 19, Nov. 2016, pp. 1823–33. DOI.org (Crossref), https://doi.org/10.1056/NEJMoa1606774.

[62] Zinman, Bernard, et al. “Empagliflozin, Cardiovascular Outcomes, and Mortality in Type 2 Diabetes.” New England Journal of Medicine, vol. 373, no. 22, Nov. 2015, pp. 2117–28

[63] Jeffrey Holford, Jeffries & Co, September 17, 2015

[64] “FDA Approves Jardiance to Reduce Cardiovascular Death in Adults with Type 2 Diabetes,” FDA (FDA, March 24, 2020), https://www.fda.gov/news-events/press-announcements/fda-approves-jardiance-reduce-cardiovascular-death-adults-type-2-diabetes.

[65] Mathew Maurer, “Primary Results from APOLLO-B, A Phase 3 Study of Patisiran in Patients with Transthyretin-Mediated Amyloidosis with Cardiomyopathy.”

[66] Mazen Hanna et al., “Improvements in Efficacy Measures With Tafamidis in the Tafamidis in Transthyretin Cardiomyopathy Clinical Trial,” JACC: Advances 1, no. 5 (December 14, 2022): 100148, https://doi.org/10.1016/j.jacadv.2022.100148.

[67] Aldostefano Porcari et al., “Breakthrough Advances Enhancing Care in ATTR Amyloid Cardiomyopathy,” European Journal of Internal Medicine 123 (May 1, 2024): 29–36, https://doi.org/10.1016/j.ejim.2024.01.001.

[68] https://www.fightcancer.org/sites/default/files/economics_of_drug_shortages_final

[69] https://cancerletter.com/clinical/20230526_1/