Introduction

As we described in a prior whitepaper, explaining over- and under-performance of newly launched therapies relative to pre-launch expectations is a critical element to enabling robust product strategy in the future. Broadly, we concluded that product performance hinges on the interplay of multiple factors: scientific efficacy, pricing strategy, patient preferences, and payer dynamics—each capable of shifting market outcomes in meaningful ways.

One theme identified then, for which we see increasing evidence, is that in today’s therapeutic landscape, efficacy and payer access are increasingly more determinant of success than advantages in route of administration alone. We previously saw this dynamic with injectable GLP1s winning against oral SGLT2s in the cardiometabolic space. A similar pattern is now emerging in moderate-to-severe plaque psoriasis, where the oral newcomer Sotyktu has been relegated to later-line use and underperformed expectations thus far. Despite an advantage in route of administration, more modest efficacy as indicated by PASI scores (Psoriasis Area and Severity Index) in clinical readouts, along with less favorable pricing and access compared to market leader Skyrizi, has constrained Sotyktu’s adoption.

The following analysis summarizes the factors driving Sotyktu’s underperformance – including the failure of its positioning as best available oral therapy – and identifies both potential market disruptors in the immunology pipeline as well as broader lessons for other product strategies.

Sotyktu’s challenges

In 2022, Sotyktu entered the psoriasis market as the first new oral therapy in approximately a decade.[1] As a TYK2 inhibitor, its target specificity offered advantages over broader JAK inhibitors, with reduced risk of malignancies, muscle disorders, and thromboembolic events. Sotyktu averted FDA black box warnings, which were ubiquitous to the JAK class. Pre-launch, BMS projected $4B in peak sales across psoriasis, psoriatic arthritis, lupus, and IBD indications.[2],[3] However, actual sales have remained well below projections due to two main reasons: demonstrated efficacy and payer access.

Efficacy lags standard-of-care

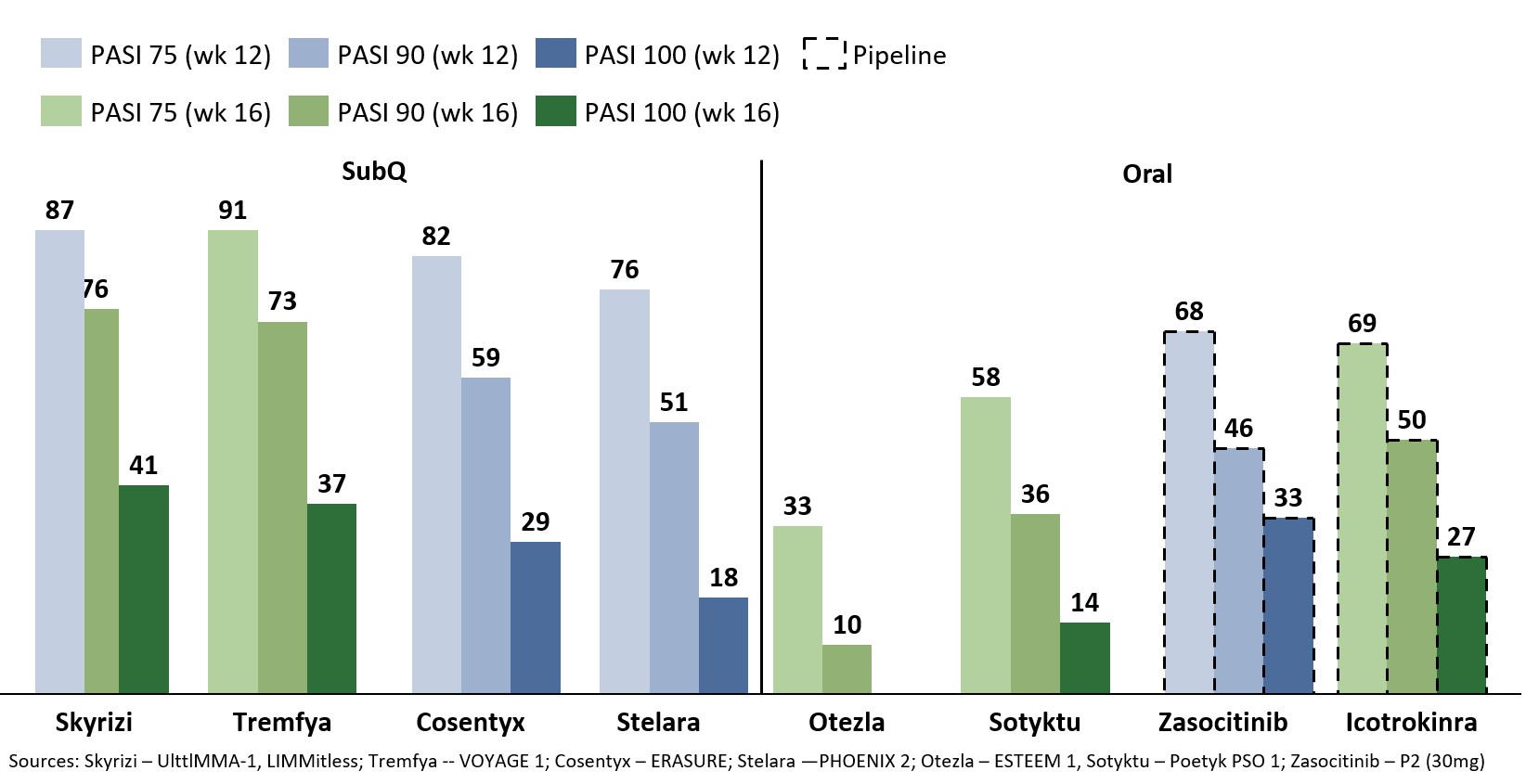

The market for psoriasis is particularly competitive, with a number of therapies available to patients. Across all psoriasis treatment options, Skyrizi sets the efficacy benchmark for PASI reduction, with other biologic drugs at similar levels (Exhibit 1). In the oral treatment modality, Otezla was the leading oral treatment option until Sotyktu’s approval. But while Sotyktu’s clinical efficacy surpassed Otezla’s, it trails significantly behind Skyrizi’s.

Exhibit 1. Percent patients reaching PASI75, PASI90, and PASI100 clearance for select in-market and pipeline Psoriasis drugs

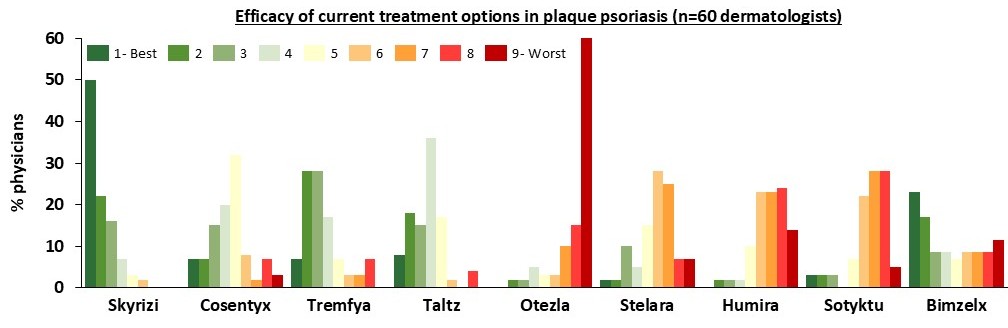

A Deutsche Bank survey of 60 dermatologists ranking nine plaque psoriasis therapies (Skyrizi, Cosentyx, Tremfya, Taltz, Otezla, Stelara, Humira, Sotyktu, Bimzelx) demonstrated Sotyktu’s unfavorable efficacy profile (Exhibit 2).[4] Sotyktu clustered near the bottom when it came to efficacy, with 50% of dermatologists ranking it either 7th or 8th out of nine options (25% each). Only Otezla performed worse, with 60% of respondents ranking it in the bottom position. Skyrizi dominated efficacy, ranking 1st for 50% of respondents.

Exhibit 2. Dermatologist’s perception of efficacy of current treatment in psoriasis

Additionally, dermatologist KOL interviews indicate that physicians hold mixed views regarding Sotyktu’s clinical efficacy.

- “It definitely as an oral works much, much better than Otezla. Is it going to compete with a biologic most consistently? No, absolutely not.” Epiphany Dermatology (July 2025)

- “It’s only more or less for the needle phobic or if a patient has tried and failed one or more biologics/” Paragon Dermatology (July 2025)

- “Most physicians in my area haven’t been impressed with Sotyktu. It just hasn’t lived up to the clinical data that it was supposed to have.” Former Amgen sales representative (Aug 2025)

Physician interviews consistently reinforced the clinical superiority of biologics such as Skyrizi, indicating that orals are regarded either as later-line therapies or for limited populations only.

Rebate barriers block access

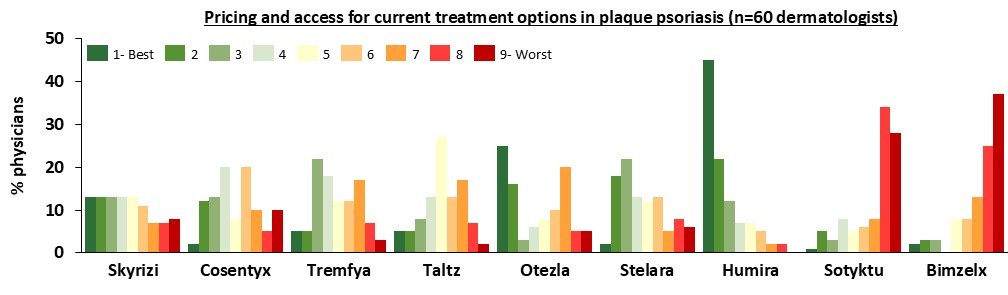

Another dermatologist survey data point from Deutsche Bank showed that SOTYKTU fared worse when it came to pricing and access, with 65% of dermatologists ranking it in the bottom two positions (35% ranked it 8th, 30% ranked it 9th) (Exhibit 3). Only Bimzelx scored lower on price and access metrics. Humira, with biosimilar versions now on market and Abbvie defending with aggressive rebates to secure formulary position, earned the top price/access ranking from 45% of respondents.

Exhibit 3. Dermatologist’s perception of pricing and access of current treatment in psoriasis

Dermatologist KOL interviews also identify consistent themes around SOTYKTU’s limited formulary access relative to established biologics. A Northwestern dermatologist (October 2023) indicated, “If you take four patients and they all decide they want to go on SOTYKTU, two or maybe only one of them can get it covered by their insurance.”

BMS has acknowledged these access constraints through strategic pivots beyond traditional channels. In September 2025, the company announced plans to offer Sotyktu through its Patient Connect direct-to-consumer platform at over 80% below list price ($6,678 for a 30-day supply)[5]. This approach signals BMS’s recognition that traditional payer strategies have proven insufficient.

Upcoming oral challengers – Ikotrokinra, Zasocitinib, and beyond

Icotrokinra, an IL-23 inhibitor, represents a potential near-term oral competitor in psoriasis, further crowding this market. In Phase 3 head-to-head ICONIC-ADVANCE trials, Icotrokinra demonstrated superiority over Sotyktu at Weeks 16 and 24, though PASI90 and PASI 100 clearance rates lag Skyrizi’s. At Week 52, Icotrokinra achieved an 84% PASI90 response (versus 21% placebo), similar to Skyrizi’s 82% PASI90 efficacy at the same timepoint; however, week 16 clearance rates meaningfully lag Sykrizi’s. With competitive payer access, this favorable clinical profile could translate into strong commercial performance. However, sustained uptake will depend on pricing that aligns with demonstrated efficacy, and not just on perceived oral convenience alone, particularly since Skyrizi’s once-every-12-week subcutaneous dosing is already a low-burden alternative. It also remains to be seen whether Icotrokinra’s comparatively slower Week 16 clearance rates will allow for first-line positioning among physicians and patients.

Other products in the pipeline include Takeda’s Zasocitinib (TAK-279), which also has the potential to disrupt the market if it achieves similar efficacy to Icotrokinra while maintaining a cleaner adverse event profile. As a TYK2 inhibitor, Zasocitinib may benefit from narrower targeting compared to IL-23 inhibitors like Icotrokinra. Preliminary 12-week data demonstrate efficacy comparable to leading psoriasis products (Exhibit 1), and longer-term data are expected to show further improvement. While clinical data remains early, Oruka’s once-yearly IL-23 injectable (ORKA-001) represents another differentiating approach. Phase 1 data demonstrated an approximately 100-day half-life, with Phase 2a trials now underway. Whether annual dosing versus 6-8 week injectable schedules will meaningfully influence patient preference remains an open question.

Summary

Sotyktu’s market uptake demonstrates that a route of administration advantage does not alone translate to commercial success. In diseases where patients are highly motivated by outcomes, particularly those with visible symptoms or significant quality of life impact like psoriasis, efficacy increasingly supersedes dosing convenience. Sotyktu is currently primarily used for biologic failures, due to both weaker efficacy relative to IL-23 leaders and disadvantaged market access against AbbVie’s best-in-class rebate and formulary coverage. Their near-term challenges may further intensify if next-generation products from Johnson & Johnson and Takeda deliver stronger results while addressing payer access. More broadly, the psoriasis story demonstrates that oral convenience may only compensate for modest efficacy gaps. Next-generation products in competitive market segments must deliver on a combination of efficacy, reduced adverse events, improved patient convenience and payer coverage in order to meaningfully win market share.

[1]https://www.biospace.com/bms-wins-clean-label-approval-for-first-plaque-psoriasis-oral-innovation-in-a-decade

[2] 4Q2021 BMS Investor Event Presentation

[3] Jan 2022 JP Morgan Presentation

[4] Deutsche Bank, 14 March 2024

[5]https://www.pharmaceutical-technology.com/newsletters/bms-direct-to-consumer-sotyktu-expansion/?cf-view