Summary

- Aetna has struck a deal to sell individual health insurance with Costco, the #6 retailer. The deal targets 9 populous states first with more to follow in 2012

- While the deal lacks some of the levers of the very successful Walmart-Humana Part D deal, there is real potential for this channel to attract consumers if employers opt-out on a large scale

- Given that Aetna has some arrangements with Best Buy (the #9 retailer) and an established alliance with CVS (the #7 retailer), it looks like Aetna is building out a multi-prong big box retailer channel strategy; others may follow

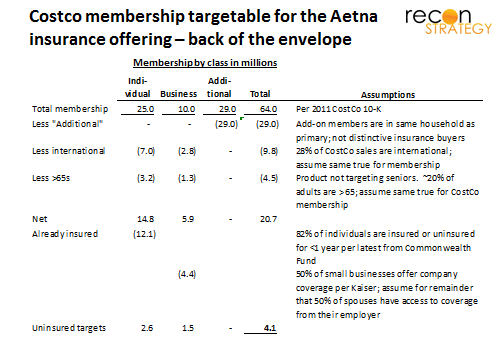

Aetna has struck a deal with Costco, a warehouse club retailer, to sell individual health insurance in nine states (with plans for roll out to more in 2012). Costco is the #6 retailer in the country and has about 50% of the warehouse club market. This is Aetna’s second deal with a major retailer this year: the first was a more modestly scaled pilot to sell wellness products but with Best Buy, the #9 retailer in the county. Costco claims overall membership of 64M. The target market within that membership is a lot smaller (probably closer to 4M) but certainly still attractive. A quick teardown:

Note: although a big share of the Costco membership is small business, these members may still be targets for an offering (given that many small businesses do not offer coverage). My assumptions could be debated (e.g., are Costco members more or less likely to be uninsured vs. the rest of the country) and the estimates would need to be adjusted to reflect geographic distribution of Costco customers and the Aetna offering. But the potential market is large enough to be interesting.

This deal occurs at a time when there is a lot of fluidity in the health insurance channel driven by near term pressures (e.g., MLR rules impact on broker commissions) and longer-term scenarios regarding whether and how employers will retreat from providing coverage (opt out, switch to defined contribution, growth of private exchanges, etc.). Insurers and retailers have been exploring the potential of a variety of channel models such as:

- Insurers forward integrating into retail by opening stores (e.g., Blues plans such as Highmark)

- Retailers backward integrating into health insurance distribution (e.g. Walgreen’s plans to pursue a private exchange – or PHIX – strategy)

- Joint builds: most interesting perhaps being the Walmart-Humana Part D collaboration which coupled a powerful retail brand, massive traffic, a preferred delivery network (built around Walmart affiliated pharmacies) with an insurance product.

The contrast between the Walmart Humana deal, WAG’s PHIX move and the Aetna-Costco deal is instructive. Keep in mind that the Walmart-Humana deal seems to be a winning formula, generated a lot of traction both in gaining share and acquiring copy-cats among competitors. It is not clear structurally if WAG-PHIX or Costco-Aetna can match that success given the broader scope (all medical, not just pharmacy) of the primary offers:

Walmart-Humana

- Jointly branded product

- Some shared economics enabled by focusing on a coverage domain (pharmacy) where Walmart and Humana can act as major providers (Walmart on the retail, Humana on the mail-order) and value of incremental cross-sell of non-pharmacy products derived from the traffic

- Strong differentiation on price and design

- Reinforced consumer ties with the retailer (pulling in their prescriptions and any incremental purchasing from the visits)

WAG- PHIX

Not a lot of details have been announced regarding the plan, but some surmises:

- Little joint branding: the PHIX will likely offer competing plans and a mix of products (presumably full medical, though perhaps some MedSupp and Part D) on the exchange. Accordingly, there will be limited leverage to push for custom designs.

- There may be a wild-card play with WAG co-branding an ultra-low cost offering similar to the “we have the branded OTCs but our generic version on the same shelf is so much cheaper” pitch which plays out on many chain drugstore shelves.

- Commercial coverage will likely be full medical, so WAG also cannot play a decisive role in care provision, limiting sharable vertical economics. There may be some prominence afforded the WAG pharmacy and Take Care clinics but the bulk of medical care will be delivered by other care providers (especially if WAG does not want to harm its relations with prescribing physicians).

- Key value will be in the low cost cross-selling to the WAG customer base and perhaps some pricing achieved by exchange based competition.

Costco-Aetna

- Jointly-branded products

- Focus on affordability (product range is for high deductible plans)

- Limited vertical economics: Costco does pharmacy, of course but has not done much with clinics (so far); the products do have lower copays for Costco pharmacies but consolidating retail scripts would still offer only limited vertical economics relative to the overall cost of insurance (though there may be some clever ways to package this via co-pays)

- Key value will probably be in lower customer acquisition costs (the cross-sell) and perhaps in Costco leverage: In theory, by focusing on a single insurer, Costco can use its buying leverage to get the best custom deal for its customers — broadly consistent with their retail philosophy which is highly selective on the vendors and SKUs stocked depending on the deal which they can cut.

- For Aetna, this may be an economically viable channel to reach the individual market (which historically has had much higher selling costs than group products but is now also subject to MLR rules).

Though the press release promises special features for the Costco Aetna product, these aren’t obvious outside in. The differentiation and incremental value proposition is probably still modest at this point – of course, it is early days still. Also the outbound marketing may describe something more compelling.

The roll out seems ambitious: the first nine states include Aetna’s flagship market Connecticut, along with populous states such as Georgia, Illinois, Michigan, Pennsylvania, Texas, and Virginia (also: the less populous Arizona and Nevada). With more states planned for 2012, this seems like less of a pilot and more of a land grab to sew up a major retailers with a nice cross-section of individual and small business customers.

Aetna’s strategy may very well be to establish the channel first – especially with the 2014 big bang just around the corner – and then modify the products and offering in time for the 2013 selling year. What might come next? Some thoughts:

- More focused networks – pharmacy to start; perhaps Costco may dive into the convenience clinic market to expand the vertical economics

- Integrated tracking for deductible healthcare products bought at Costco for savings accounts (perhaps taking advantage of the capabilities Aetna beefed up with the Payflex acquisition)

- Kiosks and temporary departments during peak season to sell insurance (avoiding the fixed bricks and mortar costs of other strategies)

- An expansion into small business coverage products

Given in-place deals with Costco (#6 retailer) and Best Buy (#9 retailer), Aetna is clearly building out an option on a big box retailer channel which could pay off big in a scenario of major employer opt-out. Aetna’s relationship with the Caremark PBM may give it an option with CVS (the #7 retailer). The list of unaligned retailers (or ones likely pushing go it alone strategies such as WAG or likely attracting risky populations such as Home Depot) is getting shorter!