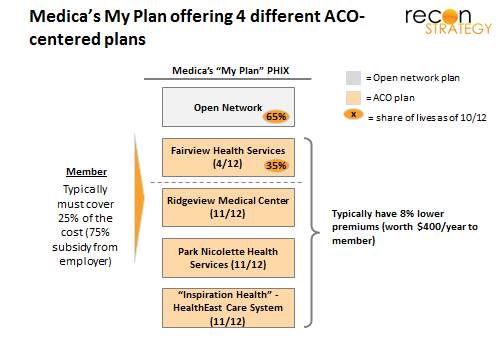

At a TEDMED conference a couple years ago, I had to write some sample “ask me” questions on the bottom of my ID badge as conversation starters. One of them was “Ask me why PHIX+ACO=:-)” Given the presentations on 3D tissue printers and technologies to help blind people just about see again, I was not surprised to have few takers. However, recent news from Minnesota suggests that others see the potential in combining risk-taking providers with exchanges. Medica – one of the early leaders in private exchanges with Bloom Health — is expanding the offerings on its My Plan exchange to include four products, each centered on a single major system operating as an ACO and sold side-by-side against an open network plan. This is a fascinating development.

The employer-based insurance model places multiple drags on innovation: moral hazard (employees demand richer coverage because of the advantaged tax treatment, blunting the rewards to innovations in cost reduction); principal-agent (HR departments bear the brunt of additional work, complaints and ire created by new, complex or restrictive designs and therefore have a special incentive to avoid them); and heavy reliance on procurement leverage (employers choose a one or two plans from one or two health plans which offer the “best” compromise across their diverse employees, stopping innovative products such as narrow network getting traction). Private exchanges remove some of drags: the defined contribution component puts the choice and the cost of those choices into the hands of the consumer (removing moral hazard and removing the accountability of HR in selecting a plan); private exchanges then break the model of concentrated procurement leverage by expanding the range of choice open to consumers across employer sets.

By centering products on particular provider systems, Medica is exposing these providers to market forces and market opportunity. There are a couple aspects to keep in mind:

- Enhancing the power of shared savings: The economics of shared savings models are often not that great once you factor in payment uncertainties and onerous reporting requirements. Bring together shared savings with an opportunity to attract more patients, however, and the story can become a lot more compelling (particularly if those patients have an incentive to pick a cost-effective provider). You could potentially double or better the value of shared savings bonuses alone.

- Providing more value to consumers: Cost-effectiveness does not have to be the only enticement offered to consumers. The four providers on Medica’s My Plan are trying to distinguish themselves with various conveniences. The ideas are fairly routine so far (same-day appointments, integrated call centers which can address medical and coverage topics, free wellness evaluations and coaching sessions, electronic access to medical records, etc.) but it is early days and the key is the dynamic being put in place.

- Blunting the relative attractiveness for providers to become insurers. Providers becoming health insurers are in the news a lot these days. But becoming an insurer involves a lot of infrastructure build and execution risk and is not a decision to be undertaken lightly. The Medica model could offer an attractive alternative to these providers by offering much of the benefits of being an insurer (specifically a way of converting cost effectiveness into a growth strategy) at a much lower cost.